Weekly Roundup: 'Software-mageddon' Takes the Market on a Wild Ride

During a volatile week, we added to one holding, explained our view on software stocks, and saw sharp rebounds in our EPS Diplomats model and several other positions.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

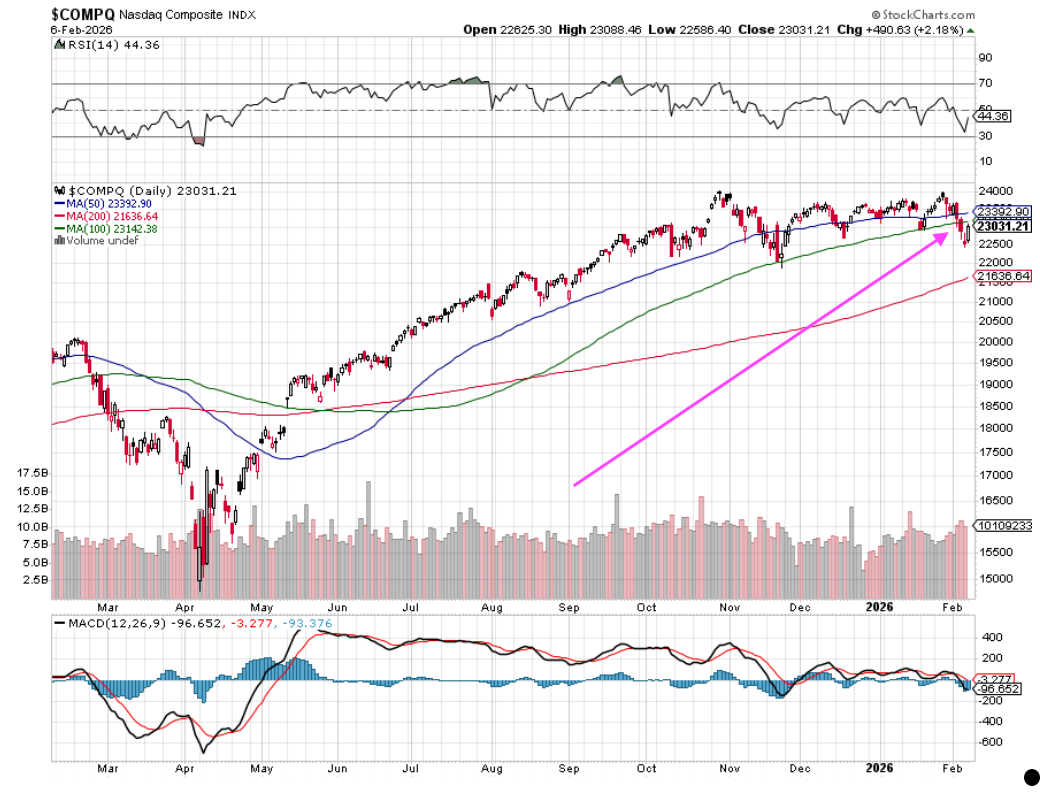

If we had to characterize the last five trading days in just a few words we'd say it's been “a wild ride.” We say that given the cumulative move lower for the S&P 500 over the last several trading days, but especially the 5.5% fall in the Nasdaq Composite between the market close on January 28 and Thursday, February 5. On Thursday, we shared that we were closely watching the S&P 500 relative to its 100-day moving average, which was the next layer of support to challenge the market selloff.

With Friday’s sharp rebound, which pushed the Dow Jones Industrial Average past 50,000 for the first time, the S&P 500 managed to recover its losses and move well past its 50-day moving average near 6886. Early next week, we’ll want to see if that support level holds and what that could mean for the market. However, even after Friday’s more than 2% jump in the Nasdaq Composite, it still finished the week down ~1.6% and, as we can see in the chart below, beneath its 100-day moving average. The drivers behind that took a toll on the Pro Portfolio with the declines in Amazon (AMZN) , Axon (AXON) , Meta (META) , ServiceNow (NOW) , Microsoft (MSFT) , and Palantir (PLTR) .

On Friday, we explained why we are inclined to remain long AMZN shares, and our position on META shares hasn’t changed since the prior week. The catalyst that led us to pick up more AXON speaks to the expanding use of body cameras and the higher margin services business, which should continue to drive favorable operating leverage. That keeps us bullish on AXON.

We also discussed this week why, even after the pounding that software stocks have taken, we’re not throwing in the towel just yet. We shared sobering comments about what has come to be called "Software-mageddon" from Nvidia’s (NVDA) Jensen Huang, Advanced Micro Devices' (AMD) Lisa Su, and ARM (ARM) CEO Rene Haas, as well as why, to use some of their words, it is “illogical” and a “micro-hysteria.” To that, we’ll add the severe oversold condition for NOW and AXON, the oversold one for MSFT shares, and PLTR shares narrowly escaping that condition on Friday.

We recognize it may take some time for these shares to rebound, but we could also see a quick snapback given those RSI readings. As we have done in the past, we will follow the money, and based on rising backlog, total contract, and RPO levels, we should see higher stock prices for these companies. We’ll watch call option flow and other indicators, including upcoming conference appearances, and yes, we are considering putting some of the Portfolio’s capital to work.

Focusing solely on those six beleaguered stocks, one can miss the double-digit move in United Rentals (URI) this week and mid-to-high-single-digit gains from Apple (AAPL) , Bank of America (BAC) , Costco (COST) , and Eaton (ETN) . Others in the Portfolio, including American Express (AXP) , Labcorp (LH) , Morgan Stanley (MS) , TJX (TJX) , Welltower (WELL) , and Waste Management (WM) , were outperformers this week.

Enjoy the weekend, Saturday’s Signals alert, where we share 23 signals across 8 of the strategies we use to manage the Portfolio, and, of course, the Super Bowl, its commercials, and all the fixings.

See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

We largely stayed on the sidelines during the week as the market continued to move lower through Thursday, dragging many stocks in and out of the Portfolio with it. We did use the announcement that the Department of Homeland Security will expand the use of body cameras nationwide, and the oversold condition in Axon (AXON) shares to pick up more for the Portfolio.

Given our discussion for the bulk of the Portfolio’s holdings above, we’ll skip to the EPS Diplomats. While the move lower in gold and silver prices took some wind out of the Diplomats last week and early this week, the rebound in gold prices and the outsized gains this week for shares of Lumentum (LITE) and SiTime Corp. (SITM) led the basket to regain a considerable amount of the ground it lost last week. Closing out the first five weeks of 2026, this basket is up ~9%.

Barring any buying activity early next week, we should see a modest increase in the Portfolio’s cash position as we book dividend payments from American Express (AXP) , Apple (AAPL) , Costco (COST) , and Morgan Stanley (MS) .

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during this "wild ride" of a week for the market:

Monday: In addition to Dutch Bros (BROS) joining the S&P 400, shares of ServiceNow (NOW) were added to the Goldman Sachs U.S. Conviction List, and the firm’s NOW price target of $216 was reiterated. Citi trimmed its United Rentals (URI) price target to $950 from $1,090, matching our price target for the shares. JPMorgan trimmed its American Express target by $10 to $375, while Truist revised its to $400. Piper Sandler reiterated its $600 target for Microsoft (MSFT) as well as its Overweight rating.

Tuesday: Baird upgraded shares of Palantir (PLTR) to Outperform from Neutral with a new $200 target, but Citi was the one that boosted its PLTR target to $260 from $235. Northland also upgraded PLTR shares, rating them a new Outperform with a $190 target, as did HSBC with a Buy and $205 target. Mizuho upped its Costco target to $1,065 from $1,000, putting it closer to our $1,100 target than not. Mizuho also increased its Alphabet (GOOGL) target to $400 from $365. Freedom Capital, the home of our good friend Jay Woods, lifted its Meta Platforms (META) target to $825 from $800

Wednesday: Morgan Stanley raised its Eaton (ETN) target to $425 from $405, which is just above our $420 target. RBC took its ETN target up to $407.

Thursday: JPMorgan lifted its Alphabet target to $395 from $385, Barclays took its to $360 from $315, Canaccord boosted its to $415 from $390, and Citi was in the middle of the pack with its increase to $390 from $350. Baird raised its Costco target to $1,100 from $1,100 following the company’s stellar January comp sales figures. Oppenheimer also took its COST target to $1,100, but from $1,050.

Friday: Citi lowered its Amazon (AMZN) target to $265 from $320, TD Cowen nudged its to $300 from $315 as did Morgan Stanley, and JPMorgan cut its to $265 from $305. JPMorgan inched its Labcorp (LH) price target to $319 from $317, reiterating its Overweight rating.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, February 2: CoreWeave CEO on Nvidia, AI, and Building the Cloud

Tuesday, February 3: Palantir’s Big Results and Our Latest Move With Axon

Thursday, February 5: Stocks & Markets Podcast: Inside the Market’s Next Move With Lindsey Bell

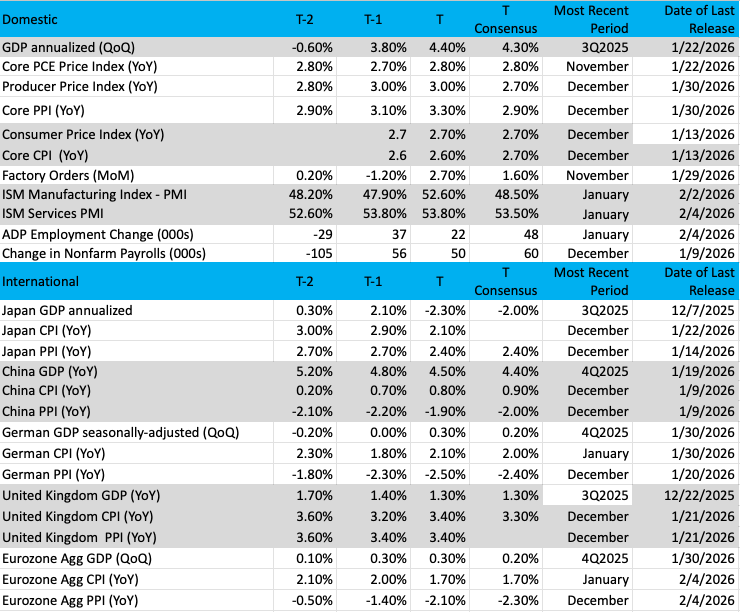

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

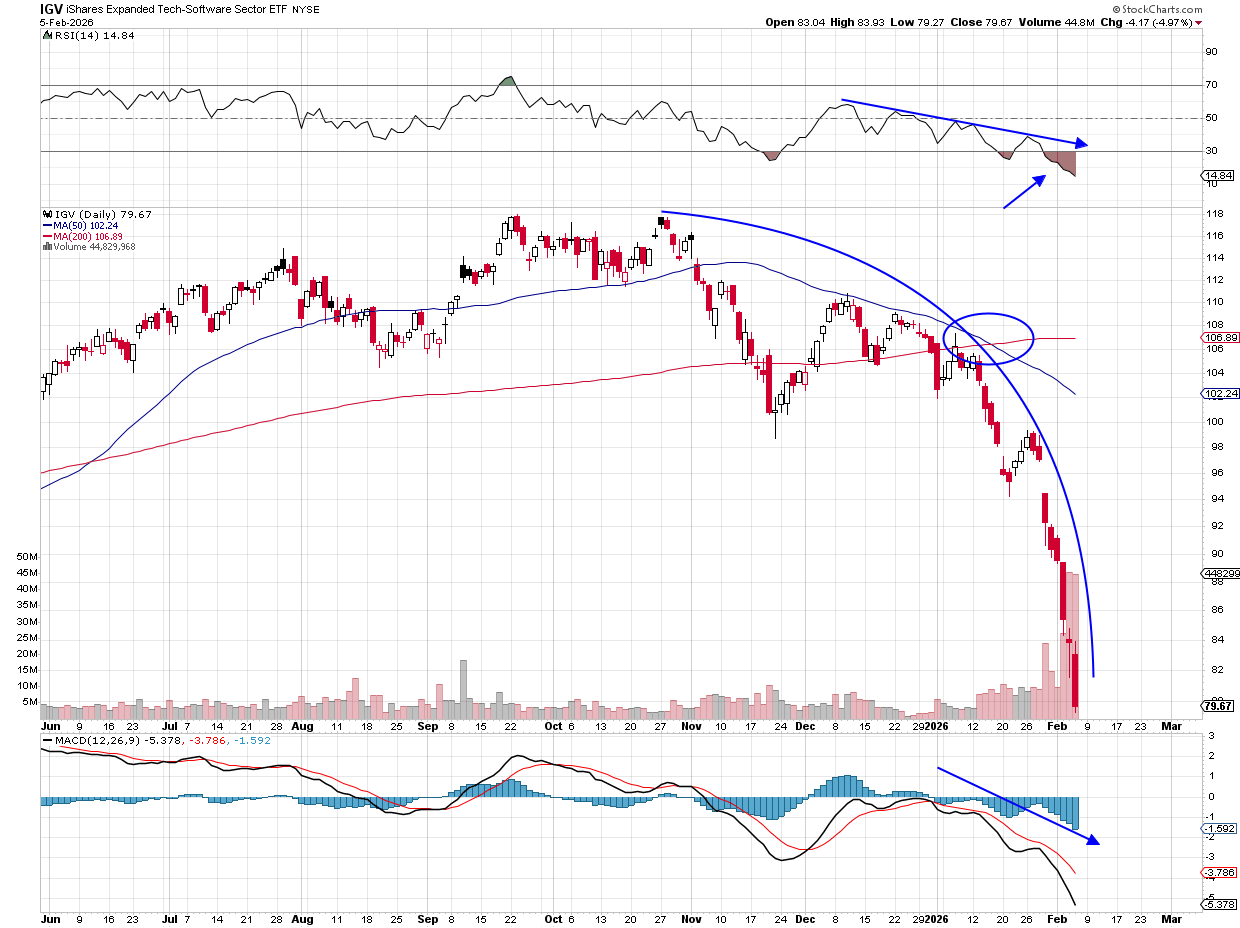

Chart of the Week: iShares Expanded-Tech Software Sector ETF (IGV)

Has there been anything uglier lately than the performance of the software companies? They just continue to go down day after day as the worry of AI taking over the software needs of companies has been making the rounds. Whether this is true or not is up for debate, but clearly, the fear of extinction is present.

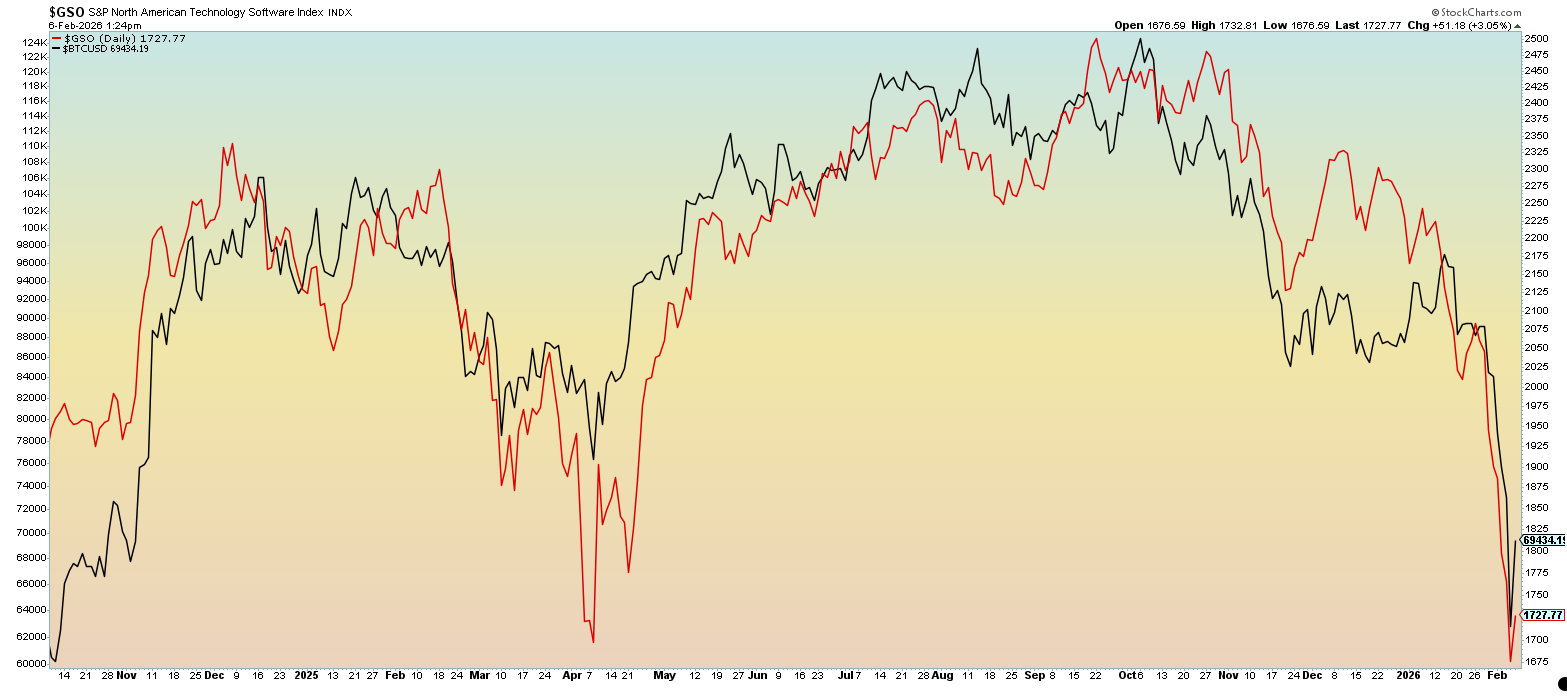

As a side note, I saw a chart (below) by Tom McClellan that showed a strong correlation between the GSO (virtually identical to the IGV) and Bitcoin. The dance steps are very similar, so if one wanted to find a reason for the weakness in software stocks, they might point a finger at Bitcoin.

Looking at the chart of (IGV) , below, you can see how much trouble the ETF has been in for a while, so no surprise the weakness is felt in the last few weeks. The down moves have been sharp and painful since the start of the new year, as optimism was abundant when the calendar turned.

Relative strength is clearly oversold here, and a bounce is likely, but with the downtrend firmly in place, there won’t be a bullish turn unless there is some solid base-building. That will take weeks of sideways movement. That might not be exciting, but bases need to be built to firm up support from big institutions. The start of the year saw a bearish death cross (50 crosses under the 200-day moving average, which is circled).

One positive on this chart might be the exhaustive volume of the last few days. When you see heavy selling and big volume show up during a strong downtrend, it often (not always) signals the bulls are waving the white flag and giving up. That is how a bottom is made. Make no mistake, the chart is bearish, and names such as Microsoft (MSFT) , ServiceNow (NOW) , and others are going to need to eventually lift the sector. We think it will happen slowly, but the rehabilitation needs to get underway. In other words, the selling needs to stop.

Other charts we shared with you this week were:

Monday, February 2: S&P 500 - Clock Is Ticking on Indecisive Market

Monday, February 2: Broadcom (AVGO) - Broadcom Is in a Surprisingly Nice Spot

Tuesday, February 3: Axon (AXON) - For Axon, It's Technicals Vs. Fundamentals

Wednesday, February 4: Eaton (ETN) - Eaton Could Start Stepping Up

Thursday, February 15: IAMGOLD (IAG) - Can This Holding Find Support at a Crucial Level?

The Week Ahead

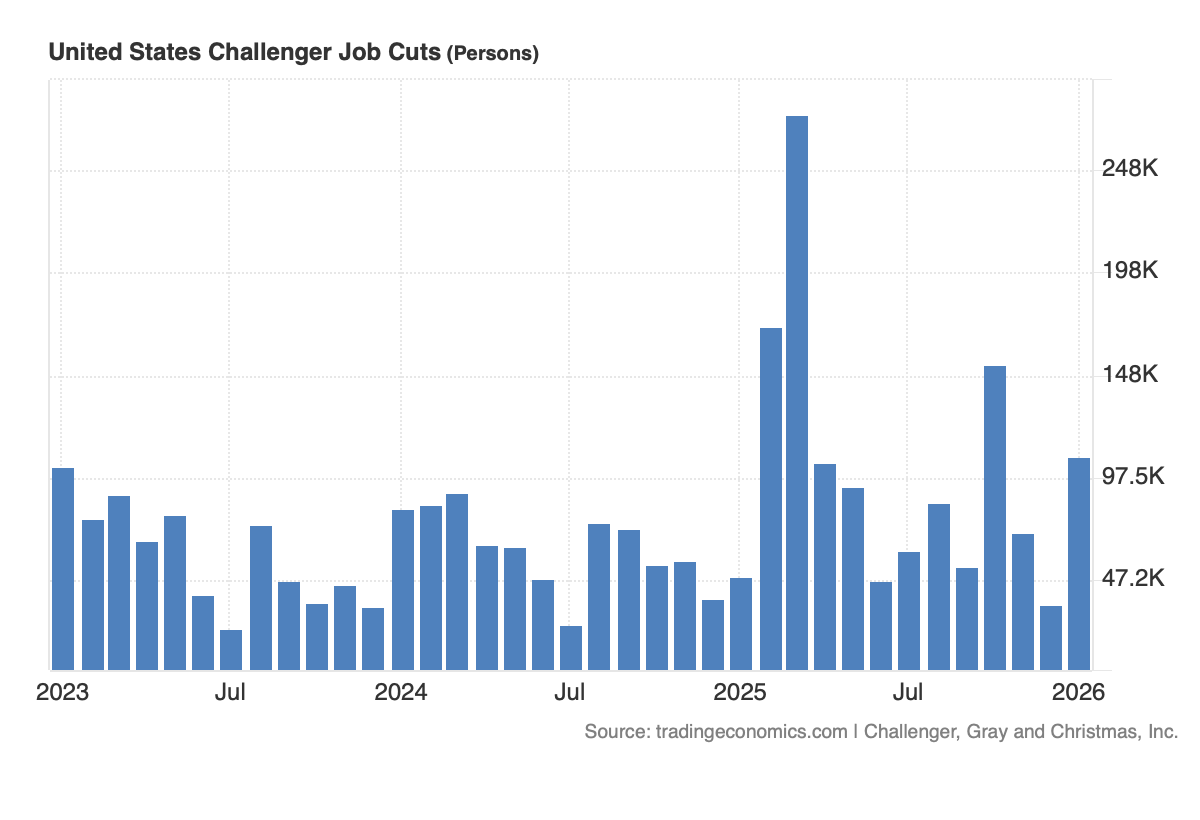

Following this week’s January PMI data, as well as the January data published by ADP, and in the Challenger Job Cuts report, the New York Fed’s Nowcast model revised its forecast for the current quarter to 2.69% from 2.73%. A pretty minor revision week to week, in our view.

On the surface, that points to an economy that continues to hum, but comments on Friday from San Francisco Fed President Mary Daly pointed out that sentiment and other surveys show folks expecting fewer jobs to be available and the unemployment rate to rise.

Coming off the January ADP Employment Report that delivered a big miss and the pop we saw in the January Challenger data, it’s hard not to agree with Daly’s logic. Connecting the dots, we see reasons to remain shareholders of Costco (COST) , TJX (TJX) , and, as we discussed on Friday, Amazon (AMZN) .

Next week brings the delayed January Employment Report, and that will round out the January jobs picture. After November and December creating an average of 53,000 jobs in each month, the consensus forecast for January calls for a pick-up in job growth to 70,000 jobs. Because we will face the winding down of holiday seasonal hiring and companies keeping a lid on hiring, we’re not as bullish on that jobs figure. While government payrolls can be a wild card in the monthly Employment Report, job creation on that front has been meager over the last few months.

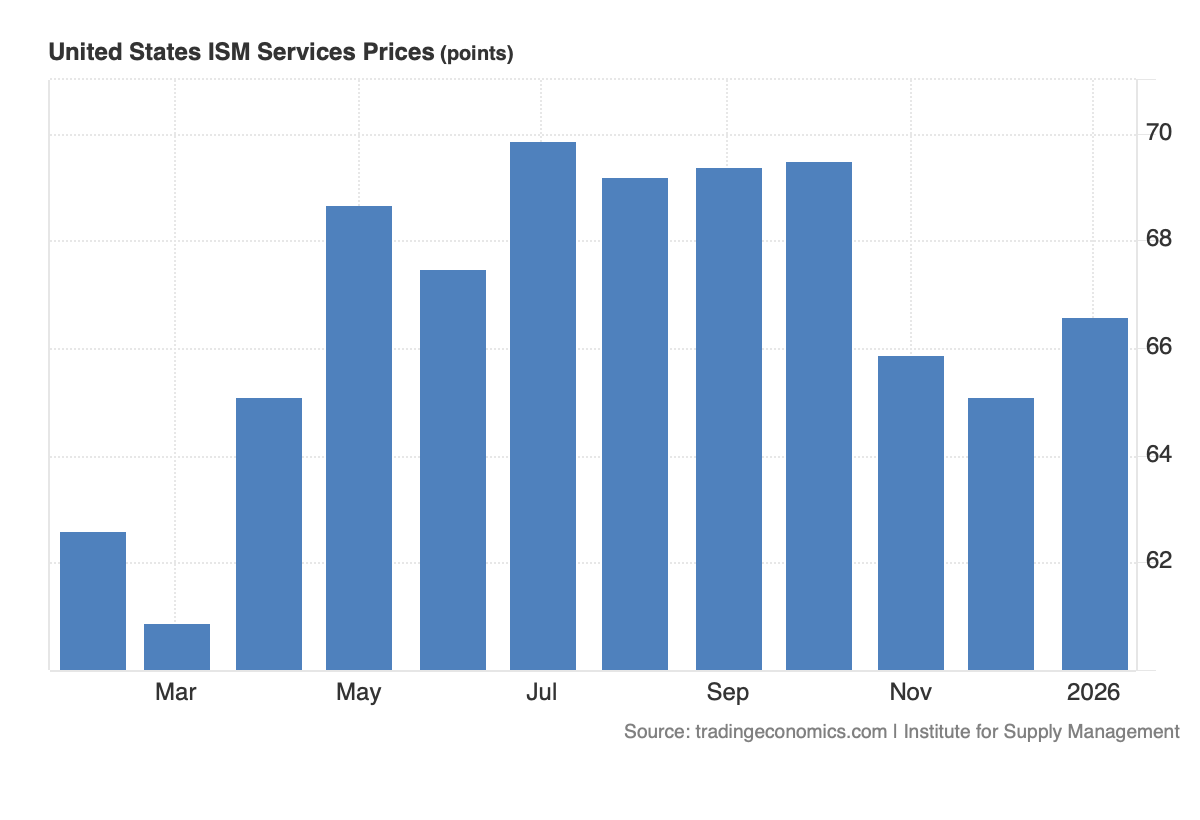

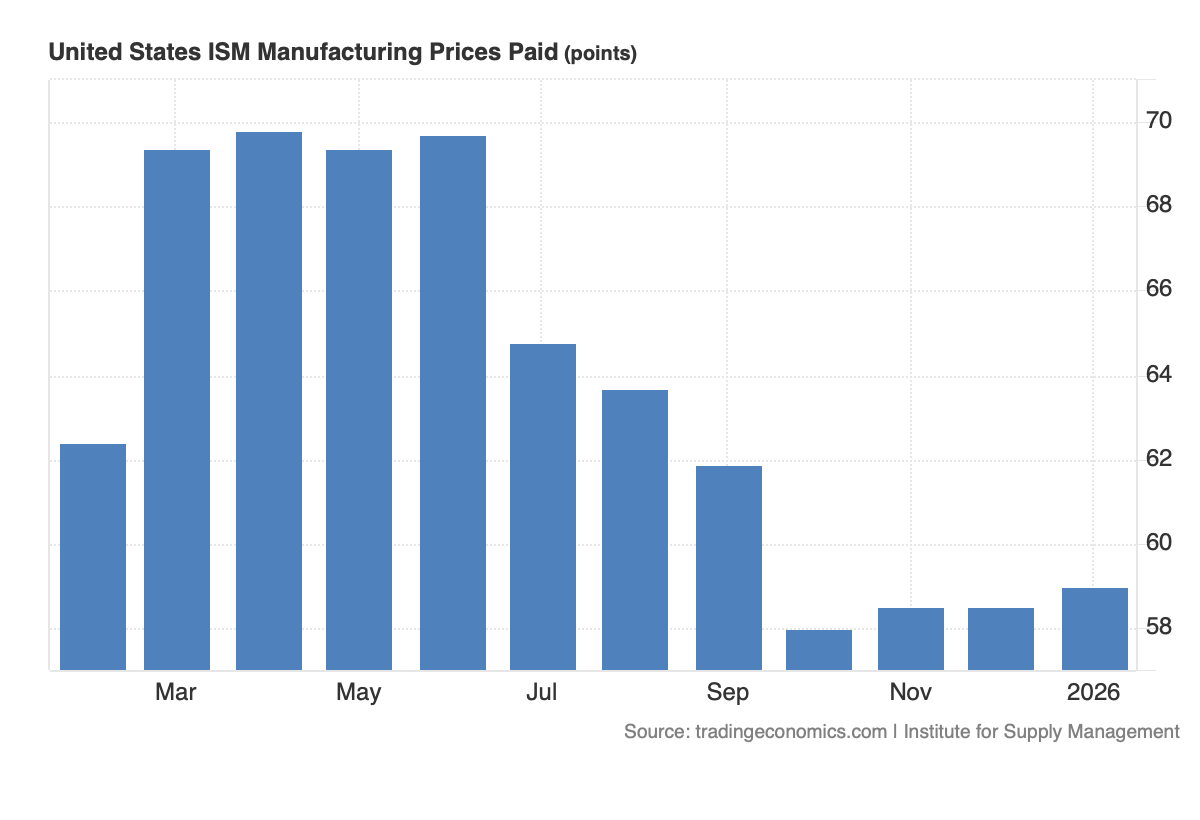

As we dig into the particulars of that report, we’ll also want to see what the January CPI and PPI reports bring, particularly for the closely watched core figures. Forecasts from the Cleveland Fed’s Inflation Nowcast call for a step down in core CPI to 2.45% in January from the 2.6% figure for November and December. That would be a welcome sight, but the same model also sees the core PCE figure coming in at 2.76% in January. We’d also add that the uptick in the Prices components seen in the January PMI Manufacturing and Services PMI data from ISM suggests the forecasted January core CPI decline forecasted by the Cleveland Fed could be a bit overly optimistic.

For now, this likely means the Fed will stand pat, but then again, that’s what the market already expects. Still, we’ll track the figures to see if something develops that could spur the Fed into action sooner than later or push out the timing for its next rate cut.

Outside of the Fed-inflation-job creation angle, we finally get the December Retail Sales report next week. While it’s a tad in the rear view, especially given the holiday shopping findings from Visa (V) , Mastercard (MA) , and comments from our own American Express (AXP) , we’ll use the data as yardsticks by which we can measure sales and comp sales figures for Costco, TJX, and Amazon.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, February 10

NFIB Small Business Optimism Index – January (6:00 AM ET)

ADP Employment Change Report – Weekly (8:15 AM ET)

Employment Cost Index – Q4 2025 (8:30 AM ET)

Import/Export Prices – December (8:30 AM ET)

Retail Sales – December (8:30 AM ET)

Business Inventories – November (10:00 AM ET)

Factory Orders – November (10:00 AM ET)

Wednesday, February 11

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Employment Report – January (8:30 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, February 12

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Producer Price Index – January (8:30 AM ET)

Existing Home Sales – January (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, February 13

Consumer Price Index – January (8:30 AM ET)

International

Monday, February 9

Japan: Eco Watchers Survey - January

Wednesday, February 11

China: Inflation Rate – January

Thursday, February 12

Japan: Producer Price Index – January

UK: GDP (Prelim) – Q4 2025

UK: Industrial and Manufacturing Production - December

Friday, February 13

Germany: Wholesale Prices – January

Eurozone: GDP (2nd Estimate) – Q4 2025

The coming week sees another avalanche of companies reporting earnings, after which ~75% of the S&P 500 will have done so. In addition to reports from Welltower (WELL) , Dutch Bros (BROS) , and Arista Networks (ANET) , we’ll be on the lookout for January revenue reports from Taiwan Semiconductor (TSM) and Foxconn, and what they have to say about demand for AI and data centers, as well as consumer electronics entering this year.

We’ll also be paying close attention to results and comments from Motorola Solutions (MSI) , given our position in Axon (AXON) . The same for Duke Energy (DUK) , American Electric (AEP) , Cisco (CSCO) , Equinix (EQIX) , Check Point Software (CHKP) , Radware (RDWR), GlobalFoundries (GFS) , and Quest Diagnostics (DGX) regarding our positions in Eaton (ETN) , Marvell (MRVL) , Broadcom (AVGO) , Labcorp (LH) , and the First Trust Nasdaq Cybersecurity ETF (CIBR) .

Here's a closer look at the earnings reports coming at us next week:

Monday, February 9

Open: Barrick Gold (B), Edgewell Personal Care (EPC), Monday.com (MNDY)

Close: onsemi (ON)

Tuesday, February 10

Open: BP (BP), Coca-Cola (KO), Datadog (DDOG), Duke Energy (DUK), DuPont (DD), Ferrari (RACE), Hasbro (HAS), Marriott (MAR), Masco (MAS), Quest Diagnostics (DGX)

Close: Cloudflare (NET), Ford Motor (F), James Hardie (JHX), Lyft (LYFT), Robinhood (HOOD), Welltower (WELL)

Wednesday, February 11

Open: CVS Health (CVS), GlobalFoundries (GFS), Hilton (HLT), Humana (HUM), Kraft Heinz (KHC), McDonald’s (MCD), Radware (RDWR), Shopify (SHOP), Terex (TEX)

Close: AppLovin (APP), Cisco (CSCO), Equinix (EQIX), Fastly (FSLY), International Flavors (IFF), Motorola Solutions (MSI), Pilgrim’s Pride (PPC), Waste Connections (WCN)

Thursday, February 12

Open: American Electric (AEP), Anheuser-Busch InBev (BUD), Check Point Software (CHKP), Lincoln Electric (LECO), Restaurant Brands (QSR), Utz Brands (UTZ)

Close: Airbnb (ABNB), Applied Materials (AMAT), Arista Networks (ANET), Coinbase (COIN), Dutch Bros (BROS), Expedia (EXPE), Ingersoll-Rand (IR), Instacart (CART), Pinterest (PINS), Rivian (RIVN), Toast (TOST), Twilio (TWLO), Wynn Resorts (WYNN), Yelp (YELP)

Friday, February 13

Open: Advanced Auto (AAP), Magna (MGA), Sensient (SXT), Wendy’s (WEN)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.