Weekly Roundup: Rate-Cut Recalibration Rocks the Market

While the portfolio gave up some ground, unlike the major indexes, we closed out the week positive year to date.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are closing out another abbreviated week of trading that saw the market vacillate back and forth, before not only closing lower but moving into the red on a year-to-date basis. The catalyst for that was addtional data showing inflation pressures accelerated in December as did the labor market during the month, a combination that led the market to further recalibrate rate-cut expectations.

Following those economic data points, and after delivering 100 basis points in rate cuts, the Fed is also likely to take a wait-and-see approach with Trump White House policies to assess the potential impact on inflation. Remember, the recently reconstituted FOMC leans more hawkish than dovish. Second, if upcoming inflation data continue to move in an upward trajectory or remain sticky near recent levels, we could also start to hear the potential need for the Fed to contemplate a rate hike. As of now, we think the central bank is more inclined to leave the Fed Funds rate as is, but should we see inflation figures climb further we doubt the Fed is going to risk the progress it’s already made on that front.

Despite the market’s decline for this week, there were several positive developments, including record December-quarter revenue at Hon Hai and the year-over-year surge in December revenue at Taiwan Semiconductor (TSM). Those data points underscore the continued and elevated levels of AI and data center chip demands that keep us upbeat on Marvell MRVL and Nvidia NVDA shares. Costco COST also delivered stellar December comp sales. Meanwhile, the outlook issued by Delta Air Lines (DAL) gave us reasons to stay bullish on the shares of American Express AXP and Mastercard MA, while consumer price sensitivity comments from Albertsons (ACI) and renewed inflation expectations do the same for Amazon AMZN and Costco shares.

Because expectations for the timing pf rate cuts have been pushed out even further, the two items that are likely to drive the market in the near term are December-quarter earnings season and Trump White House policies. Earnings season begins to heat up next week, and even more so the following one, which is when Trump will give his inauguration speech and the World Economic Forum at Davos will be held.

As we get ready for those events, we will continue to focus on quality companies benefiting from multi-year tailwinds that are poised to deliver superior earnings growth. We’ll also keep our eye on the market’s technical setup. Last week as it became evident a Santa Claus rally wasn’t in the cards, we said we would keep a close watch on the S&P 500 and its 100-day moving average. Following this week’s move lower the S&P index is sitting almost on top of that figure, which clocks in at 5820. With a current reading of 39.25, the S&P 500’s relative strength index (RSI) is not oversold.

If the S&P 500 doesn’t hold support at the 100-day moving average, the next level of support is near 5573, at the 200-day moving average. Should we get to that level, it would equate to an 8.5% pullback from the market’s early December peak. Some of the froth is coming out of the market, and if that is the level where things go, it would bring with it an opportunity to pick up some well-positioned companies at better prices.

We’ve seen this a few times over the last several months, including in early August, September, and November. We were able to take advantage of those times, and we’ll aim to be ready again if that’s where the market heads this time around. Whether that happens could hinge on what we see in next week’s inflation data and the start of the December-quarter earnings season. We’ll be there to guide you and the portfolio through those events and their implications.

So, enjoy the weekend, recharge, and get ready for next week. And as you read our next iteration of portfolio signals on Saturday, and digest another batch of Sunday Soup, be sure to cast your vote in our latest member poll.

Catching Up on the Portfolio This Week

A roller-coaster week for the market ended with the S&P 500 falling almost 2% and the Nasdaq Composite losing more than that. That had an impact on TheStreet Pro Portfolio, dragging it lower, but even so, it remained in positive territory year to date, while both of those market barometers are in the red.

On Tuesday, we prudently locked in some very big gains in the portfolio’s Marvell MRVL and Nvidia NVDA positions. As we explained in that trade alert, record December-quarter revenue from Hon Hai and other bullish data points mean we want to remain long-term owners of MRVL and NVDA shares. Later that day we revisited Bullpen resident Axon Enterprises AXON, laying out where we might be interested in calling that name back up to the portfolio.

We downgraded shares of Builders FirstSource BLDR to a Four rating on Wednesday given what we saw on the inflation front in the December ISM Service PMI and the rolling over in the Mortgage Bankers Association’s Purchase Index. We shared that if Friday’s December Employment Report suggested an even further pushout in potential rate cut timing, we would be inclined to unwind the portfolio’s BLDR position.

Even though the market was closed on Thursday, we discussed our take on Costco’s COST robust December sales report and explained why quarterly results from Jefferies (JEF) set the stage for strong results from Morgan Stanley MS and Bank of America BAC next week.

On Friday, we discussed the stronger-than-expected Q4 revenue dynamics at Taiwan Semiconductor as well as why quarterly results and guidance from Delta Air Lines (DAL) were positives for several of our holdings. Later that morning, the blowout December jobs figure, the subsequent rise in the 10-year Treasury yield, and the pushout in rate-cut timing expectations to late H2 2025 led us to close out our BLDR position. That move returned the portfolio’s cash position to more than 11%, which means added firepower that we can opportunistically use once the dust settles from this latest market recalibration.

Much like you, we are following the devastating effects of the California wildfires, and our hearts go out to all affected. When the fires are eventually contained and this disaster sorted out, the rebuilding efforts should be a nice positive for our shares of United Rentals URI, Vulcan Materials VMC, and Waste Management WM.

Now let’s turn and see what Wall Street had to say this week about the portfolio’s holdings.

KeyBanc upped its target on Alphabet GOOGL to $225 from $215 and Meta Platforms' META to $700 from $655. The firm also increased its target on The Trade Desk TTD to $140 from $130, matching our target price.

Cantor Fitzgerald had a few price target adjustments for our holdings, moving its Meta target to $730 from $680, its Alphabet target to $215 from $190, and pushing the one for Amazon AMZN to $270 from $240.

Mizuho lowered its Applied Materials AMAT price target to $200 from $210 but reiterated its Outperform rating.

Argus named Amazon shares a Top Pick for 2025, in part because of the faster adoption of AI compared to the cloud at this stage of its development. We agree, but we’d also add that continued inflation pressures should keep consumers flocking to Amazon as well as Costco.

Barclays not only upgraded Dutch Bros BROS shares to Overweight from Equal Weight, but it also reset its price target at $70 from $38. We recognize we have some catching up to do with our BROS target, but we expect to do that when the company reports its December-quarter earnings and sheds more light on its expanded food menu plans.

Following our recent buy of more Labcorp LH shares, Evercore ISI upgraded its rating on the shares to Outperform and lifted its price target to $265 from $260. We continue to keep tabs on bird flu cases, which can cause severe disease in animals and can pass from animals to people. Should we see the volume of those headlines grow, Labcorp and its new H5 bird flu molecular test are likely beneficiaries.

Susquehanna lowered its target for Lockheed Martin LMT to $590 from $695, and we intend to revisit our $650 LMT target when the company reports its quarterly results later this month. That event should also bring with it the company’s updated multi-year delivery schedule, a potential catalyst we’ve been waiting for.

Marvell MRVL shares saw Stifel inch its price target to $130 from $125 this week, while research firm Craig Hallum named the shares a “Top Idea” as it increased its target to $149 from $132.

Bank of America lifted its price target for Morgan Stanley MS to $146 from $140, which is a few dollars above our target. At almost the same time, UBS upgraded Bank of America shares to Buy from Neutral, slapping a $53 price target on them in the process, while Barclays upped its BAC target to $58 from $53.

Deutsche Bank raised its ServiceNow NOW price target to $1,300 from $1,020, something we appreciate following our early January pickup of a few more NOW shares for the portfolio.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, January 6: Hon Hai Reveals Record Revenue as CES Kicks Off

Tuesday, January 7: Here's the Plan for Our Oversold Defense Holding

Wednesday, January 8: Explaining Why We've Downgraded This Construction Name

Friday, January 10: Here's Why We Sold Off This Name, Plus One Stock We’re Looking to Add to

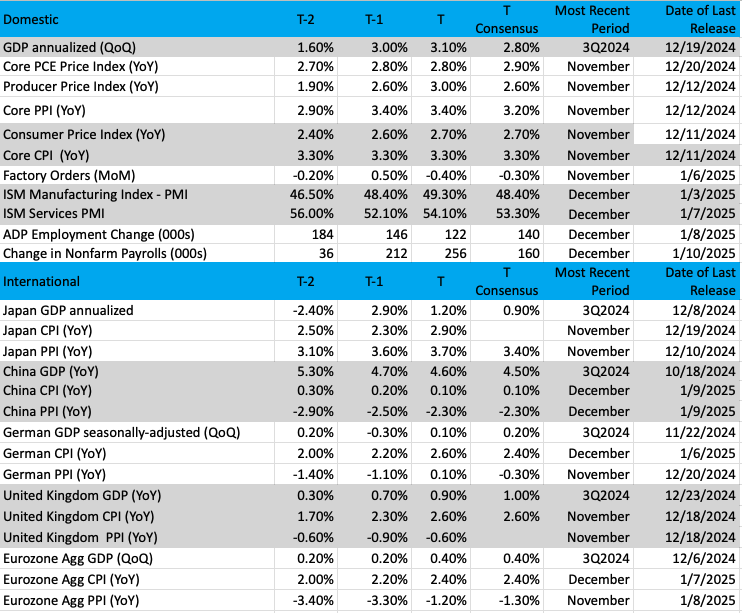

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: VanEck Semiconductor ETF (SMH)

We always keep an eye on the semiconductor group. After all, we have several names in the portfolio that influence the VanEck Semiconductor ETF SMH, and as the semis go so go technology and growth. Nvidia NVDA, of course, is the big name in this ETF that has wide influence, but there are others that contribute to performance such as Qualcomm QCOM, Broadcom AVGO, and Applied Materials AMAT, along with Taiwan Semiconductor TSM.

Recent trends have been bullish for the SMH. A breakout at the start of the year above the downtrend line (drawn in) was confirmed (two blue bars in a row). Even as the ETF dipped midweek we still see the downtrend line serving as support (for now). Further, moving averages are also supporting the price; they are below the currentprice of the SMH.

But the indicators are not flashing bullish here, in fact, they are much more neutral than anything. Money flow is flat, and stochastics (momentum) are not moving in either direction or simply are moving sideways, as is the MACD (moving average convergence/divergence), which is on a tepid buy signal.

It appears most investors in this group are just waiting for earnings season to get underway. Some traders are worried these stocks are "ahead" in terms of valuation, but we will know more when earnings start to be released in the weeks ahead. For now, we see the SMH as simply treading water, but if it moves above $265 on good volume then that would be a positive development.

Other charts we shared with you this week were:

Monday, January 6: S&P 500 - Santa Failed to Call, So Now What?

Monday, January 6: Applied Materials (AMAT) - This Tech Holding Is Building a Base

Tuesday, January 7: Netflix (NFLX) - This Bullpen Name Glides into a Support Zone

Wednesday, January 8: Qualcomm (QCOM) - As This Holding Builds a Second Base, Will It Be the One?

The Week Ahead

Next week brings a full week of trading, the first one in quite a few, and it’s going to be jam-packed with economic data, Fed speakers, and the start of the December-quarter earnings season.

Coming off this week’s inflation and December Employment Report data, the market’s economic focus will be on December CPI and PPI data as well as what the half dozen Fed speakers have to say about the future of monetary policy. Based on what we’ve seen this week, our expectation is for "higher for longer" with the market now postulating how late in 2025 any next rate cut could be.

In addition to next week’s data that we’ve laid out below, we’ll also be waiting to see what the next update for the Atlanta Fed’s rolling GDPNow model says about Q4 GDP expectations. We’re nearing the end of December data and that means the model’s forecast should be solidifying once it includes next week’s December Retail Sales, Housing Starts, and Industrial Production figures. This also means we will be turning our focus to GDP expectations for the current quarter and that means marking our calendars for January 24, which is when we’ll receive S&P Global’s Flash January PMI.

As you mark your calendar for that, be sure to also circle January 20, which is Inauguration Day, as well as January 20-24 for the World Economic Forum in Davos, Switzerland. We expect President Trump will use his inaugural address to set the tone for his next term in the White House, and Davos should bring responses and comments from world and business leaders that are likely to be insightful and helpful to us.

With that in mind, we’re starting to see Elon Musk backtracking on his $2 trillion cost-cutting target for the Department of Government Efficiency (DOGE). He’s now calling that a “best-case” outcome and conceded there is only a good shot at cutting half that. We suspect there will be more pushback on DOGE, and our thinking is that pressure should take some off shares of Lockheed Martin LMT.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, January 13

· Consumer Inflation Expectation – December (11:00 AM ET)

Tuesday, January 14

· NFIB Small Business Optimism Index – December (6:00 AM ET)

· Producer Price Index – December (8:30 AM ET)

Wednesday, January 15

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Consumer Price Index – December (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Beige Book (2 PM ET)

Thursday, January 16

· Retail Sales – December (8:30 AM ET)

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Import/Export Prices – December (8:30 AM ET)

· Business Inventories – November (10:00 AM ET)

· NAHB Housing Market Index – January (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, January 17

· Housing Starts & Building Permits – December (8:30 AM ET)

· Industrial Production & Capacity Utilization – December (9:15 AM ET)

International

Monday, January 13

· China: Import/Exports - December

Tuesday, January 14

· China: Vehicle Sales, Outstanding Loan Growth – December

Wednesday, January 15

· Japan: Machine Tool Orders – December

· UK: Inflation Rate – December

· Eurozone: Industrial Production - November

Thursday, January 16

· Germany: Inflation Rate – December

· UK: Industrial Production - November

Friday, January 17

· China: GDP – 4Q 2024

· China: Industrial Production, Retail Sales – December

· UK – Retail Sales – December

· Eurozone: Inflation Rate - December

The pace of corporate earnings reports kicks into gear next week, and once again that means we will have a sea of bank and financial company earnings to sift through. That includes the ones from Morgan Stanley MS and Bank of America BAC, which should benefit from the uptick in investment banking activity and asset management. Quarterly results reported this week from Jefferies (JEF) were the last point of confirmation for that.

Ahead of those two reports on Thursday, results from JPMorgan Chase (JPM), Goldman Sachs (GS), and Citigroup (C) the day before will bring additional color. In those reports, we’ll look for more confirmation on investment banking, the outlook on loan activity, and expectations for net interest income in the coming year. Those insights will refine expectations for results and guidance from Morgan Stanley and Bank of America. And we’ll backfill in what we hear from them when Truist (TFC), PNC (PNC), and others report.

When KB Home (KBH) posts its quarterly numbers, we’ll be interested in management’s take on recent inflation data and how it impacts their outlook for the coming year. We’ll also be on the lookout for earnings pre-announcements and potential implications for our holdings.

Here's a closer look at the earnings reports coming at us next week:

Monday, January 13

· Close: KB Home (KBH)

Tuesday, January 14

· Open: Applied Digital Corp. (APLD)

· Close: Calavo Growers (CVGW)

Wednesday, January 15

· Open: BlackRock (BLK), BNY Mellon (BNY), Citigroup (C), Goldman Sachs (GS), JPMorgan Chase (JPM), Wells Fargo (WFC)

Thursday, January 16

· Open: Bank of America (BAC), Morgan Stanley (MS), PNC (PNC), US Bancorp (USB), United Health (UNH)

· Close: JB Hunt (JBHT)

Friday, January 17

· Open: Citizens Financial (CFG), Fastenal (FAST), State Street (STT), Truist (TFC).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics : Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.