Weekly Roundup: Tariffs and Inflation Bring Volatility and Fed Questions

Market volatility can be nerve-racking but, as we’ve seen, it can be filled with opportunity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market volatility see-sawed this week, something we can see in the Cboe Volatility Index (VIX), but the Fear & Greed Index continued to flash "Fear." While the week’s economic data showed the jobs market and overall economy remain on firm footing, the latest indications reaffirm the growing likelihood that inflation pressures are not receding, and wage pressures are rebounding. Mix in the pop in the year-ahead consumer inflation expectations and, as one might expect, that led to some sobering talk from a variety of Fed heads late this week

The final ingredients for that market stew were announced, but delayed tariffs on Mexico and Canada and fresh tariffs on China that were met with retaliatory measures. Tariff talk resumed on Friday with word President Trump will announce reciprocal trade tariffs next week. That weighed on the markets, largely erasing the midweek rebound that occurred when Trump delayed some tariffs and didn’t respond to China’s retaliatory measures.

Coming off Inauguration Day we shared our concern the market would have to adapt to President Trump’s tactic of using uncertainty to push forward certain aspects of his agenda. We saw this during his first term, and we see no reason it won’t be used in the current one, which means volatility is likely to be with us for a while. We had best get used to it — as well as to the high probability Sunday nights and Monday mornings will be full of uncertainty and volatility.

As it relates to the TheStreet Pro Portfolio, our playbook is clear. Be mindful of the market volatility and the market’s technical setup. Continue to focus on the data and fundamentals. Revisit opportunities to lock in gains, identify levels that make for more than favorable pickup points for existing positions, and do the same for potential new entrants. One of our more recent positions, the VanEck Uranium & Nuclear ETF NLR, is up nicely, reaffirming the thought that sometimes timing is everything.

And with that, we’ll remind you that while market volatility can be unnerving, it can also be helpful. The trick is to be prepared and that’s what we aim to be, and we’ll make sure you are as well.

Catching Up on the Portfolio This Week

After a week that started and ended with tariff concerns, the portfolio was down modestly but continued to have a nice year-to-date lead on the S&P 500. The continued increase in Dutch Bros BROS ahead of next week’s earnings report as well as gains in Meta META, Costco COST, Nvidia NVDA, and the VanEck Uranium & Nuclear ETF NLR were offset by declines in Alphabet GOOGL, Amazon AMZN, Universal Display OLED, and Eaton ETN.

In a week that started with President Trump imposing tariffs on Mexico, Canada, and China we called the shares of inverse ETFs ProShares Short S&P500 SH and ProShares Short QQQ PSQ back to the portfolio. As we explained in that trade alert to members, we opted for this course to help insulate the portfolio from near-term volatility without sacrificing its exposure to quality companies in what is likely to be a reactionary and turbulent market environment. While those new positions moved lower against an up market during the week, Friday’s market turbulence showcased our reason for adding them.

During the week, we boosted our price target for Costco following another robust monthly sales report. We also reiterated our Qualcomm QCOM price target given the progress we saw in its December quarter earnings report on management’s revenue diversification plan. Then on Friday did the same for Labcorp LH. We also shared our in-depth thoughts about Amazon’s December quarter results, guidance, and why we aim to be long-term shareholders.

Now let’s catch up on Wall Street’s actions on the portfolio’s holdings over the last few days:

Alphabet saw several price target cuts this week from Morgan Stanley, KeyBanc, UBS, and Piper Sandler to $208-$220 from $210-$225. We maintained our $210 target and discussed a potential spot for adding more shares.

RBC Capital lifted its Amazon price target to $265 from $255 while Deutsche Bank upped its to $287 from $275, and DA Davidson boosted its to $280 from $235.

Costco shares received multiple price target increases from Stifel, Loop Capital, Oppenheimer, and DA Davidson to $1,075-$1,130 from $900-$1,095.

Ahead of next week’s earnings report, Wedbush slapped an $80 target on Dutch Bros shares, up from $65.

Shares of Labcorp received a $293 target from Baird, while BMO Capital increased its target to $280 from $265.

Post quarterly earnings, TD Cowen upsized its Qualcomm price target to $195 from $180.

Argus Research lifted its Waste Management WM target to $245 from $240, while Citi increased its to $255 from $242.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, February 3: Why We're Adding Protection and What We're Watching

Tuesday, February 4: How the Outcome of Trump’s Conversation With Xi Will Impact Our Holdings

Wednesday, February 5: Alphabet, Microsoft's cloud misses highlights capacity problem

Thursday, February 6: NVDA & MRVL Will Stay Tech Winners; QCOM & GOOGL After Earnings

Thursday, February 6: LIVE on NYSE TV | Earnings, Stagwell, International Trade & More

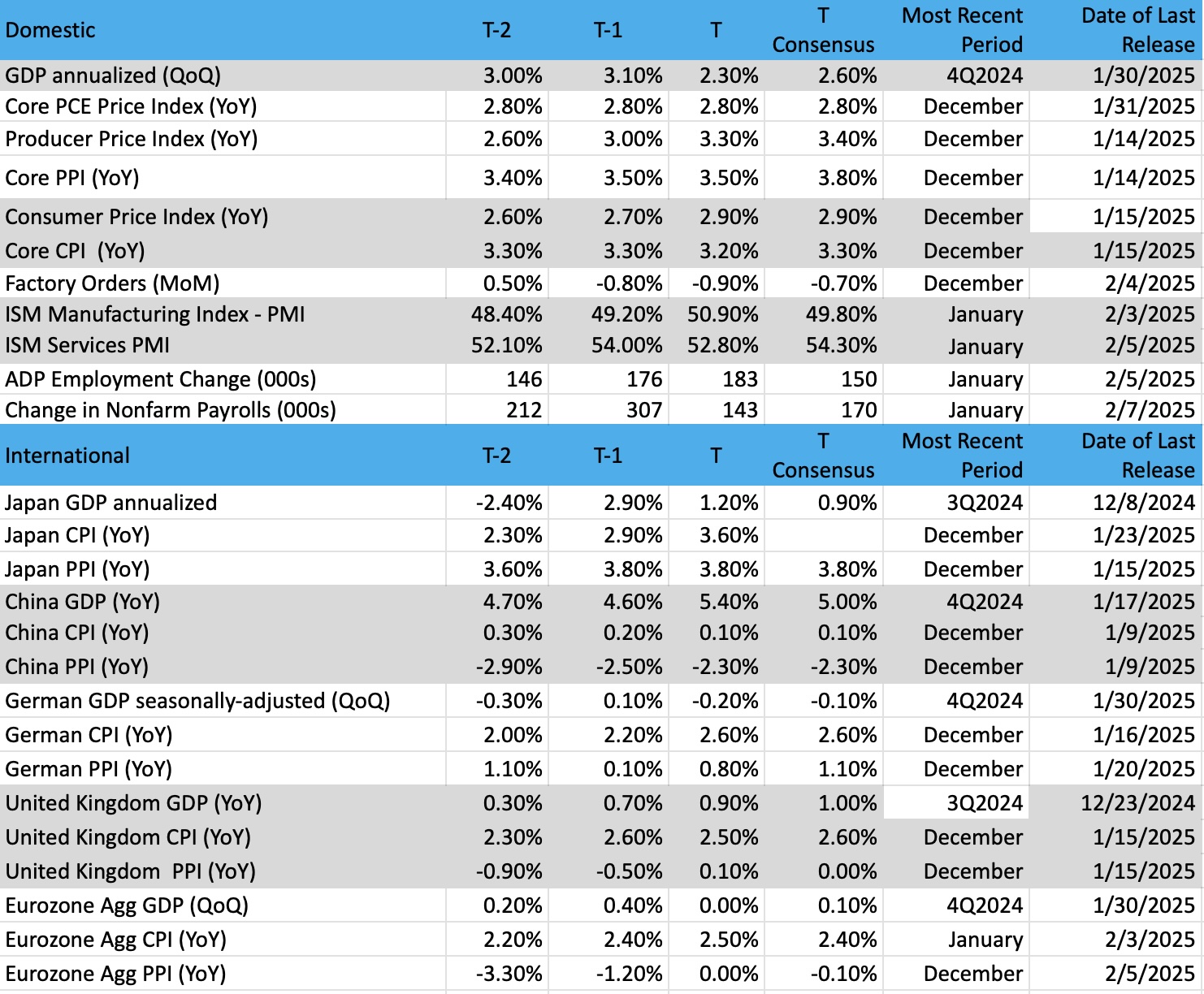

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: The 2-Year Treasury Yield

There has been quite a bit of discussion surrounding interest rates of late. For good reason, our economy is at a point where inflation is at an inflection point. Can the demon of high prices finally turn lower and make its way towards the Federal Reserve’s goal of 2% inflation, or are we simply stuck with higher prices?

To be sure, the committee is playing it with caution, preferring to rely on the generosity it showed late in 2024 with 100 basis points of rate cuts in the last four months of the year. That slashing of rates brought the funds rate down to 4.25%-4.5%, a familiar number. Why is that? It is where we have seen the 2-year and 10-year yields hover for the past couple of years (on average). What does that mean then? Basically, the supply and demand equation tells us short-term, medium- and long-term needs (funding) are priced similarly, and the risk-free rate of return is in line with the Fed’s borrowing rate.

The recent chatter from the Trump administration is it to work on reducing the long-term interest rate, which would be a monumental task given the U.S. has more than 38 trillion in debt and continues to roll parts of it day after day. The long end of the curve is a market-based product and while some argue it has been manipulated for years by the Federal Reserve, if there is not a large buyer present (other than dealers and sovereign countries) then this task of bringing rates down is difficult at best.

But looking at the chart of the 10-year and 2-year yield with the Fed funds, below, shows the similarity of the moves. A recent pop in the 10-year (in black, top) towards 5% caused some consternation in markets early in 2025 but since then the yield has backed off some. We see the 2-year yield (in red, top) has stabilized here at around 4.22% and continues to trade below the Fed funds rate, which is healthy.

Fed speakers have recently noted their hesitancy to cut rates further but were not insistent on tight policy if inflation starts coming down again. For now, they seem to be in wait-and-see mode. The long bonds as seen here might give us some clues as to when the committee is ready to cut, that is if yields continue to slide.

Other charts we shared with you this week were:

Monday, February 3: S&P 500 - S&P 500 Looks to Be Running Out of Steam

Monday, February 3: Qualcomm (QCOM) - A Tech Holding Rises to the Occasion

Tuesday, February 4: ProShares Short S&P 500 ETF (SH) - Don't Forget to Keep Some Market Protection

Wednesday, February 5: Elastic NV (ESTC) - This Holding Shows Good Flexibility

Thursday, February 6: Eaton Corp. (ETN) - How to Play a Name That's Not Bullish and Not Bearish

The Week Ahead

Looking ahead to next week, several factors are likely to influence how the market moves as we close out the first half of the current quarter. The known knowns include the January figures for the Consumer and Producer Price Indexes, back-to-back appearances by Fed Chair Powell, and the January Retail Sales report.

Inflation pressures continue to look at best, sticky, and in some cases inching higher. We’re basing that on the pricing data found in the January PMI reports, the wage gains identified in the January jobs data, and Friday’s preliminary take on year-ahead consumer inflation expectations. The response to the Friday findings led the 10-year Treasury yield to rebound and brought cautious comments from Fed Governor Kugler: “Recent progress on inflation has been slow and uneven, and inflation remains elevated. There is also considerable uncertainty about the economic effects of proposals of new policies.”

That tail end of Kugler’s comments reflects the announced and delayed tariffs on Mexico and China this week, and China’s retaliatory tariffs announced on Wednesday. Those developments and the potential for President Trump to announce tariffs on American imports equal to the rates that trading partners impose on American exports in the coming days set the stage for Powell’s comments on Tuesday and Wednesday. And as you can see below, Powell will be speaking after we get the January CPI data.

The combination of another leg up in tariffs and what is likely to be more hawkish than not commentary from the Fed Chair means we will remain owners of the SH and PSQ inverse ETFs heading into next week.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, February 10

· Consumer inflation Expectations - January

Wednesday, February 12

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Consumer Price Index – January (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, February 13

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Producer Price Index – January (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, February 14

· Retail Sales – January (8:30 AM ET)

· Import/Export Prices – January (8:30 AM ET)

· Industrial Production & Capacity Utilization – January (9:15 AM ET)

· Business Inventories – December (10:00 AM ET)

International

Monday, February 10

· China: Inflation Rate, Producer Price Index – January

· Japan: Eco Watchers Survey - January

Tuesday, February 11

· China: Loan Growth, Vehicle Sales – January

Wednesday, February 12

· Japan: Machine Tool Orders - January

Thursday, February 13

· UK: GDP – 4Q 2024· UK: Industrial Production, Manufacturing Production – December

· Eurozone: Industrial Production - December

Friday, February 14

· Eurozone: GDP, Employment Change – 4Q 2024

As you can see below, Dutch Bros BROS, The Trade Desk TTD, and Applied Materials AMAT are reporting next week. Combined with the coming inflation data, Powell's comments, and tariff developments, it is another busy week ahead.

We will still mine comments and insights from other companies as they report next week. We intend to focus on what McDonald’s (MCD) has to say about food inflation, tariffs, and currency headwinds. With Global Foundries (GFS), what are its 2025 capital spending plans and where does it see pockets of strength and weakness across its end market exposure?

With an eye toward our positions in American Express AXP and Mastercard MA, we’ll be interested in travel-related comments from Marriott (MAR), Airbnb (ABNB), and Lyft (LYFT), while capital spending comments will be our focus when Duke Energy (DUK) and Lincoln Electric (LECO) reports. The same goes for Digital Realty Trust (DLR) and Equinix (EQIX), and we expect those to sync up with 2025 capital spending comments for AI, cloud, and data center from Big Tech this week and last.

We’ll round out those insights with comments from Granite Construction (GVC), and Martin Marietta (MLM) as we get ready for quarterly results from Vulcan Materials (VMC) on February 18. And finally, we’ll be comparing comments on 2025 pricing action from Casella Waste (CWST) and Waste Connections (WCN) as we reflect on Waste Management’s WM recent earnings report.

We will also want to collect comments from companies about announced tariffs and their implications, and continue to be mindful of the dollar and currency headwinds.

Here's a closer look at the earnings reports coming at us next week:

Monday, February 10

· Open: McDonald’s (MCD), ON Semiconductor (ON), Rockwell Automation (ROK), Tower Semi (TSEM)

· Close: Harmonic (NLIT, Lattice Semi (LSCC)

Tuesday, February 11

· Open: AutoNation (AN), Coca-Cola (KO), GlobalFoundries (GFS), Marriott (MAR)

· Close: DoorDash (DASH), Lyft (LYFT), Welltower (WELL)

Wednesday, February 12

· Open: Kraft Heinz (KHC), Martin Marietta (MLM)

· Close: Casella Waste (CWST), Dutch Bros (BROS), Equinix (EQIX), Fastly (FSLY), Reddit (RDDT), Robinhood Markets (HOOD), The Trade Desk (TTD), Waste Connections (WCN)

Thursday, February 13

· Open: Ceva (CEVA), CyberArk (CYBR), DataDog (DDOG), Duke Energy (DUK), Granite Construction (GVA), Lincoln Electric (LECO)

· Close: Airbnb (ABNB), Applied Materials (AMAT), Coinbase Global (COIN), Digital Realty Trust (DLR), DraftKings (DKNG), Motorola Solutions (MSI), Nu Skin (NUS), Roku (ROKU)

Friday, February 14

· Open: American Axle (AXL), Sensient (SXT), TreeHouse Foods (THS).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.