Weekly Roundup: Recapping Our Moves and Looking Ahead After a Challenging Week

Let’s review recent activity in the Pro Portfolio and discuss what we're looking for as we prepare for a shortened holiday trading week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market selloff accelerated this week with the S&P 500 moving past its 100-day moving average on Thursday as folks overlooked Nvidia’s (NVDA) beat-and-raise October-quarter results. The market rebounded on Friday, closing the week off the worst of its declines, with the S&P 500 finishing back above that closely watched technical level. However, despite Friday's rebound, all the major market barometers still finished lower on a week-over-week basis, and are down in the low single digits so far this month.

In Friday’s Portfolio video, with our own Bob Lang, we discussed why the S&P 500 re-testing that 100-day moving average would be a constructive development for the market. The thinking is that a retest would potentially clear the way for the market to rebound further in what has historically been a seasonally strong time of year. During that discussion, we explained why we may not see that re-test come about until after the Thanksgiving holiday. We also shared why that same week could prove to be a volatile one for the markets as it grapples with whether the Fed may deliver a December rate cut.

When we’ve seen the market facing similar conditions as this week, we’ve stayed focused on the medium to longer-term, emphasizing well-positioned companies with superior EPS growth prospects. That focus has served us well in the past, as did keeping our emotions in check, while we examined RSI levels for oversold opportunities. And as we detail below, we took some advantage of that over the last few trading days.

The coming shortened week is likely to see lower trading volumes, while the following one could be volatile as the market digests November economic data from ADP and ISM. Noting that landscape, we’ll tread carefully, keeping an eye on key technical levels for the S&P 500. After crediting Eaton’s (ETN) latest quarterly dividend on Friday, the Portfolio’s cash position stood at just over 7% of its assets. That gives us some room to selectively round out a few position sizes for existing holdings as the market finds its footing.

Enjoy your weekend, Saturday’s signals alert, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday, when I’ll also be sitting in for Doug Kass in the Daily Diary.

On the housekeeping front, given how the Thanksgiving holiday falls this year, our November Monthly Roundup will be published on Monday, December 1.

Catching Up on the Portfolio This Week

We began the week by initiating the EPS Diplomats model strategy as part of the Pro Portfolio. Tuesday, we flagged Home Depot (HD) as a potential Portfolio candidate by adding it to the Bullpen while removing two others. Following quarterly results from TJX Companies (TJX) that confirmed our rationale behind owning the shares, we lifted our price target to $165 from $150. On the back of TJX’s earnings press release that showed stellar October comps compared to those reported by other retailers, on Wednesday, we added further to the Portfolio’s Costco (COST) position at $882.50.

Thursday, we used the oversold condition in shares of Axon (AXON) , Meta (META) , and ServiceNow (NOW) to round out the Portfolio’s exposure to those three holdings. Also on Thursday, following Nvidia’s (NVDA) October-quarter results, we boosted our price target to $250 from $230 to reflect improved earnings prospects as chip demand climbs and manufacturing costs move further down the cost curve.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday – BofA upsized its Welltower (WELL) target to $260 from $246. RBC initiated coverage on the shares of Axon with an Outperform rating and an $860 target, sharing that the company has a "strong position in a large and growing addressable market." And Progressive (PGR) , a holding in the EPS Diplomat model, was upgraded to a Buy at HSBC with a $259 target.

Tuesday – Goldman Sachs lifted its price target on Marvell (MRVL) to $80 from $72, sharing that it expects a steep ramp in data-center guidance. Stifel lifted its Nvidia price target to $250 from $212, while Loop Capital upgraded Alphabet (GOOGL) shares to Buy from Hold with a $320 target.

Thursday – Following quarterly results from TJX and Nvidia on Wednesday night, the shares of both received multiple price target increases in addition to our own, discussed above. Price targets for TJX shares were reset to $155-$181, with a cluster around $168 that included Citi, Barclays, and BofA. With NVDA, price targets were lifted to $235-$275, with a cluster joining us at $250 that includes Benchmark, JPMorgan, Jefferies, and Susquehanna. We will note the upside outlier that is the $352 target at Evercore ISI.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Tuesday, November 18: Here's Our Game Plan as the S&P 500 Touches a 5% Pullback

Wednesday, November 19: Stocks & Market Podcast: Consumer Spending Stocks With Eric Clark

Friday, November 21: What to Watch Next in the Market With Bob Lang

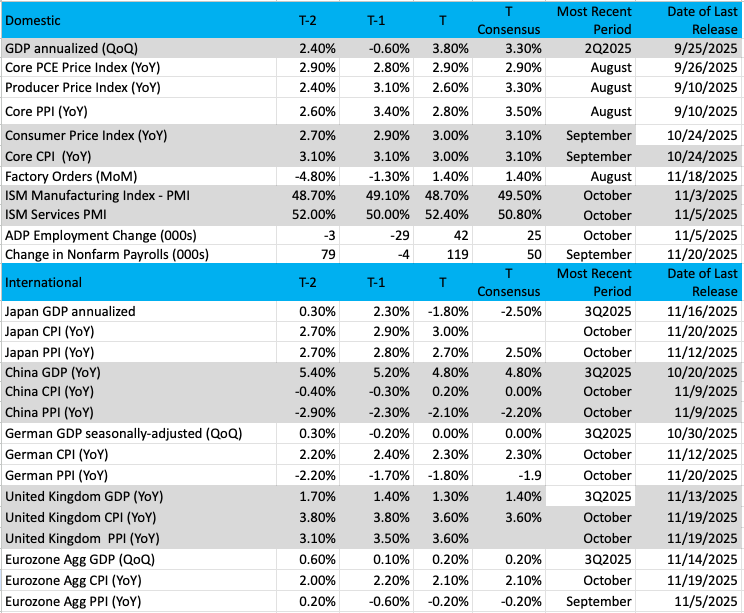

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

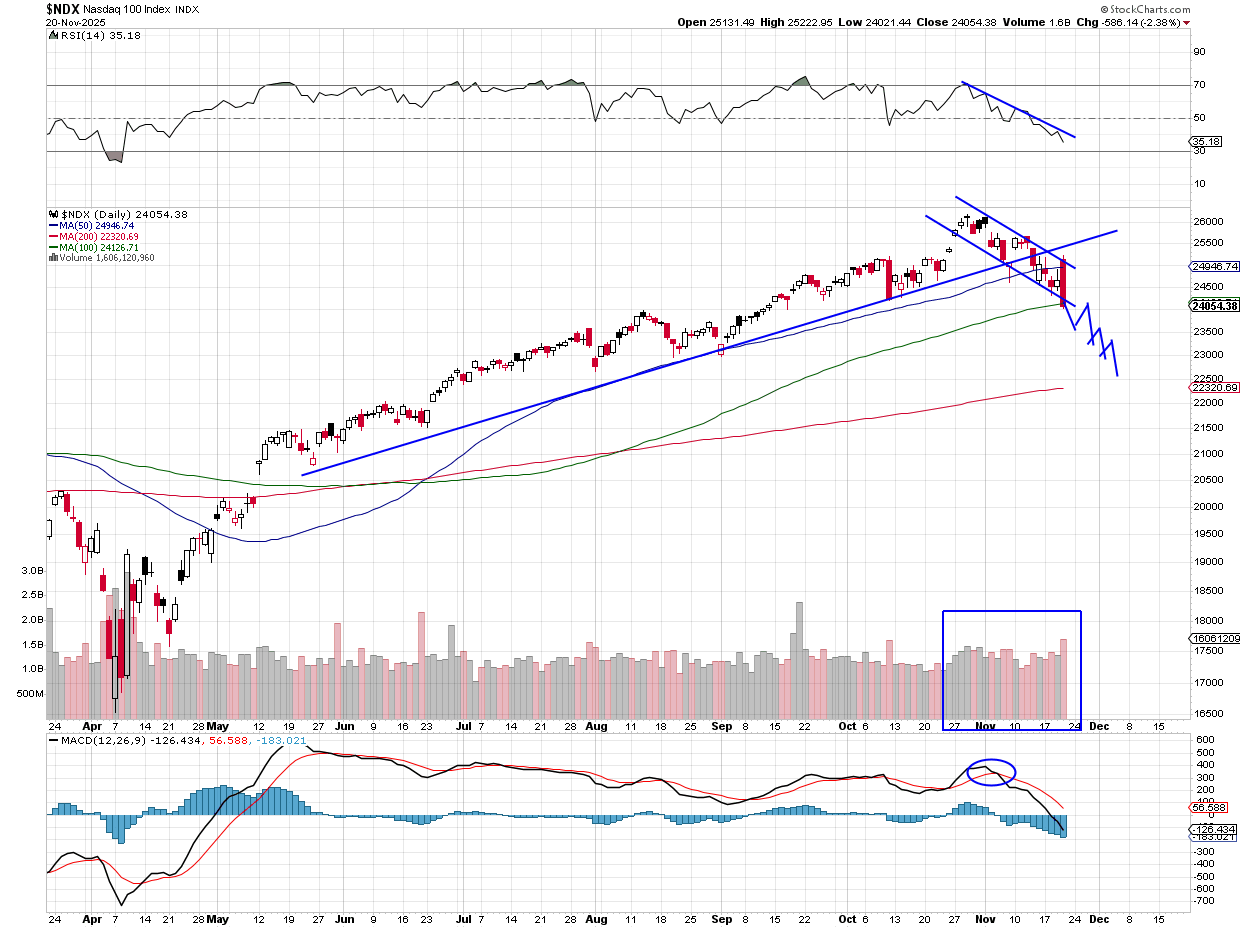

Chart of the Week: The Nasdaq 100

The Nasdaq 100 index (NDX) has been correcting sharply since the start of the month. After reaching new all-time highs just before Halloween, it seems the time was right to "pull the rug out" from underneath the staunch bulls, to the tune of an 8% correction. Now, we could certainly see the markets hold in here and make a stand, (enough is enough), as the 100-day moving average is tested. However, the trend has shifted downward now, with lower highs and lower lows.

The difficult part for investors and traders is trying to figure out why the market is going down when we are in a seasonally bullish period. The market is supposed to be rising during this time frame, or so they say. Nothing ever happens 100% of the time, though, so that is why we need to pay attention to the signposts and signals that tell us when the trade winds are shifting. Now is one of those times.

Falling below the 50-day moving average last week was significant, and on Thursday, the Nasdaq 100 tried to trade above it but failed. That failure is magnified by the fact that buyers early in the day are now sitting on a loss, and with some highly volatile sessions to come over the next several weeks, we could see quite a bit of selling. The downtrend line has been established (channel) as the uptrend line was broken last week.

Volume trends are high and bearish as well. Notice the days when the market has been down and the Nasdaq volume explodes. MACD is on a sell signal as well, and RSI is pointing lower, but not quite oversold. It will be difficult to see the markets rising with so much resistance above.

Other charts we shared with you this week were:

Monday, November 17: S&P 500 - This Indicator Is Starting to Roll Over

Monday, November 17: TJX (TJX) - Can TJX Show Strong Growth in a Tough Environment?

Tuesday, November 18: Celestica (CLS) - New EPS Diplomats Name Gets a Read

Wednesday, November 19: Barrick Mining Corp. (B) - This EPS Diplomat Holding Has a 'Golden' Look

Thursday, November 20: Home Depot (HD) - This New Bullpen Entrant Is in Need of Repair

The Week Ahead

We have a compressed week coming at us because of the Thanksgiving holiday, which will see U.S. equity markets closed on Thursday, November 27. The following day, also known to some as Black Friday, U.S. equity markets will close at 1 PM ET.

What this means is starting around Wednesday morning, trading volumes will taper off as folks hit the road for what is one of, if not the most traveled holiday. All told, roughly 82 million people are expected to travel over the Thanksgiving holiday, which is now defined as Tuesday, November 25-Monday, December 1. Cyber Monday will take place on December 1 this year.

We should expect trading volumes to remain thin on Black Friday as folks aim to capitalize on deals and sales. We’ll be watching the progress on those shopping days, but we will also be keeping a watchful eye out for any companies that try to sneak in a negative pre-announcement when most investors are looking elsewhere.

Below, we list the expected economic data, but odds are that with the federal government only starting to reopen on November 13, we won’t begin to see the return of regularly published data until after the Thanksgiving holiday. We already know the October and November Employment Report data won’t be published until after the Fed’s next policy decision. The same goes for the October and November Consumer Price Index data.

What this means is we’ll have to continue to parse the data we do get as we head toward the Fed’s next policy decision on December 10. As we enter December and that data is released, we are likely to once again see the market move based on the latest received data point. However, as history has shown, the Fed will not make a decision on any one data point, which means we will look at the aggregate data to determine if the Fed is poised to deliver a December rate cut.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, November 24

· Chicago Fed National Activity Index – October (9:30 AM ET)

Tuesday, November 25

· ADP Employment Change – Weekly (9:15 AM ET)

· FHFA Housing Price Index – September (9:00 AM ET)

· S&P Case Shiller Home Price Index – September (9:00 AM ET)

· Consumer Confidence – November (10:00 AM ET)

· Pending Home Sales – October (10:00 AM ET)

Wednesday, November 26

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Retail & Wholesale Inventories (Advanced) – October (8:30 AM ET)

· Durable Orders – October (8:30 AM ET)

· GDP (2nd estimate) – Q3 2025 (8:30 AM ET)

· Personal Income & Spending, PCE Price Index – October (10 AM ET)

· New Home Sales – October (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, November 27

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

International

Monday, November 24

· Germany: Ifo Business Climate - November

Tuesday, November 25

· Eurozone: New Car Registrations – October

· Germany: Final GDP – Q3 2025

Wednesday, November 26

· Japan: Leading Economic Index (Final) - September

Thursday, November 27

· China: Industrial Profits – October

· Germany: GfK Consumer Confidence – December

· Eurozone: Economic Sentiment & Consumer Confidence – November

Friday, November 28

· Japan: Industrial Production, Housing Starts – October

· Germany: Retail Sales – October

· Germany: Inflation Rate (Prelim.) – November

Saturday, November 29

· China: NBS Manufacturing & Non-Manufacturing PMI - November

During the short trading week, we will get a few earnings reports on Monday afternoon, but the far greater cluster will come on Tuesday. Across the wave of retailers reporting that morning, we’ll review their comp sales figures, comments about the holiday shopping season, and gauge the degree to which sweeteners, sales, and discounts could impact their margins in the second half of their current quarter.

Coming off Nvidia’s earnings this week, and as we get ready for Marvell’s on December 2, we’ll be breaking down what Dell (DELL) and HP (HPQ) have to say about their AI and data-center server businesses. That includes backlog and remaining performance obligation (RPO) figures that support Jensen Huang’s implications for 2026 and beyond. We’ll also be listening for what Dell and HPQ say about the ramp in AI PCs, given our position in Qualcomm (QCOM) . As that transpires on Tuesday afternoon, we’ll also review Zscaler’s (ZS) outlook for the coming year and what that means for our position in the First Trust Nasdaq Cybersecurity ETF (CIBR) .

Here's a closer look at the earnings reports coming at us next week:

Monday, November 24

· Close: Agilent (A), Zoom Communications (ZM)

Tuesday, November 25

· Open: Abercrombie & Fitch (ANF), Alibaba (BABA), Best Buy (BBY), Burlington Stores (BURL), Dick’s Sporting Goods (DKS), JM Smucker (SJM), Kohl’s (KSS)

· Close: Dell (DELL), HP (HPQ), NetApp (NTAP), Urban Outfitters (URBN), Workday (WDAY), Zscaler (ZS)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

· Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.