Weekly Roundup: Portfolio Notches Another Win, But Next Week Is Big

We are mindful of potential risks as earnings heat up, the Fed meets and Trump tariffs loom.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

With one week to go in January, one that some watch as an indicator of the market’s performance for the coming year, all the major market averages are up month to date. That’s even after Friday’s move lower that was precipitated by the findings in S&P Global’s Flash January PMI report.

Helping spur the market higher this week were some positive earnings reports, many of which brought support for TheStreet Pro Portfolio's holdings. There were also several AI and data center developments that, in our view, confirm companies are in an AI arms race. Over the near and medium term, that bodes rather well for several of our chip and construction-related positions.

As we explain in our road map for the coming week below, with the Fed’s next policy decision and looming Trump tariffs, next week is a big one for the markets. It’s also another big one on the earnings front, with more than one-fifth of the S&P 500 constituent weighting reporting, as the pace of corporate reporting accelerates.

We expect next week will be a busy one for the portfolio, and that means we’ll be on guard for surprises and developing risks even as we look out for opportunities. One developing risk is the potential for a showdown between President Trump and Fed Chair Powell as the former seeks lower interest rates and the latter stays on path to tame inflation. As we discuss below, the uncertainty around potential Trump tariffs and the impact on inflation is something we are watching closely.

On the earnings front, quarterly results on Friday from American Express AXP, which were in-line to only slightly better than consensus, showed that may not be enough for the market, especially if a company’s shares have been zooming higher of late. While such a share-price reaction may not be appealing, we’ll let the underlying fundamentals and prospects for the coming quarters be our guide. In some cases, these reactions could bring the chance to add to our holdings, but we’ll evaluate those situations as they develop.

Enjoy Saturday’s ripped-from-the-headlines "signals" for the portfolio’s strategies and be sure to return for Sunday Soup, our collection of articles and streaming ideas that caught our attention this week.

Catching Up on the Portfolio This Week

As the S&P 500 expanded its January gains during this shortened trading week, so too did the TheStreet Pro Portfolio. Leading the way from our holdings are the double-digit January-to-date gains in Applied Materials AMAT, Dutch Bros BROS, Eaton ETN, Meta META, Marvell MRVL, and Qualcomm QCOM. Supporting some of those moves were the number of AI and data center developments this week, including President Trump’s Stargate announcement, guidance from SK Hynix, and Meta’s Mark Zuckerberg telegraphing a 50%-70% year-over-year capital spending increase. Those announcements also lifted our shares of Nvidia NVDA this week, joined by ServiceNow NOW, and Elastic ESTC.

On Wednesday, we boosted our price target on The Trade Desk TTD to $145, lifted our rating to One from Two, and picked up more shares for the portfolio. After reviewing quarterly results and a sizable dividend increase from American Express AXP, on Friday we increased our price target to $345 and laid out where we would be inclined to pick up more shares. In between, we shared some thesis-reaffirming comments from LG Display LPL for our position in Universal Display OLED.

Now let’s turn to what Wall Street had to say this week about the portfolio’s holdings:

DA Davidson upped its Alphabet GOOGL price target to $200 from $190.

Scotiabank lifted its Amazon AMZN price target to $306 from $246, and Raymond James raised its to $260 from $230.

Apple AAPL shares caught a few price target declines, with BofA lowering its target to $253 from $256, and Goldman Sachs trimming its to $280 from $286.

Piper Sandler reset its Mastercard MA price target at $591, up from $575, and TD Cowen boosted its to $599 from $567.

KeyBanc raised its Marvell MRVL target to $135 from $125 as it expects AI demand to remain robust. We share that sentiment, especially after this week’s developments.

BofA upped its Meta META target to $710 from $660, while Raymond James upped its by $50 to $725. On Friday, we read Meta’s Threads, which competes with X and Bluesky, is starting to test ads with a handful of brands. Should that move from testing to full launch, which we think is likely, it would give us and others a reason to revisit current price targets.

Following our price target boost to Morgan Stanley MS shares to $145 last week, early this week UBS increased its MS target to $140 from $130.

Bank of America increased its target for ServiceNow NOW to $1,280 from $1,074 and upped its target for Vulcan Materials VMC to $311. JMP Securities also lifted its ServiceNow target to $1,300 from $1,00. We’ll revisit our price target after NOW reports its earnings next week.

The Trade Desk TTD saw coverage initiated by JMP Securities with a $150 target and an Outperform rating.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Tuesday, January 21: Trump Returns and Earnings Season Can Shape These Four Holdings

Wednesday, January 22: Connecting the Dots on Trump's Stargate Announcement Across the Portfolio

Thursday, January 23: We're Prepared for Market Uncertainty After Trump WEF Address

Friday, January 24: Why We Could Be in for a Trump-Powell Showdown

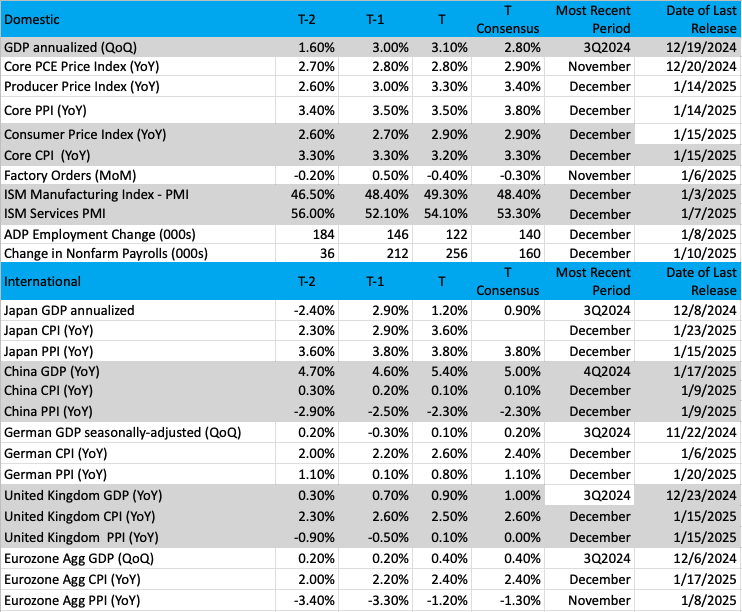

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Invesco S&P 500 Equal Weight ETF

When a market is trending upward, we like to see strength across all weight classes of stocks. Take the SPY and RSP, which are the S&P 500 weighted and equal-weighted ETFs, respectively. We have talked here about how important it is to see these two ETFs in sync or simply moving together.

Remember the descriptions here, the equal-weighted RSP pays no attention to the size of the company. Each member gets one vote, whereas the SPY is a market cap-weighted index that is priced based on the capitalization of all 500 stocks. As one would imagine, the names at the top of this list (highest value) have the most influence.

In recent years the separation of the SPY and RSP has been quite apparent on many occasions. Why is that? Well, simply put, the influence of a few names, the Magnificent Seven for instance, which skews the SPY to deliver gains more in line with those names.

So, when a divergence occurs, or when the SPY and RSP are moving in different directions then we need to examine the situation to figure out why. As pointed out in the chart, there was a period in December when the SPY was performing at a better rate than the RSP, but they both resumed their congruence later in the month and are now in sync.

Yet, the SPY price is more than 3x the price of the RSP, which tells us the valuation of the SPY is dominated by the influence of a few stocks. Can this continue? It certainly can continue as investors plow more capital into those dominant names.

The chart shows a nice symmetry for these two ETFs, with a double bottom being made simultaneously and liftoff into January for a new all-time high. The RSP, for its part, remains below the all-time high reached in December but is making up ground quickly and could be at a new high within days.

Other charts we shared with you this week were:

Monday, January 20: S&P 500 - S&P 500 Gets a Much-Needed Jolt

Tuesday, January 21: Bright Family Solutions (BFAM) - The Future Looks Rosy for This Bullpen Stock

Wednesday, January 22: Alphabet (GOOGL) - Don't Write Off Alphabet

Thursday, January 23: United Rentals (URI) - Can This Holding Move Above Resistance?

The Week Ahead

Next week brings the Fed’s next policy meeting and earnings from several key S&P 500 components, so it will be an important one for the markets. The week also closes out January and that means we will be paying close attention to the February 1 date, shared by President Trump, that could start a new wave of tariffs.

That potential should make for some interesting comments when Fed Chair Powell takes the podium Wednesday afternoon. No one expects the Fed to deliver a cut at that meeting or at its March one, but we could see Powell’s tone skew more hawkish following the inflation comments found in Friday’s January Flash PMI report. As we discussed in today’s video, this could set up a showdown between Powell and the Fed, which are determined to tame inflation, and President Trump, who during his World Economic Forum address said he will “demand” interest rates drop.

Moving through the Fed’s policy meeting and the wave of earnings we discuss below, we will keep a close watch on Trump’s tariff intentions, their possible timing, and implications. As some of that uncertainty fades, we’ll course correct the portfolio as needed.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, January 27

· New Home Sales – December (10:00 AM ET)

Tuesday, January 28

· Durable Orders – December (8:30 AM ET)

· FHFA Housing Price Index – November (9:00 AM ET)

· S&P Case-Shiller Home Price Index – November (9:00 AM ET)

· Consumer Confidence – January (10:00 AM ET)

Wednesday, January 29

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Advance Trade and Inventories – December (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Rate Decision – 2 PM ET

Thursday, January 30

· GDP – 4Q 2024 (8:30 AM ET)

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Pending Home Sales – December (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, January 31

· Personal Income & Spending, PCE Price Index – December (8:30 AM ET)

· Employment Cost Index – 4Q 2024 (8:30 AM ET)

International

Monday, January 27

· China: Industrial Profits – December

· Germany: IFO Business Climate & Expectations - January

Wednesday, January 29

· Japan: Consumer Confidence – January

· Germany: GfK Consumer Confidence - February

Thursday, January 30

· Germany: Flash GDP – 4Q 2024

· UK: Bank of England Consumer Credit – December

· Eurozone: Flash GDP – 4Q 2024

· Eurozone: Consumer Confidence, Economic Sentiment – January

· Eurozone: European Central Bank Interest Rate Decision

Friday, January 31

· Japan: Industrial Production, Retail Sales – December

· China: NBS Manufacturing & Non-Manufacturing PMI – January

· China: Caixin Manufacturing PMI – January

· Germany: Retail Sales – December

During the upcoming week, 102 S&P 500 companies and nine Dow 30 components are scheduled to report their quarterly results. What this means is exiting next week, roughly one-third of the S&P 500 basket will have been reported. However, when we look at some of the companies set to report next week, which are also portfolio holdings, such as Apple, Microsoft, Meta, ServiceNow, Lockheed Martin, United Rentals, Waste Management, and Mastercard, they account for over 15% of the S&P 500.

Layer in Tesla (TSLA), Visa (VISA), and a few others, and the tally of S&P 500 constituent weighting reporting next week easily pass 20%. This means it will be a big week for the S&P 500, with quarterly results and earnings guidance factoring heavily into 2025 EPS expectations for that market barometer.

As we digest those earnings reports as well as those from Boeing (BA), SAP SE (SAP), Qorvo (QRVO), Starbucks (SBUX), ASML (ASML), Lam Research (LRCX), Visa (V), Caterpillar (CAT), Intel (INTC) and others, we’ll be factoring their results and guidance into our investment mosaic.

Here's a closer look at the earnings reports coming at us next week:

Monday, January 27

· Open: AT&T (T), SoFi Technologies (SOFI).

· Close: Alexandria RE (ARE), Crane (CR), Nucor (NUE).

Tuesday, January 28

· Open: Boeing (BA), General Motors (GM), JetBlue Airways (JBLU), Kimberly Clark (KMB), Lockheed Martin (LMT), Paccar (PCAR), SAP SE (SAP), Synchrony Financial (SYF), Sysco (SYY).

· Close: F5 Networks (FFIV), LendingClub (LC), Qorvo (QRVO), Starbucks (SBUX).

Wednesday, January 29

· Open: ASML (ASML), ADP (ADP), Corning (GLW), General Dynamics (GD), VF Corp. (VFC).

· Close: Ameriprise Financial (AMP), IBM (IBM), Lam Research (LRCX), Levi Strauss (LEVI), Meta (META), Microsoft (MSFT), ServiceNow (NOW), Tesla (TSLA), United Rentals (URI).

Thursday, January 30

· Open: Altria (MO), Caterpillar (CAT), Check Point Software (CHKP), Comcast (CMCSA), Mastercard (MA), Mobileye Global (MBLY), Northrop Grumman (NOC), Pulte Group (PHM), Quest Diagnostics (DGX), UPS (UPS), Waste Management (WM).

· Close: Apple (AAPL), Beazer Homes (BZH), Intel (INTC), KLA Corp. (KLAC), PPG Industries (PPG), Visa (V).

Friday, January 31

· Open: Aon (AON), Chevron (CVX), Church & Dwight (CHD), Colgate Palmolive (CL), Eaton (ETN), Exxon Mobil (XOM).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.