Weekly Roundup: Portfolio Treads Water While Market Questions Need for Rate Cuts

After a few moves this week, we still have room to do more, including a new position or two.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

After hitting another round of all-time highs during the week, the stock market traded off on Friday, leaving the S&P 500 with muted gains for the holiday-shortened week. Economic data painted the picture of a slower economy but also one contending with elevated inflation and the potential for more ahead. But it was Friday’s much worse than expected August Employment Report and the net downward revisions for June and July that ultimately weighed on stocks.

The initial "bad news is good news" response to the weak August jobs print of 22,000 led the market higher, stretching its extended P/E valuation that much further. Only after folks started to question the implications of the much slower than expected jobs market and wage gains that may not fully offset inflation pressures did traders and short-term investors start to question why the Fed may need to deliver the multiple rate cuts expected by the stock market the rest of this year.

There was also likely some element of “sell the news” following the increased likelihood that the Fed will deliver at least some rate cuts before the end of this year. To us, next week’s August CPI and PPI figures will help frame not only the Fed’s policy statement and Fed Chair Powell’s remarks on September 17. The same goes for the updated set of economic projections the central bank will share that afternoon. With two more policy meetings left in the year, where the Fed funds rate lands for 2025 in that update will tell us if the market’s expectation is tracking… or not.

Stepping away from potential Fed policy and back to the market, our view remains that for the market to move meaningfully higher, given its week-ending P/E ratio of more than 24x on expected 2025 EPS, we are going to need to see second-half 2025 EPS expectations move higher. This week, companies presented at a few investor conferences, but next week, we have the annual Goldman Sachs Communacopia & Technology conference. Not only will it bring out some heavyweights, but they will be presenting with only a few weeks to go in the current quarter.

We’ll be interested in what they say about demand dynamics, inflation, pricing, and, where appropriate, pending new tariffs. This week, President Trump said he would be placing chip tariffs “very shortly,” and that they will be “fairly substantial,” but those that move their manufacturing to the U.S. will be exempt. Per Trump, that exemption includes Apple AAPL. Citing national security concerns, the Trump administration is set to introduce new regulations targeting imports of Chinese drones and medium to heavy-duty vehicles.

Next week also brings us Apple’s next wave of hardware products, and we could see some price target adjustments later in the week. In recent years, this annual event has gone from shock and awe to iterative updates. Perhaps that might change this year, but we give that a low probability. Still, Apple could surprise us with something on the Apple Intelligence or Siri front.

It's going to be another busy week, like this past one, but instead of being back-end loaded, things will be spread out across the entire week. We’ll be there to guide you through it, and if opportunity strikes or if we need to shift gears, we’ll communicate our thoughts and actions to you in short order.

Enjoy your weekend, Saturday’s signals alert, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

As noted above, the post Labor Day holiday week ended on a whimper with the S&P 500 giving back most of the gains it picked up earlier in the week. Declines on Friday for shares of Dutch Bros BROS, Nvidia NVDA, and Microsoft MSFT were largely responsible for the Pro Portfolio’s being little changed week over week. Those declines were offset by the high-single-digit move in Alphabet GOOGL as well as gains from Apple AAPL, Costco COST, Universal Display OLED, United Rentals URI, and TJX Companies TJX. With 17 trading days left in the quarter, the Pro Portfolio remains firmly in the black and even more so on a year-to-date basis.

During the week, we lifted our price targets on Alphabet and Apple following what we saw as a favorable DoJ ruling for Alphabet. As we and others lifted our price targets, GOOGL shares catapulted higher, pushing our position size well past 4.5%. That led us to do some prudent and very profitable profit-taking, using the bulk of the proceeds to pick up some additional shares of Marvell MRVL and Palantir PLTR.

Even after those buys, we have room to add further to those positions and some others in the Pro Portfolio. However, as we discussed on Friday, with the prospects for rate cuts growing after the disappointing August Employment Report, we are examining some new candidates for the Pro Portfolio and dusting off one or two currently in the Bullpen.

Existing positions on our updated shopping list include TJX Companies, Waste Management WM, SuRo Capital SSSS, the Cybersecurity ETF CIBR, and Palantir PLTR. We have ample cash on hand, just over 10% of the Pro Portfolio’s assets, as well as room to expand our holdings a wee bit further past the current 25 positions.

We also lifted our price target for United Rentals to $1,000 from $950, and we have every intention of revisiting our Morgan Stanley MS and Bank of America BAC targets as the upcoming wave of IPOs is priced.

Now let’s see what others on Wall Street had to say about the Pro Portfolio’s holdings during this shortened, but electric week for the market:

BofA notes that Apple is developing a new AI-powered web search feature for Siri, internally dubbed "World Knowledge Answers," with plans to launch in spring 2026. The report suggests that the tool might be powered by a customized version of Google’s Gemini model. That lines up with our thinking as well.

MoffettNathanson upgraded AAPL shares to Neutral from Sell as a “number of key headwinds have faded” and the “worst-case scenarios are off the table.” Meanwhile, Oppenheimer boosted its AAPL target to $270 from $235 in part due to a potential AI collaboration between Apple and Google.

Tigress Financial lifted its GOOGL price target to $280 from $240. Like us, the firm sees the company well-positioned with AI, cloud, and YouTube. Wedbush hiked its price target to $245 from $225 for GOOGL shares, while BofA went to $252 from $217.

JPMorgan reiterated its Overweight rating on Nvidia NVDAand $215 price target as chip demand continues to outweigh supply, which keeps its lead times “stretched but stable.”

Erste Group reinstated coverage of TJX with a Buy rating and calls out management’s guidance as somewhat conservative.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns and Podcast. If you happened to miss one or more of them, here are some helpful links:

Tuesday, September 2: August Manufacturing PMI No Slam Dunk for a Rate Cut

Wednesday, September 3: PWC’s Holiday Shopping Survey Backs Our Consumer Plays

Thursday, September 4: Rate Cut Will 'Come Down to the Wire' as Fed Sends Mixed Messages

Thursday, September 4: Stocks & Markets Podcast: Frothy Valuations and Focusing on the Longer-Term With Ed Maguire

Friday, September 5: Our Game Plan After the Big Miss August Jobs Report

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.

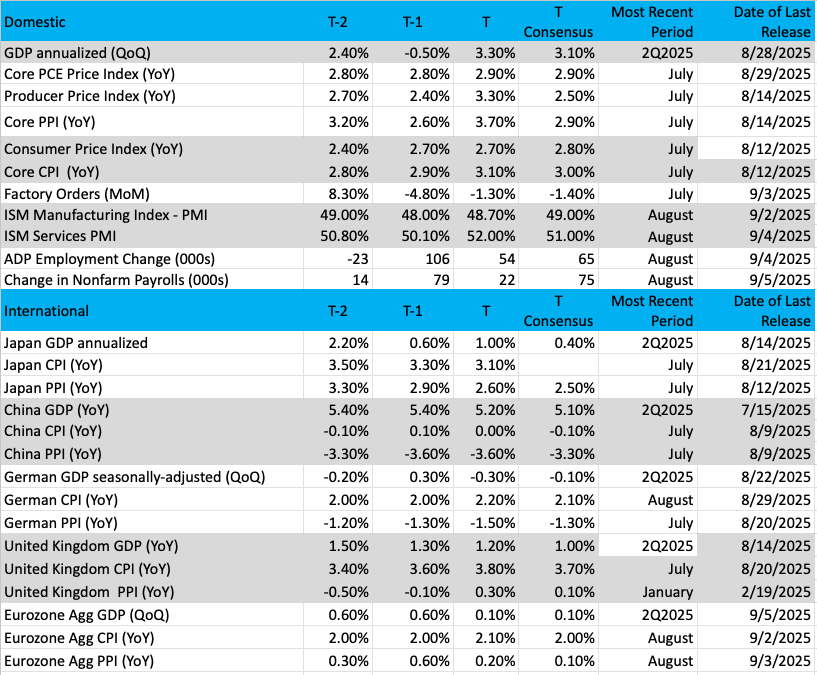

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

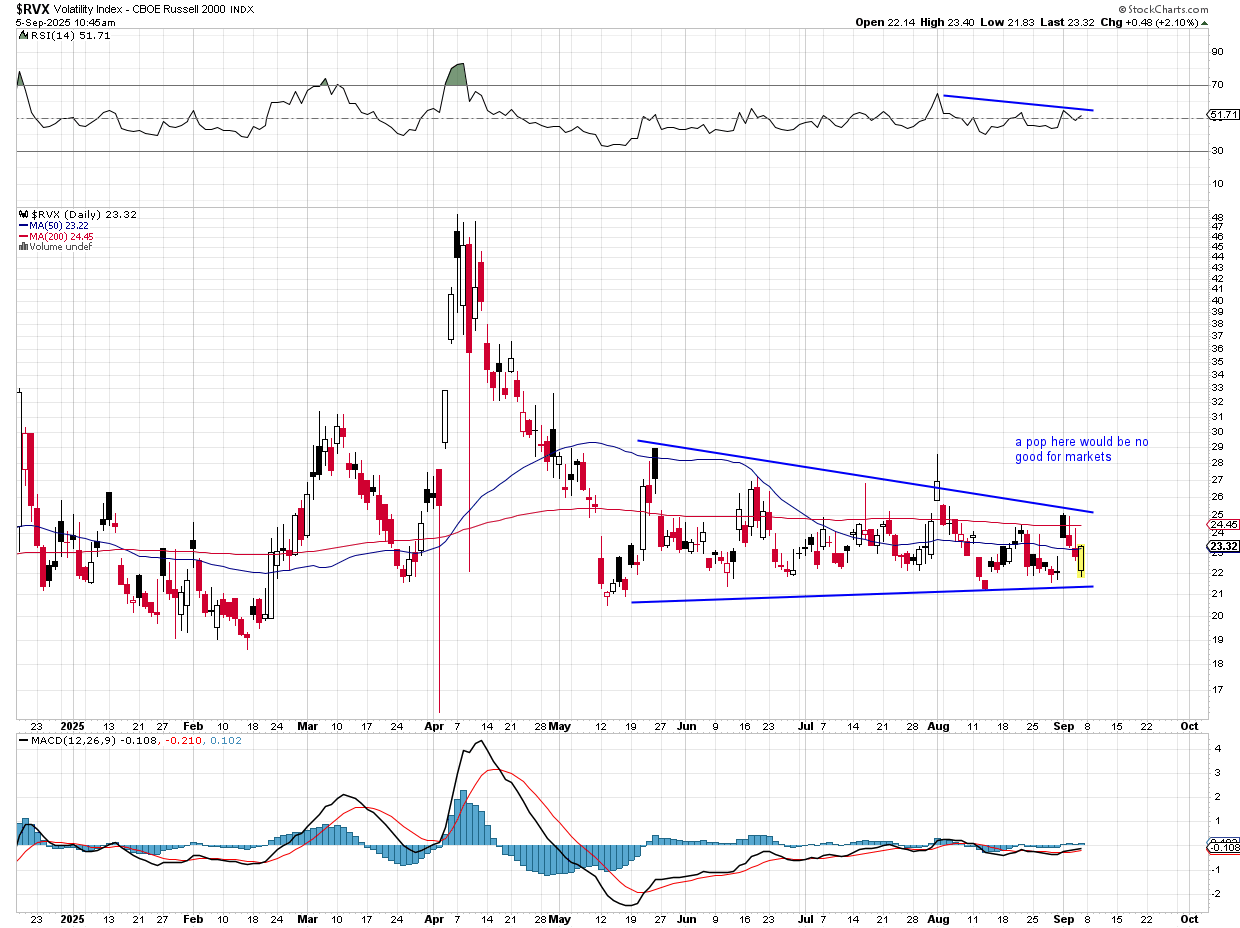

Chart of the Week: The Russell 2000 Volatility Index

We always have one eye on volatility to make sure we can get a good read on investor sentiment. While the VIX is one of the best tools to help us gauge investor sentiment, there are two others that also provide good information.

The VXN is the Nasdaq 100 volatility instrument, while the RVX represents volatility on the Russell 2000, or the small-caps. These two instruments tell us how investors are "feeling" about the market at a certain point in time.

Now, why would one need to focus specifically on small-caps or the Nasdaq 100 rather than the volatility index, which itself measures the entire S&P 500? It’s a good question. We would like to understand how certain areas of the market are perceived at certain moments in time. Small-caps and the Nasdaq tend to lead the rest of the market.

If small-cap stock volatility (RVX) is rising, it means we can expect large moves, but if the VXN is not moving much, then we can say the market players are complacent, and that sets up perhaps for a contrarian move, which might be down. Take this all with a grain of salt; there is no reason to trade/invest from this information, but it is always good to know where people stand in their views, as it may influence behavior.

Looking at the chart of the RVX, we see a very long base, a tight pattern with a small range, especially over the last few months. This may signal a springboard move as the RVX is coiled like a spring. The RSI (relative strength index) is not showing us much; volatility is well-contained. It is no surprise then that the small-caps have been rallying have been rallying. With RVX so low and remaining down there is little worry of a stock market selloff (but there always should be!).

Keep your eye on this chart, if small-cap volatility starts to rise, it could have damaging effects on the rest of the stock market.

Other charts we shared with you this week were:

Monday, September 2: S&P 500 - Market Confronts 'Blatant' Seasonality and Complacency

Tuesday, September 2: Let's Give Apple Some Love, Too!

Wednesday, September 3: ServiceNow (NOW) - After a Rough Go, This Tech Holding Is Battling Back

Thursday, September 4: Meta (META) - Meta Bulls Should Make a Stand at This 'Springboard' Spot

The Week Ahead

We have a full week on tap ahead, but what we won’t have are any Fed officials making the rounds. As we discussed in Friday’s video, over the weekend, the Fed entered the blackout period ahead of its September policy meeting. That means the market will be left to fend for itself when the August CPI and PPI reports are published. Both are expected to show core PPI and CPI flat with their July counterparts, which means at elevated levels. Backing that expectation are the inflation findings from this week’s August PMI reports.

Before we get the PPI and CPI reports on Wednesday and Thursday, at 10 AM on Tuesday, the annual revision to non-farm payroll data will be released. This will affect employment figures for the 12 months through March 2025, and given all the bluster from the White House about “better employment data” going forward, we would not be surprised if that data set is revised lower. Call us a bit cynical, but a meaningful downward revision would not only add more support for Trump’s call to lower interest rates, but would also take some wind out of the Biden economy.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, September 8

· Consumer Credit – July (3 PM ET)

Tuesday, September 9

· NFIB Small Business Optimism Index – August (6:00 AM ET)

Wednesday, September 10

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Producer Price Index - August (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, September 11

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Consumer Price Index – August (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

· Treasury Budget – August (2 PM ET)

Friday, September 12

· University of Michigan Consumer Sentiment Index (Prelim) – September (10:00 AM ET)

International

Monday, September 8

· Japan: Eco Watchers Survey - August

Wednesday, September 10

· China: Inflation Rate, Producer Price Index – August

· Japan: Machine Tool Orders - August

Thursday, September 11

· Japan: Producer Price Index – August

· Eurozone: European Central Bank Interest Rate Decision

Friday, September 12

· Japan: Industrial Production – July

· UK: GDP, Industrial Production – July

While we have no Pro Portfolio companies reporting next week, several of them will be presenting at the Goldman Sachs Communacopia + Technology Conference, including Axon AXON, Nvidia NVDA, and Microsoft MSFT. We also have Morgan Stanley MS and Bank of America BAC presenting at the Barclays Global Financial Services Conference.

Other conferences next week include the Morgan Stanley Global Healthcare Conference, the Wolfe Research TMT Conference, and the B. Riley Consumer & TMT Conference. We’ll continue to mine management comments from these and other events about the current quarter and ensuing ones. As we update our thinking, we’ll be sharing those thoughts and any implications with you.

We also have Apple’s AAPL “Awe Dropping” event on Monday, September 9, at 1 PM ET. It’s widely expected to show its next iteration of iPhones and add a new iPhone Air to the mix. Apple will also unveil other new hardware, but we’ll be interested in how those price tags stack up against existing models. We will also be l istening intently on what is said about the company’s Apple Intelligence and Siri efforts. Earlier this week, we discussed how the door is now open for Apple to tap Google GOOGL as part of that.

Back to the companies that are reporting next week, Oracle’s ORCL comments about capital spending and AI adoption will be one of our focal points. At Adobe ADBE, AI adoption will be of interest, as well, but also the degree to which it is seeing AI lift its pricing and margins.

This past week, we saw Costco COST continue to win consumer wallet share in grocery during August, and that has us interested in Kroger’s KR quarterly results. We’ll also be looking to see if Kroger is seeing a pick-up in its private-label business and what it has to say about the trend in food inflation.

Here's a closer look at the earnings reports coming at us next week:

Monday, September 8

· Close: Casey’s General Store (CASY), Mission Produce (AVO)

Tuesday, September 9

· Open: SailPoint (SAIL)

· Close: AeroVironment (AVAV), Calavo Growers (CVGW), Oracle (ORCL), Synopsys (SNPS)

Wednesday, September 10

· Open: Chewy (CHWY)

· Close: Oxford Industries (OXM)

Thursday, September 11

· Open: Kroger (KR)

· Close: Adobe (ADBE).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.