Weekly Roundup: Trading Opportunistically as S&P Continues Hitting Record Levels

With a big week ahead of us, signals point to an overbought and complacent market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market continued to chug higher this week, with the S&P 500 and Nasdaq Composite once again hitting new record closing levels along the way. TheStreet Pro Portfolio more than participated in the week's move, which was fueled by solid corporate earnings, trade deal optimism following President's Trump’s deal with Japan, and indications that the economy and job creation hummed in July. We’ll add to that the lack of fireworks following Trump’s visit to the Fed Thursday afternoon, but we continue to think his calls for the Fed to dramatically lower interest rates will fall on deaf ears. We say that given the inflation findings of S&P Global’s Flash July PMI data.

As much as we’re enjoying the continued gains in the Pro Portfolio and the larger stock market, we recognize the market can remain in overbought territory for an extended period of time. For newer readers, we’re using the relative strength index (RSI) levels for the S&P 500 and Nasdaq Composite, which are both well over 70, to label those market indexes as overbought. At the same time, over the last few days, the Volatility Index has fallen to levels that are typically synonymous with extreme market complacency.

One interpretation of that combination — a complacent and overbought market — is that it’s arguably “priced to perfection.” When we’ve seen that in the past with the market or individual stocks, it usually means everything and then some has to go right for the market or that stock to move higher. Viewed through a different lens, that means an unexpected turn or underwhelming results can take some of the wind out of its sails and spur profit-taking among more short-term oriented traders.

Looking at the S&P 500, roughly 20% of its weighting is reporting next week, in the form of Microsoft MSFT, Amazon AMZN, Meta META, and Apple AAPL. Those results and updated guidance, which are largely expected to be positive, will help determine if the market’s next move is higher or lower. That’s not to say we won’t be focusing on other earnings reports out next week, we will, and you should expect us to continue connecting dots back to the Portfolio’s holdings.

Another likely influencing factor on the market will be what comes to pass in terms of trade deals, their terms and tariffs, as Trump’s August 1 deadline comes next Friday. The president is on a bit of a roll with the trade deals he announced, but given the size of U.S. imports from Canada, Mexico, China, and the European Union, those deals and their terms will be more impactful when it comes to removing market uncertainty.

To those two potentially market-moving events, we also have the Fed’s July policy meeting announcement on Wednesday. Few, if anyone, expect the Fed to deliver a rate cut following that meeting, and based on what we saw in the Flash July PMI data from S&P, we are not expecting overly dovish comments from Fed Chair Powell. While Trump and Powell seem to have made an uneasy truce late this week, if we’re right about Powell’s forthcoming comments, we could see Trump renew his attacks on the Fed Chair.

Recognizing those potential obstacles in front of us, we’ll be taking them one at a time, keeping our long-term view intact but looking to capitalize on near-term opportunities. We did some of that this week with American Express AXP, TJX Companies TJX, and Axon Enterprise AXON, and all three finished Friday above those nip-and-tuck purchase prices.

Over the weekend, we’ll have another basket of "signals" to share with you, the same kind of findings that kept us bullish on AI adoption and prospects for stronger data center capex levels. Sunday, we have our next collection of articles and streams that have caught our attention. And when we return from the weekend, we’ll share an updated table for the Portfolio’s holdings, their latest consensus EPS expectations, RSI levels, and other usual metrics.

With that, we wish you a wonderful and peaceful weekend. Stay cool. See you on Monday!

Catching Up on the Pro Portfolio This Week

The Pro Portfolio kept pace with the S&P 500 and outperformed the Nasdaq Composite on a week-over-week basis. Strong gains in shares of United Rentals URI and Labcorp LH led the way, but other outperformers included Elastic ESTC, Eaton ETN, Alphabet GOOGL, Palantir PLTR, and Vulcan Materials VMC. Those gains were offset by declines from Dutch Bros BROS and Axon Enterprise AXON, and, as we’ll get to below, we picked up more shares of both this week.

We made several opportunistic moves with the Portfolio this week, beginning with our decision on Monday to add more shares of American Express AXP and TJX Cos. TJX. On Thursday, we bought additional shares of Costco COST and Dutch Bros using recent share price weakness, oversold conditions, and technical support levels to our advantage. The same day, we also picked up more Axon shares given the number of supporting points for AI adoption from earlier in the week, which, combined with the recent pullback in the stock, made for an easy trigger to pull. Our timing was pretty good as we picked up those AXON at $698.02, and it closed the week notably higher.

Following those moves, the Portfolio’s cash position stood at ~10% as we headed into the weekend. With the S&P 500 and Nasdaq Composite at or near record levels and well into overbought territory, we will continue to pick and choose spots to build out existing positions as well as add any new ones to the Portfolio.

Next week we’ll get our first dividend payment from SuRo Capital SSSS. When we started the position and then added more shares to the Portfolio, we explained why we are taking a total return view with this position. Barring any changes to our SSSS share count, we should see the Portfolio’s cash position credited $3,425 to reflect SuRo’s July 31 quarterly dividend payment of $0.25 per share. We’re pointing this out ahead of time to avoid any confusion. SuRo is expected to pay additional dividends as it monetizes its investment portfolio, and that means we are inclined to remain owners.

In addition to this week’s buying activity, we also made several price target adjustments. On Thursday, we upped our price target on ServiceNow NOW to $1,200 from $1,100 and raised our Alphabet GOOGL target to $220 from $200. But as we made that second adjustment, we also downgraded GOOGL shares to a Two rating from One. On Friday, we bumped up our Labcorp price target to $300 from $265, and reset our United Rentals target at $950, up from $800. As more of the Portfolio’s holdings report their quarterly results and share their updated view on H2 2025, we’ll revisit their price targets as necessary.

There were a few other developments this week that we wanted to share with you. While Bank of America BAC announced an increase to its quarterly dividend a short while ago, on Wednesday, its Board authorized a new $40 billion common stock repurchase program, effective August 1, to replace the company's current program, which will expire on that date.

On Friday, Bloomberg reported that ServiceNow inked a five-year deal with Google for more than $1 billion in cloud computing services. That adds some color around a Thursday SEC filing in which ServiceNow disclosed $4.8 billion in total cloud services commitments through 2030. It also explains why Google raised its 2025 capital spending to $85 billion from $75 billion and bodes well for another year of elevated capex in 2026. That suggests the AI and data center arms race will continue, reinforcing our bullish stance on Nvidia NVDA, Marvell MRVL, and other Portfolio holdings.

Now let’s see what Wall Street had to say about the Portfolio’s holdings over the last few days:

RBC Capital raised its Alphabet target to $220 from $200. Joining RBC and us at the $220 level was Needham, while Oppenheimer took its price target to $235 from $220.

Amazon shares were given a new price target of $265 at BofA, up from $248. Scotiabank made a more aggressive move, putting its target at $275, up from $250 ahead of the company’s June-quarter earnings report next week.

Ahead of its earnings report next week, Evercore ISI boosted its Microsoft target to $545 from $515 as it expects a favorable margin guide for the coming quarters. The odds of such a guide are favorable as Microsoft monetizes added cloud capacity. Loop Capital also lifted its MSFT target to $600 from $550.

Morgan Stanley increased its Labcorp price target to $306 from $283 on Friday, reiterating its Overweight rating. UBS upped its target to $305 from $282, Baird reset its at $302, while Truist lifted its target to $310 from $290.

Piper Sandler initiated coverage of Palantir PLTR with an Overweight rating and $170 price target. The firm believes Palantir can grow into a $24 billion revenue run-rate by 2032 due to market share gains in two one trillion-dollar total addressable markets — government and U.S. commercial. In keeping with our Two rating, Piper’s message is to be patient and buy PLTR shares on weakness.

UBS raised its target on the shares of Qualcomm QCOM to $165 from $145, noting a “modest upside bias” for the company’s June-quarter results.

ServiceNow saw its price target at RBC move to $1,200 from $1,100, like we did, while DA Davidson reset its target at $1,250, up from $1,150. BofA and Needham also joined us at the $1,200 level.

United Rentals caught several price target increases late in the week, including KeyBanc taking its target to $960 from $865, and BofA boosting theirs to $900. Citigroup and JPMorgan both raised their URI targets to $1,000.

This Week's Portfolio Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and Stocks &Markets Podcast. If you happened to miss any of them, here are some helpful links:

Monday, July 21: The Weekend’s Big Cyberattack Is Good News for This Holding

Wednesday, July 23: Stocks & Markets Podcast: Secrets of Venture Capital With SuRo Capital's Mark Klein

Wednesday, July 23: This Holding's CEO Highlights Our Play

As connectivity and construction issues subside, we expect to be back in the swing of things when it comes to Portfolio videos early next week.

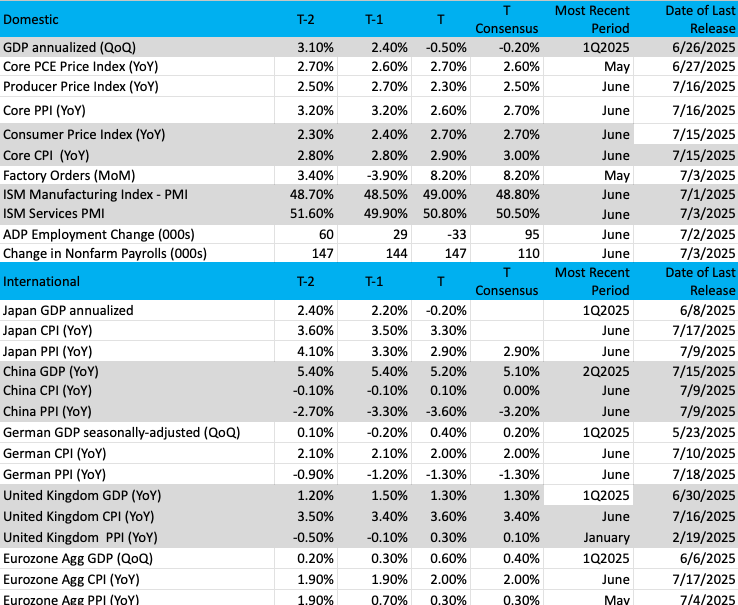

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

Chart of the Week: Roundhill Magnificent Seven ETF

The coming week is a big one for the vaunted Magnificent Seven stocks – otherwise known as the "trillion-dollar club." Earnings will be released from four of the seven names (Apple, Amazon, Meta, and Microsoft), which are all in TheStreet Pro Portfolio. Last week, we heard from two of the Mag 7 names (Alphabet and Tesla) to a mixed response. But next week, with the biggest of these names reporting (ex Nvidia), we should see quite a bit of movement as implied volatility is elevated (as usual in front of earnings).

These four names (MSFT, AMZN, META, AAPL) have all risen nicely over the past few months and may be due for a rest. Will the earnings report for each be a signal that stocks should be sold on the news? It might be, but we suspect that any sizeable dip is going to be bought aggressively, so be ready with some ammunition.

As for the chart of the Mag 7 all in one, we reference the Roundhill Magnificent Seven ETF MAGS. This chart shows a strong uptrend, and higher highs and higher lows, which is our textbook definition of an uptrend. But this ETF is up nearly 50% since the lows in April, which shows you how strong these stocks have moved. Further, the Nasdaq 100, for which these seven names have the heaviest weighting, is also up a healthy 40% since the lows in early April.

The MAGS is quite overbought, but remember that it is just a condition and not a signal. Stocks and ETFs can remain overbought for a long period of time, more than you think they can. Stochastics are strong and embedded, which means dip buyers are active on any pullback. This serves to limit any downside move outside of any extraordinary news.

Money flow is strong, the Chaikin indicator at the bottom of the chart is recently hitting new highs, volume trends are bullish, and the candles are blue and have been for months. The only care in the world is if these companies break down hard following earnings news. We don’t expect that to happen this time around.

Other charts we shared with you this week were:

Monday, July 21: S&P 500 - What More Do You Need to Prove the Trend?

Monday, July 21: Universal Display (OLED) - Good Time to Buy This Tech Holding?

Tuesday, July 22: Meta (META) - Meta Pulls Back Just in Time

Wednesday, July 23: Broadcom (AVGO) - Is Broadcom Finally Near a Buy Point?

Thursday, July 24: Bank of America Is a Name We Can 'BAC'

The Week Ahead

When you review the list of economic data and earnings reports coming at us below, you’ll notice a rather slow start to what will be a busy and potentially critical week for the stock market. While the docket on Monday is extremely light, the flow of data warms up on Tuesday and by Wednesday we get into the thick of things with the first reading of Q2 2025 GDP, the outcome of the Fed’s next policy meeting, more big tech company earnings. On Friday, the July Employment Report and ISM Manufacturing PMI data arrive. That’s right, once again the data scales tip toward the end of the week.

Based on the data received in recent months and pairing that with what we saw in that Flash PMI data, the odds of a Fed rate cut next week are extremely low. During his post-policy announcement presser, we would be surprised if Fed Chair Powell’s tone skewed more dovish. That could put him at renewed odds with President Trump, who on Friday said he believes Powell will start lowering interest rates. With more companies citing tariffs and pressure on input costs as reasons to lift prices, we suspect Powell will reiterate recent comments about following the data as the Fed determines when to next cut interest rates.

Next week ends on August 1, the self-imposed deadline for Trump's trade deals. As of Friday, the Trump administration is scheduled for another round of trade talks with China, and the market is waiting to see what develops on the trade or tariff front with Canada, Mexico, and the European Union. Closing out this week, Trump commented that the EU may need to do a “buy down” similar to Japan, establishing a $550 billion fund to make investments in the U.S. Alongside that comment, Trump also intimated he is “not having much luck” with Canada when it comes to trade talks. With a week to go, a lot can happen. We’ll assess any tariff announcements, trade deals and their terms and reposition the Portfolio as necessary.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, July 29

· Advanced International Trade, Retail Inventories, Wholesale Inventories – June (8:30 AM ET)

· FHFA Housing Price Index – May (9:00 AM ET)

· S&P Case Schiller Home Price Index – May (9:00 AM ET)

· Consumer Confidence – July (10:00 AM ET)

· JOLTS Job Openings & Quits - June

Wednesday, July 30

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· GDP – Q2 2025 (8:30 AM ET)

· Pending Home Sales – June (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Rate Decision – July (2 PM ET)

Thursday, July 31

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Personal Income & Spending, PCE Price Index – June (8:30 AM ET)

· Employment Cost Index – Q2 2025 (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, August 1

· Employment Report – June (8:30 AM ET)

· S&P Global Final Manufacturing PMI – July (9:45 AM ET)

· ISM Manufacturing Index – July (10:00 AM ET)

· Construction Spending – June (10:00 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – July (10:00 AM ET)

International

Monday, July 28

· China: Industrial Profits - June

Tuesday, July 29

· Eurozone: ECB Consumer Inflation Expectations – June

· UK: BoE Consumer Credit - June

Wednesday, July 30

· Germany: Retail Sales – June

· Germany: Flash GDP – Q2 2025

· Eurozone: Flash GDP – Q2 2025

· Eurozone: Consumer Confidence & Inflation Expectations – July

· Canada: Bank of Canada Interest Rate Decision

Thursday, July 31

· Japan: Retail Sales, Industrial Production – June

· Japan: Bank of Japan Interest Rate Decision

· China: NBS Manufacturing & Non-Manufacturing Indices – July·

Friday, August 1

· Japan: S&P Global Final Manufacturing PMI - July

· China: Caixin Manufacturing PMI – July

· Eurozone: HCOB Final Manufacturing PMI – July

· Eurozone: Flash Inflation Rate – July

· UK: S&P Global Final Manufacturing PMI - July

We have another step up in the number of companies reporting earnings next week. The same goes for the number of Portfolio companies reporting, including ones that are also key constituents in the S&P 500 and the Nasdaq Composite. With the market punching into new territory this week, the outlook for the back half issued by Apple AAPL, Microsoft MSFT, Amazon AMZN, and Meta META will tell us if an overbought market can push even higher in the short term.

Outside of those Portfolio holdings and key market index members, we also have quarterly results on tap from Waste Management WM, Vulcan Materials VMC, and Universal Display OLED. In between all of those reports, we’ll continue to cross-reference comments and forecasts from others reporting next week, tying them back to the Portfolio’s holdings.

Here's a closer look at the earnings reports coming at us next week:

Monday, July 28

· Close: Nucor (NUE), Rambus (RMBS), Waste Management (WM)

Tuesday, July 29

· Open: American Tower (AMT), Celestica (CLS), Corning (GLW), Herc Holdings (HRI), JetBlue Airways (JBLU). Norfolk Southern (MSC), PayPal (PYPL), Polaris Industries (PII), Procter & Gamble (PG), UnitedHealth (UNH), UPS (UPS)

· Close: Avis Budget (CAR), Booking Holdings (BKNG), Caesars (CZR), Cheesecake Factory (CAKE), Lending Club (LC), Logitech International (LOGI), Mondelez International (MDLZ), PPG Industries (PPG), Qorvo (QRVO), Starbucks (SBUX), Visa (V)

Wednesday, July 30

· Open: Check Point Software (CHKP), GE Healthcare (GEHC), Hershey (HSY), Illinois Tool Works (ITW), Kraft Heinz (KHC), Radware (RDWR), VF Corp (VFC), Wingstop (WING)

· Close: American Water Works (AWK), Applied Digital (APLD), Carvana (CVNA), eBay (EBAY), Equinix (EQIX), F5 Networks (FFIV), Ford Motor (F), Hologic (HOLX), Lam Research (LRCX), Meta (META), Microsoft (MSFT), Pilgrim’s Pride (PPC), Qualcomm (QCOM), Robinhood (HOOD)

Thursday, July 31

· Open: AbbVie (ABBV), AGCO (AGCO), Anheuser-Busch InBev (BUD), Bristol-Myers (BMY), Canada Goose (GOOS), Comcast (CMCSA), CVS Health (CVS), InterDigital (IDCC), Lincoln Electric (LNC), Masco (MAS), Mastercard (MA), Peabody Energy (BTU), Shake Shack (SHAK), Terex (TEX), TreeHouse Foods (THS), Vulcan Materials (VMC)

· Close: Amazon (AMZN), Apple (AAPL), Clorox (CLX), Cloudflare (NET), Coinbase Global (COIN), Ingersoll-Rand (IR), KLA Corp. (KLAC), Universal Display (OLED)

Friday, August 1

· Open: Cboe Global Markets (CBOE), Chevron (CVX), Exxon Mobil (XOM), Kimberly Clark (KMB), Piper Sandler (PIPR)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.