Weekly Roundup: Widening Our Lead and Adding a New Position

Indexes crossed key mileposts during a week where we increased our year-to-date lead over the S&P 500 and added a fresh name to the Pro Portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market climbed higher this week with the S&P 500 crossing the 6000 level and the Nasdaq Composite surpassing 19,500. In Friday’s video, we explained why the Pro Portfolio widened its lead over the market this week, and we go into some additional detail on that below in the Catching Up on the Portfolio This Week section.

What’s significant about the S&P 500 and the Nasdaq Composite reclaiming those levels is that they haven’t been there since late February. Back then, we had yet to see President Trump’s tariffs and the market expected more Fed rate cuts than it currently does. Over the last four weeks, the S&P has rebounded more than 6% and the Nasdaq Composite more than 9%, and while the relative strength (RSI) level for neither is over 70, both are not that far off. It's not quite as quick as the market move we saw between mid-April to mid-May, but it’s enough for us to tread cautiously, especially as the Fear & Greed Index is flashing “Greed.”

Following the May PMI and April Import/Export data published during the first half of this week, the Atlanta Fed’s GDPNow Model was revised back to +3.8% for the current quarter. Friday's May Employment Report, which showed better-than-expected job creation and wage pressure ticking up as well, is likely to tip that figure a bit higher. Our view has been these and other recent data points should lead the market to reconsider the three 25-basis point rate cuts it has been expecting per the CME Fed Watch tool. As we close out the week, it still shows the market calling for three 25-basis point rate cuts this year.

With Atlanta Fed President Raphael Bostic signaling ahead of the May Employment Report that he sees room for just one rate cut, the growing likelihood is more Fed heads will fall into that camp based on the aggregate data published this week. We also have to wonder if Bostic’s comment helps lay the groundwork for the Fed’s upcoming set of economic projections that it will publish alongside its next policy decision on June 18.

Our view for some time has been those forthcoming updates will give us a far better indication of what the Fed is likely to do or not do. Gaming it out, the odds of the Fed telegraphing on June 18 just one rate cut in the second half of 2025 will increase if next week’s May CPI and PPI data support the May inflation data we’ve seen thus far and there is no meaningful progress on trade deals. Not trade talks, trade deals.

On Friday, President Trump said trade talks between the U.S. and China would resume on Monday in London. While we are cautiously optimistic that we could see progress, our position continues to be that final trade deals and their details are what matters. They will also help remove some of the uncertainty that is overhanging the market and EPS expectations for the 2025 second half. While the market would welcome a quick deal to be struck, the probability of that happening isn’t very high in our opinion.

Barring any developments on that front early next week, should we see the market continue to melt up ahead of the May CPI and PPI reports, ones that we think could take some of the wind out of the market’s sails, we may opt for prudent portfolio action to lock in some of the big quarter-to-date gains in the Pro Portfolio.

Catching Up on the Portfolio This Week

The Pro Portfolio continued to pull ahead of the S&P 500 this week, led by a strong performance from Marvell MRVL, Meta META, Axon Enterprise AXON, Elastic ESTC, Nvidia NVDA, and our newest position, SuRo Capital SSSS. While the bulk of Pro Portfolio holdings advanced more than the S&P 500 this week, there were still a few names that underperformed, including United Rentals URI, Vulcan Materials VMC, Waste Management WM, and Palantir PLTR.

Naturally, stock prices can vary week to week, but quarter-to-date all our positons, except Waste Management, are up double digits and well ahead of the S&P 500. With WM shares, despite treading water of late, are up more than 15% on a year-to-date basis, which makes them a strong performer relative to the overall market. Remember, the next known catalyst for WM shares is Waste Management's 2025 Investor Day on June 24.

In the May Monthly Roundup, we shared that Elastic and Marvell were on our shopping list and that we would likely be buyers when the shares settled out this week. We did just that on Tuesday, picking up additional ESTC shares at $81 and MRVL at $62.29. Our conclusion that Elastic management issued overly conservative guidance, the culprit in leading to the latest pullback in the shares last week, was confirmed by management’s investor conference presentation this week.

The next day, we called up SuRo Capital to the Pro Portfolio from the Bullpen, initiating a small position at $6.76 with a Two rating. In that Alert, we laid out our investment case for SSSS as SuRo looks to monetize its investment portfolio as the IPO lockup periods for ServiceTitan (TTAN) and CoreWeave CRWV come. Those transactions should translate into dividend payments to shareholders given SuRo’s business development corporation status. As the IPO market improves, we’re likely to see other companies in SuRo’s investment portfolio go public or be acquired.

On Thursday, we raised our price target for Costco COST shares to $1,200 from $1,150 and later that day boosted our target for Axon shares to $825 from $750. In both cases, we maintained our Two ratings. On Friday, we bumped up our price target for Palantir shares to $140 from $130 following a new partnership win for the company’s commercial business. As we made that move, we reiterated that we still plan on revisiting our PLTR target following the company’s next AIPCon event.

Now, let’s see what Wall Street and others had to say about Pro Portfolio holdings this week…

Adweek reports Advertisers are shifting millions of dollars in ad budgets, particularly in connected TV, from Trade Desk's TTD demand-side platform to Amazon.

China Renaissance initiated coverage of Marvell shares with a Buy rating and a $110 target.

JPMorgan lifted its Meta target to $735 from $675 and upped its Amazon AMZN target to $240 from $225.

BofA reset its Amazon price target at $248, up from $230.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, June 2: The Atlanta Fed’s GDP Model Did What?

Tuesday, June 3: How Our Moves in 2 Positions Demonstrate Portfolio Strategy

Wednesday, June 4: TheStreet Stocks & Markets Podcast #8: Common Sense Investing With David Miller

Thursday, June 5: What's Driving the S&P 500 to Multi-Month High?

Friday, June 6: Why We're Nicely Ahead of the S&P 500

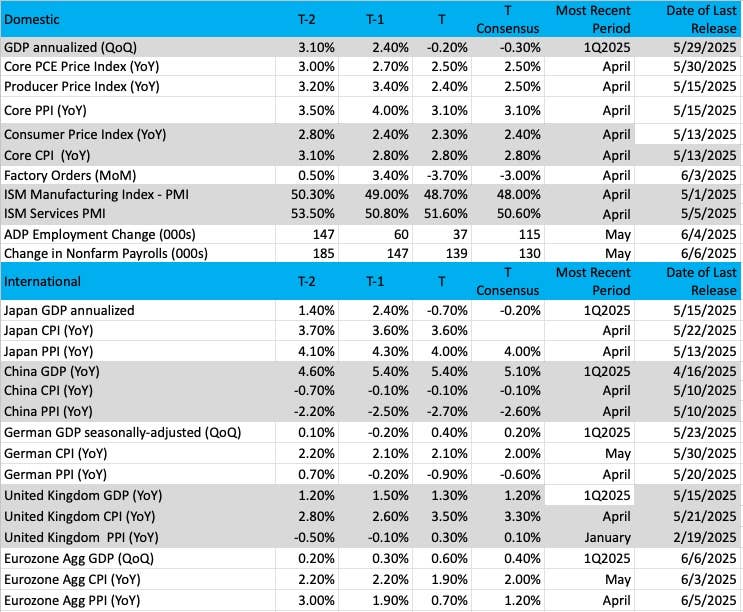

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

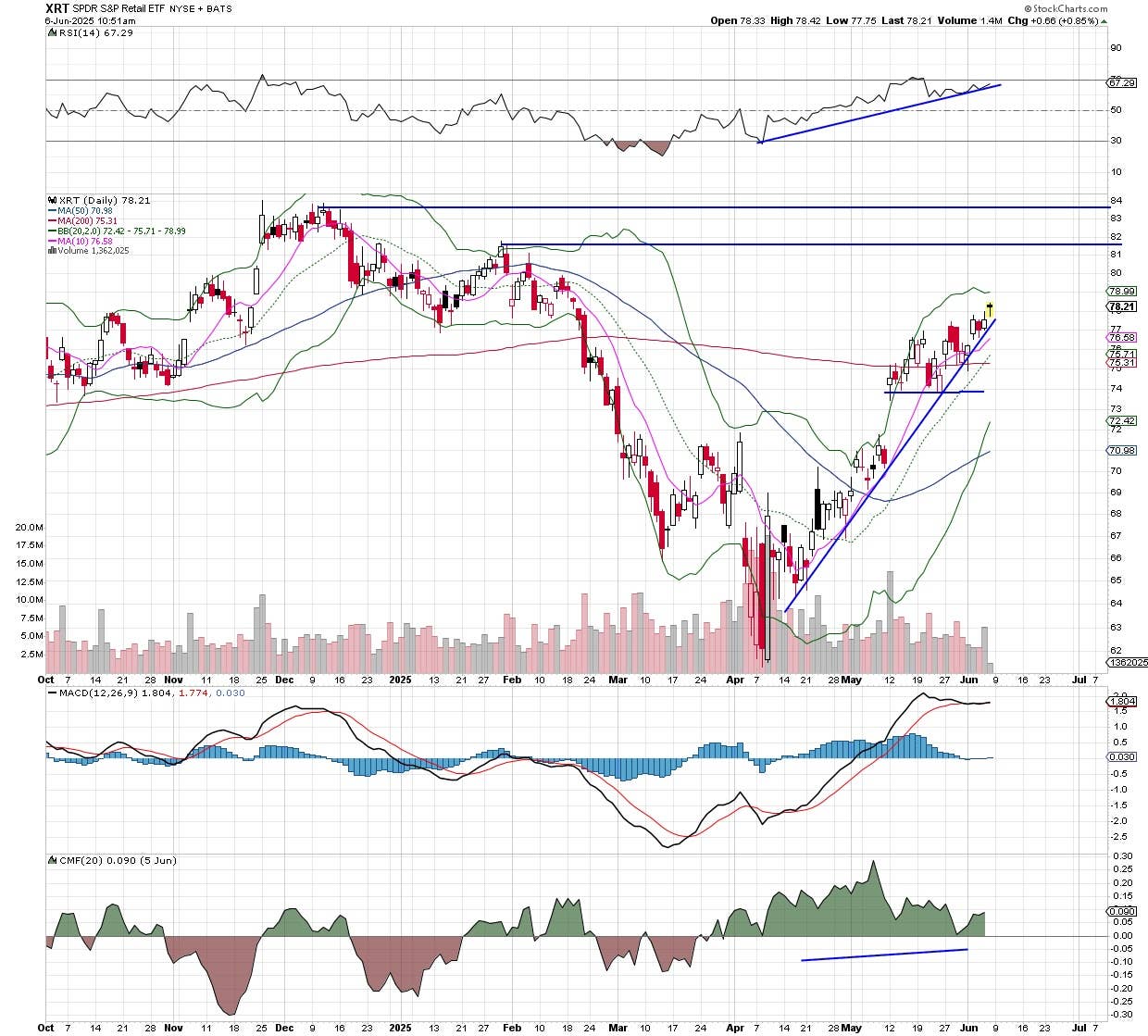

Chart of the Week: SPDR S&P Retail ETF

With the uncertainty over tariffs acting as a cloud over the stock market, it has become a direct target for retail names. We have heard from several retailers, such as Lululemon LULU this week, complaining about consumers not purchasing products for this very reason, and while this company did beat estimates, they lowered guidance for the rest of the year.

Other companies like Walmart WMT have talked about passing those tariff taxes onto the consumer, for which President Trump lashed out against them. Yet some firms have taken steps to manage the situation and have plans to deliver strong earnings regardless of the consequential tariffs. We’ll have to see how this all plays out.

We like to track retail names through an ETF. There are two relevant ones, in our view, the VanEck Retail ETF RTH and the SPDR S&P Retail ETF XRT. RTH includes several of the big-named retailers, but they have a heavier weighting on the ETF and thus an undue influence. Names like Amazon AMZN, Costco COST, Walmart, and Home Depot HD make up 44% of the RTH. It is not a good overall view of the sector, in our opinion. A better look at the retail group comes from XRT shares, which are more distributive in weight and represent more of the entire sector's performance.

The chart of the XRT, below, shows a massive move up from the April lows. Many of the S&P sector groups mirror this move on the XRT. What is notable on the chart is the huge gap in mid-May that has held nicely in place. A series of higher highs, and higher lows is our textbook definition of an uptrend, and with strong volume trends (bullish) this does not appear to be ending.

The ETF is only about 10% away from an all-time high which can be achieved if the S&P 500 makes a run to its highs, only about 2.6% away at current levels. Money flow in the XRT remains bullish; the ETF has recently cleared some big moving average resistance and sees the next objective around $81.

Other charts we shared with you this week were:

Monday, June 2: S&P 500 - Market Strives for 'Elusive Channel' Amid Big Swings

Monday, June 2: Axon Enterprise (AXON) - Axon Bases in the Right Spot

Tuesday, June 3: Universal Display (OLED) - Universal Display Quietly Turns Bullish

Wednesday, June 4: SuRo Capital (SSSS) - Our Newest Holding Has an Ace in the Hole

Thursday, June 5: Amazon (AMZN) - Amazon Is Starting to 'Get Charged Up'

The Week Ahead

When we return from the weekend, we’ll see the next update from the Atlanta Fed’s GDPNow Model on Monday, June 9. The most recent figure from this rolling model pegged current quarter GDP at 3.8% as of Thursday, June 5. However, based on what was revealed in the May Employment Report, we’re likely to see that number revised higher.

We also have the May CPI and PPI reports on Wednesday and Thursday next week. Based on the aggregate inflation data points collected so far for May, we do not foresee any meaningful progress on that front in next week’s data, and we could very well see those figures come in higher than consensus forecasts. Should that be the case, it would be another reason for us to think the Fed could forecast one less rate cut later this month than it did in March.

Speaking of the central bank, it enters its latest quiet period ahead of its two-day monetary policy meeting that concludes on June 18. With no central bankers making the rounds, the market will be left to its own devices to read the tea leaves of those inflation reports and other data making its way to us next week. Of course, we will continue to follow the data and let it “talk to us.”

Late Friday, President Trump said that Treasury Secretary Scott Bessent and two other Trump administration officials will meet with their Chinese counterparts in London on Monday for renewed trade talks. We’ll follow these meetings closely, but reiterate that headlines are one thing, but firm deals, and details are the ones that matter.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, June 9

· Wholesale Inventories – April (10:00 AM ET)

· Consumer Inflation Expectations – May (11 AM ET)

Tuesday, June 10

· NFIB Small Business Optimism Index – May (6:00 AM ET)

Wednesday, June 11

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Consumer Price Index – May (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Treasury Budget – May (2 PM ET)

Thursday, June 12

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Producer Price Index – May (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, June 13

· University of Michigan Consumer Sentiment Index (Prelim) – June (10:00 AM ET)

International

Monday, June 9

· China: Inflation Rate, Import/Exports – May

· Japan: Eco Watchers Survey & Outlook - May

Wednesday, June 11

· Japan: Machine Tool Orders – May

Thursday, June 12

· UK: GDP, Industrial & Manufacturing Production - April

Friday, June 13

· Japan: Industrial Production & Capacity Utilization – April

· Eurozone: Industrial Production - April

Hard to believe, as we stare down the final three weeks of the current quarter, but there are still several companies poised to report their quarterly results next week. As they do, we will continue to mine their results, comments, and guidance, connecting the dots back to the Pro Portfolio as it makes sense. The same goes for the next round of investor conferences next week, which include the DA Davidson Consumer & Technology Conference, Nasdaq Investor Conference, Rosenblatt Technology Conference, and the Morgan Stanley US Financials Conference.

Next week also brings a few other events that we will be focused on. One of those is Apple’s WWDC 2025 keynote on June 9, and in Friday’s video, we shared what we will be looking to hear. In the same video, we also explained why we are interested in the June 10 IPO lockup expiration for ServiceTitan (TTAN) shares given our new position in SuRo Capital SSSS. And with the growing momentum in the IPO market following this week’s successful offerings from Circle (CRCL) and Omada Health (OMDA), should we see that trend continue with the Chime (CHYM) IPO next week, we may need to revisit our price targets for Morgan Stanley MS and Bank of America BAC.

Here's a closer look at the earnings reports coming at us next week:

Monday, June 9

· Close: Calavo Growers (CVWB), Casey’s General Store (CASY)

Tuesday, June 10

· Open: JM Smucker (SMJ), United Natural Foods (UNFI)

· Close: Dave & Buster’s (PLAY), GameStop (GME)

Wednesday, June 11

· Open: Chewy (CHWY), SailPoint (SAIL)

Thursday, June 12

· Close: Adobe (ADBE)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.