Weekly Roundup: Reaping the Benefits of Recent Portfolio Moves

This week we added to two positions, reiterated multiple price targets, and updated our shopping list of stocks.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market recovered some of the lost ground it experienced in the first several trading days of October, but despite those efforts, the S&P 500 and the Nasdaq Composite remain modestly in the red quarter to date. The back and forth we saw on the trade front between the U.S. and China continues to resemble typical game theory pre-negotiation negotiations ahead of President Trump and President Xi meeting in South Korea later this month.

We flagged that early this week, and what we saw over the ensuing days reinforces that view, including Trump himself saying on Friday that the high, threatened tariffs on China are not sustainable. We could see more gamesmanship as the Trump-Xi gathering approaches, and that could keep the market a bit volatile, but we recognize it will be the outcome of their time together that will matter more.

Over the next few weeks, the pace of quarterly earnings will heat up, and we will also have the outcome of the Fed’s next policy meeting. Based on the limited data available, it’s likely the Fed will deliver that 25-basis point rate cut it penciled in its latest Set of Economic Projections, but next week’s Flash October PMI report could cement those odds.

In reviewing consensus EPS expectations for the S&P 500 on Friday, we noticed those expectations for H2 2025 edged up to improve by 5.67% compared to H1 2025. That likely reflects the positive week of earnings we had this week, the same ones that benefited several of the Pro Portfolio’s holdings. While that is still down dramatically compared to the 13.9% figure at the end of March, it marks the second consecutive week of improvement after bottoming at 5.26% on October 3. We’ve shared why, given the S&P 500’s P/E multiple near 25x expected 2025 EPS, we would need to see those consensus EPS expectations move higher in order to drive the market higher on a sustainable basis.

The wave of corporate earnings over the next two weeks will signal we’re in the midst of a positive resetting for those expectations. Next week will bring some indication, but the last week of October, which will see Apple (AAPL) , Amazon (AMZN) , Meta (META) , Alphabet (GOOGL) , and Microsoft (MSFT) report, will be a much more important one. Results from those companies should also help calm concerns stemming from recent headlines about a potential AI bubble. We suspect we will learn how companies are using AI to drive productivity when they report next week, and those learnings should reaffirm us being only in the early to middle innings of AI adoption.

While we collect those learnings, we will continue to follow developments on the regional banking front and be mindful of technical setups, not only for the market but for our holdings as well. As we discuss below, we’ll continue to follow happenings in Washington and what that could mean for an end to the current government shutdown.

Enjoy your weekend, Saturday’s Signals alert, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

As we discussed above, the market moved higher this week, and the factors behind that action lifted the Pro Portfolio, as did the cumulative moves we’ve made over the last few weeks. That led the Portfolio to climb at a quicker pace than the market for the week, closing the gap between its year-to-date performance and that of the S&P 500.

Following our move to add to our Dutch Bros (BROS) position last week, the shares were the strongest performer this week, up a nice low-double-digit percentage. Shares of Welltower (WELL) , Qualcomm (QCOM) , Alphabet (GOOGL) , American Express (AXP) , Bank of America (BAC) , Morgan Stanley (MS) , and Universal Display (OLED) were other strong performers. Those gains, however, were mitigated by declines in Arista Networks (ANET) , Axon (AXON) , and Suro Capital (SSSS) .

During the week, we used those declines to pick up additional shares of Arista Networks and later added additional shares of Axon. We also reiterated our price targets for Morgan Stanley, Bank of America, and American Express following their consensus-topping September-quarter results.

Monday, we increased our Apple price target to $270 following a few pieces of confirming data. Reaffirming that decision, as well as our bullish stances on Qualcomm and Universal Display, research firm IDC released its Q3 2025 smartphone shipment figures that saw Apple regain market share during the 90-day period. Shortly thereafter, quarterly results from Taiwan Semiconductor (TSM) revealed its smartphone business rose more than 22% quarter over quarter. That same report from TSM revealed its High-Performance Computing segment revenue for the quarter soared more than 57% year over year, reaffirming our thoughts on Nvidia (NVDA) , Marvell (MRVL) , Eaton Corp. (ETN) , and others.

The above trades consumed more of our cash and combined with others we made in recent weeks, the Portfolio’s cash level is around 6.6% of its assets. While this is the lowest it has been in some time, we’ve carefully chosen our spots, tending to use pullbacks to put capital to work in well-positioned companies.

Because we have a few more existing positions on our shopping list, like SuRo Capital, Welltower, Arista Networks, and TJX Companies (TJX) , past a certain point, we may need to make some tough decisions. Remember, we strive to focus the Portfolio on companies benefiting from multi-year structural changes poised to deliver more robust EPS growth than the S&P 500. Let’s also remember that one of the easiest traps is to fall in love with your positions and treat them with "hopium." We will continue to follow the data, and where and when it makes sense, lock in profits so we can continue to position the Portfolio for what’s ahead.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday

Cantor Fitzgerald upped its Alphabet target to $265 from $201 as it expects the company to deliver September-quarter results ahead of consensus expectations.

Citi opened an “upside 90-day catalyst watch” on shares of Meta and reiterated both its Buy rating and $915 target.

Mizuho boosted its Nvidia target to $225 from $205 following the company’s pact with OpenAI.

UBS raised its price target on Marvell to $105 from $95 and reiterated its Buy rating.

Tuesday

BGIT initiated coverage on Costco (COST) with a Buy rating and a $1,115 target. BTIG also initiated coverage on TJX Companies with a Buy rating and a $165 target.

Goldman Sachs raised its price targets for Alphabet and Meta to $288 and $870 from $234 and $830, respectively.

KeyBanc revised its Eaton target to $420 from $410.

Piper Sandler took its Palantir (PLTR) target to $201 from $182.

Truist lifted its Labcorp target to $320 from $310.

Wednesday

HSBC upped its rating on Nvidia to Buy from Hold with a fresh $320 price target.

JPMorgan became incrementally bullish on Eaton shares, lifting its target to $429 from $380.

Roth Capital increased its Marvell target to $105 from $80

Thursday

BofA raised its Morgan Stanley target to $180 from $170, while Evercore took its MS target to $175 from $165. Wells Fargo took its MS target to $177 from $165.

Morgan Stanley increased its BAC target to $67 from $66, while Evercore inched its target up to $57 from $55.

Roth Capital lifted its Alphabet target to $265 from $210.

Friday

BofA lifted its price target on Welltower shares to $246 from $240.

Guggenheim upped its Alphabet target to $280 from $210.

Keefe, Bruyette reset its Morgan Stanley and Bank of America targets to $184 and $58 from $176 and $57, respectively.

Mizuho increased its Labcorp target to $320 from $285, and the firm also took its target for Eaton to $425 from $385.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Tuesday, October 14: Government Shutdown Could Weigh on IPOs

Wednesday, October 15: Stocks & Markets Podcast: The Next Market Catalysts With Noah Weidner

Thursday, October 16: Our Reaction to Bullish Wall Street Comments on Nvidia and Another Holding

Friday, October 17: Buying the Dip Can Burn You in the AI Market

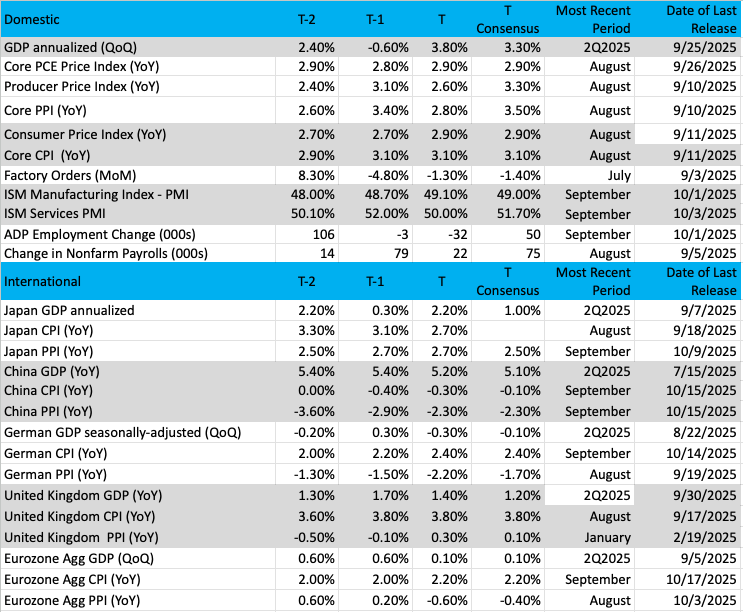

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

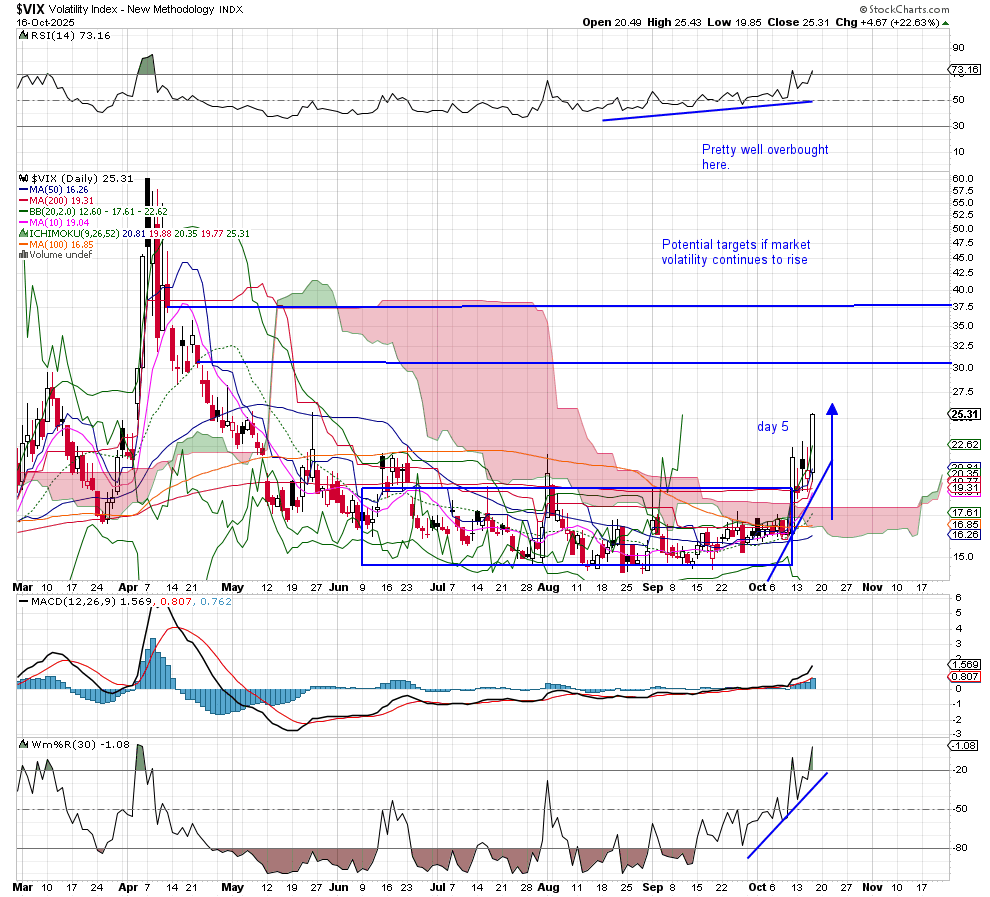

Chart of the Week: The Volatility Index

Market volatility is starting to kick up after an extended four-month lull. Investors/traders can use any excuse to sell; there are a million reasons to do it. The best excuse is simply to take profits — markets are up double digits in 2025 and sharply higher since the lows in early April. But the latest round of excuses includes worries about banking/credit (this week’s earnings reports), unresolved conflicts around the world, and a potential threat to involve the U.S. in a military action (Thursday comments by President Trump). Further, the extension of the trade war and tariff threats between the U.S. and China makes investors nervous.

The rise in volatility is being watched closely not only by investors/traders, but also by those in Washington, especially those in the White House. Policy moves and rhetorical comments are met with immediate moves in the markets, and the VIX responds in kind.

Think about how calm the market waters were this summer when the VIX was traveling in a tight range from 14.8 to 19. Stocks made their move as most investors were encouraged to jump into the pool rather than just dip a toe in. That may no longer be the case, as we see the recent action in volatility has put the VIX in a bullish state.

The big move was last Friday, October 10, as the indexes were smashed down hard on very heavy turnover. When we see big moves like this that have long candles, then we watch for a follow-through day, which often comes within 4-7 sessions after the first move (a rule created by William O’Neil, founder of Investor's Business Daily). Thursday’s sharp move up was day 5, so the original move was confirmed.

Now, this being the VIX, it does not attract long-term investors. Remember, the VIX tells us what volatile conditions will be for the next 30 days. No question the nerves of investors are being rattled, while new highs in silver/gold, bond buying (safe-haven vehicle), and heavy put option buying tell us investors are uncomfortable now. But just selling because you have a nice profit this year and do not want to lose it is a good enough reason. Just be ready to get back in — the long-term uptrend is still intact even if the market remains volatile.

Other charts we shared with you this week were:

Monday, October 13: S&P 500 - Bearish Action May Lead to More Downside

Monday, October 13: Morgan Stanley (MS) - Morgan Stanley Decline Signals Harsh Reality for Big Banks

Tuesday, October 14: Qualcomm (QCOM) - For Qualcomm, Follow the Money Flow

Wednesday, October 15: Labcorp (LH) - This Holding Remains a 'Steady Eddie'

Thursday, October 16: American Express (AXP) - American Express Offers a Nice Entry Point Before Earnings

The Week Ahead

On Friday, the government shutdown entered day 17, and after senators failed to resolve the impasse for a 10th time on Thursday, there appears to be no end in sight. We’ll see what, if any progress is made over the weekend, but with the Senate out until Monday, and the House out of session since September 19, with no plans to return until the shutdown is over, we’re not expecting much. In the prior edition of the Weekly Roundup, we noted market prediction site Kalshi pegged the shutdown lasting ~30 days. As we move into the weekend, the latest figures from Kalshi have the shutdown lasting more like 40 days.

We will continue to closely review the economic data points we do get, and next week, that means digging deep into the Chicago Fed National Activity Index for September, as well as the Flash October PMI data from S&P Global. When we examine these data sets, besides looking at them for their respective month, we’ll be tying them back to the last few iterations. What we’ll be looking for are any noteworthy changes in the data’s direction (vector) and speed (velocity).

Assuming the government shutdown continues, that Flash October PMI report will be one of the few we get before the Fed concludes its next policy meeting on October 28. As of October 17, the CME FedWatch Tool shows the market expecting just one 25-basis point rate cut exiting that meeting, with another flagged for the December policy meeting.

When it comes to 2026, that FedWatch Tool tells us the market sees three more 25-basis point rate cuts coming, which would put the Fed funds rate between 275-300 basis points. TBD if the data will support such a move, but let’s remember Jerome Powell’s term as Fed Chair ends in May 2026.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, October 20

· Leading Indicators – September (10:00 AM ET)

Tuesday, October 21

· Redbook Index – Weekly (8:55 AM ET)

Wednesday, October 22

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, October 23

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Chicago Fed National Activity Index – September (8:30 AM ET)

· Existing Home Sales – September (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, October 24

· Consumer Price Index – September (8:30 AM ET)

· S&P Global Flash PMI – October (9:45 AM ET)

· New Home Sales – September (10:00 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – October (10:00 AM ET)

International

Monday, October 20

· China: GDP – Q3 2025

· China: Retail Sales, Industrial Production – September

· Germany: Producer Price Index – September

Wednesday, October 22

· Japan: Imports/Exports – September

· UK: Inflation Rate - September

Thursday, October 23

· Eurozone: Consumer Confidence (Flash) - October

Friday, October 24

· UK: GfK Consumer Confidence – October

· Japan: Inflation Rate – September

· Japan: S&P Global Flash PMI – October

· Eurozone: HCOB Flash PMI – October

· UK: Retail Sales – September

· UK: S&P Global Flash PMI - October

Per FactSet, we will have 90 members of the S&P 500 reporting next week, and five Dow Jones Industrial Average members as well. That’s right, the pace of the September-quarter earnings season is going to become rather brisk. In all, nearly 500 companies report next week, but brace yourselves because the number reporting the following week will more than double in size. Sounds daunting, but we’ll take it one step at a time, connecting the dots as we go.

While only one Pro Portfolio holding is reporting next week, United Rentals (URI) , we will have our work cut out for us as we continue to connect the dots and relate what we learn back to our holdings. With that in mind, we will be paying close attention to quarterly results and guidance from Labcorp (LH) competitor Quest Diagnostics (DGX) , digital advertising comments from Netflix (NFLX) and Omnicom (OMC), and examining housing backlog data from Pulte Group (PHM) , M/I Homes (MHO), and others. We’ll also be following what companies like Mattel (MAT) and Hasbro (HAS) have to say about holiday shopping prospects.

As we sift through those reports and others coming our way, we’ll be noting what is said about AI adoption and usage as we get ready for Big Tech earnings the following week. We’ll also be on the lookout for earnings pre-announcements, positive as well as negative, and any implications they may have for our holdings. On Friday, we shared a current list of reporting dates for those companies, and if you missed it, you can find it here.

Here's a closer look at the earnings reports coming at us next week:

Monday, October 20

· Close: Steel Dynamics (STLD), Zions Bancorp (ZION)

Tuesday, October 21

· Open: 3M (MMM), Coca-Cola (KO), Danaher (DHR), Elevance Health (ETLV), GATX (GATX), GE Aerospace (GE), General Motors (GM), Lockheed Martin (LMT), Northrop Grumman (NOC), Paccar (PCAR), Philip Morris International (PM), Pulte Group (PHM), Quest Diagnostics (DGX)

· Close: Capital One (COF), Mattel (MAT), Netflix (NFLX), Omnicom (OMC), Texas Instruments (TXN)

Wednesday, October 22

· Open: AT&T (T), CME Group (CME), GE Verona (GEV), Hilton (HLT), M/I Homes (MHO), Travel + Leisure (TNL), Wabtec (WAB)

· Close: Alcoa (AA), Banc of California (BANC), CACI International (CACI), Crown Castle (CCI), IBM (IBM), Lam Research (LRCX), Las Vegas Sands (LVS), Lending Club (LC), Packaging Corp. (PKG), SAP SE (SAP), Tesla (TSLA), United Rentals (URI), Waste Connections (WCN)

Thursday, October 23

· Open: American Airlines (AAL), AutoNation (AN), Blackstone (BX), Darling Ingredients (DAR), Dover (DOV), Dow (DOW), Hasbro (HAS), Honeywell (HON), Lazard (LAZ), MSC Industrial (MSM), Nokia (NOK), STMicroelectronics (STM), Textron (TXT), Union Pacific (UNP)

· Close: Alaska Air (ALK), Coursera (COUR), Deckers Outdoors (DECK), Digital Realty Trust (DLR), Ford Motor (F), Intel (INTC), Norfolk Southern (NSC)

Friday, October 24

· Open: Booz Allen Hamilton (BAH), General Dynamics (GD), Illinois Tool Works (ITW), Procter & Gamble (PG)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.