Weekly Roundup: Portfolio Gains Ground Amid Key Data and News

During the week we booked a big, big gain on a financial position, and downgraded a chip stock, as markets hit new highs to start 2026.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The first full week of trading in 2026 was a positive one for the market and TheStreet Pro Portfolio.

While coming into this week there were ample questions following the U.S. move into Venezuela, both the market and the Pro Portfolio were initially propelled higher as CES 2026 got underway with keynotes from Nvidia (NVDA) and Advanced Micro Devices (AMD) . Both were upbeat on the topic of AI and data-center demand, but we Nvidia also shared its outlook for autonomous driving and robotics.

AMD CEO Lisa Su shared expectations for AI to go from 1 billion active users to 5 billion within five years. That raised our eyebrows and most likely a few others. We don’t get overly hung up on the precise numbers when figures like these are mentioned, but focus more on the vector and the velocity. In this case, those are “higher” and “fast.” That meshes with our thinking on AI adoption and usage across the enterprise, with consumers and other entities like federal, state, and local governments.

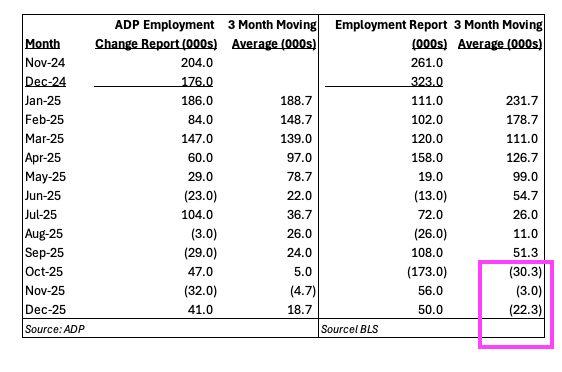

Wednesday was a big data day with ADP’s December Employment Change Report and ISM’s December Services PMI. Looking at those alongside Monday’s December Manufacturing PMI from ISM, it was clear the pace of job growth had remained tepid, but the Services side of the economy perked up as we closed out 2025. Indeed, the Services sector New Orders sub-index came in at 57.9, the highest reading since September 2024.

Friday, the December Employment Report came in weaker than expected, but as we discussed with you, the revisions to October and November jobs figures resulted in three-month trailing jobs data for each month in Q4 2025 being negative. Should next week’s inflation data come in cooler than expected, we could see Fed speakers become incrementally dovish ahead of the next Fed policy meeting later this month.

We also had several White House “moments” this week. The first, as mentioned, was tied with Venezuela, and as we suspected would happen, more time has led to more rational comments. We’ll continue to evaluate what’s ahead on that front. President Trump also blasted the defense industry for moving too slowly to produce equipment and ordered defense companies to stop stock dividends and buybacks. Shortly thereafter, Trump called for a record $1.5 trillion defense budget in 2027, up from $0.9 trillion in 2026.

Thursday, Trump ordered Fannie Mae and Freddie Mac to start buying up to $200 billion in bonds backed by mortgages. Details were modest, but on Friday, we did note that the difference between the interest rates on mortgage bonds and Treasuries narrowed by 0.1 percentage points, a sharp move in that market and an early indication that the initiative could have some effect on the mortgage market. Before we break out the champagne for the housing market, though, let’s remember that job creation has a hand in housing demand, and weak job creation does not suggest a vibrant housing market ahead.

What we did not get this week was the Supreme Court’s ruling on Trump’s tariffs. Expectations pointed to that as a potential development on Friday, but the justices did not release their opinion in the tariff case. The court, however, indicated its next opinion day would come on Wednesday, Jan. 14.

The net of the above led the S&P 500 to hit a new high on Friday. While we are happy to participate in that move higher, we continue to think the December-quarter earnings season will be the next determinant of the market’s direction. That means in addition to next week’s December inflation data and potential ruling on tariffs, big bank earnings and quarterly results from Taiwan Semiconductor (TSM) will be closely watched and dissected by the market and us.

Based on what those early reports say about what’s ahead, we’ll fine-tune the Portfolio’s exposure as needed.

Enjoy your weekend, and Saturday’s Signals alert. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio posted a greater-than-1% gain for the week due to double-digit gains in shares of Axon Enterprise (AXON) and United Rentals (URI) , as well as strong moves in Amazon (AMZN) , Costco (COST) , Alphabet (GOOGL) , and Palantir (PLTR) . The refreshed EPS Diplomats basket also rose week over week, continuing to outperform the S&P 500.

Those gains were mitigated somewhat by week-over-week declines in shares of Apple (AAPL) , Nvidia (NVDA) , Marvell (MRVL) , and ServiceNow (NOW) . Coming into January, we recognized Apple shares could trade sideways until the company unveils its updated, AI-enabled Siri. With Nvidia and Marvell, we continue to see rising AI adoption and usage driving demand for their chips, as well as networking and digital infrastructure. As such, we remain bullish on Arista Networks (ANET) despite the stock's decline this week.

On Monday, as continued strength in Bank of America (BAC) shares led to an outsized position in the Portfolio, we trimmed our exposure, locking in a gain of almost 99% on that slug of shares. With the IPO market and M&A activity poised to remain vibrant in the coming quarters, and the potential for loan activity to improve as the interest rates continue to move lower, we will remain owners of BAC to capture further upside. Based on the near-term tone of the IPO and M&A market, we may need to revisit our BAC price target as well as the one for Morgan Stanley (MS) . Both banks report next week.

On Friday, we downgraded our rating on shares of Qualcomm (QCOM) to Three from Two, and if you missed our note in which we laid out the reasons why we did that and our action plan, you can find both here. The same day, Mizuho downgraded QCOM shares to Neutral from Outperform, cutting its price target to $175 from $200. If guidance from Taiwan Semi (TSM) supports our concerns, odds are Qualcomm shares will become a source of funds as we look to bulk up other holdings with better near-term positioning and faster EPS growth prospects.

Companies on that short list include Broadcom (AVGO) , Arista Networks (ANET) , Microsoft (MSFT) , and Welltower (WELL) . We’d also note shares of ServiceNow (NOW) and Apple (AAPL) have dipped back into an oversold condition based on RSI figures, while the quick double-digit move in United Rentals (URI) so far in January has landed them in overbought territory.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Cantor Fitzgerald upgraded Alphabet to an Overweight rating from Neutral with a renewed price target of $370, up from $310. Canaccord also boosted its GOOGL target to $390 from $330. In our note on Wednesday, we explained our thinking that Wall Street may have underestimated Google and that could set up a nice upside surprise when it reports later this month. Should that be the case, and depending on its drivers, we may need to revisit our $350 target. And if we do, there will be more than a few joining us, given that the current market consensus target is at $334.

Evercore ISI increased its Apple target to $275 from $245, given what it sees as upside EPS prospects due to “robust” iPhone demand.

TD Cowen boosted its American Express (AXP) target to $375 from $350, and BofA upped its target to $420 from $410 on Friday. Goldman Sachs also boosted its AXP target, taking it to $420 from $400. We upped our AXP target to $385 in early December.

Shares of Arista Networks were upgraded to Overweight from Neutral at Piper Sandler with a $159 target.

Northcoast upgraded Axon shares to Buy from Neutral, slapping a new $742 target on them.

Mizuho lifted its Broadcom target to $480 from $450 as it continues to favor what it calls “AI accelerators.” AVGO shares are on our shopping list. Mizuho also increased its Nvidia target to $275 from $245.

Deutsche Bank resumed coverage on Costco shares with a Buy rating and a fresh $1,044 price target. COST shares were also upgraded to Outperform from Neutral at Mizuho with a $1,000 price target. In breaking down Costco’s December sales report, we explained why our patience with the shares was starting to pay off.

Barclays nudged its Dutch Bros (BROS) target to $76 from $72, citing a combination of persistent sales growth and quick service taking share from fast casual and casual dining.

Marvell shares were upgraded to Buy from Hold at Melius Research with a $135 target.

Wolfe Research upped its Morgan Stanley target to $211 from $198, calling the shares its top pick in the space. As the IPO market picks back up and as we digest the start of bank earnings next week, we’ll look to revisit our $185 target for MS. Yes, we’re aware the shares are trading around that level today, but we also know that before Morgan Stanley reports next Thursday, JPMorgan Chase (JPM) reports Tuesday, and Bank of America and Citigroup (C) on Wednesday.

Lucid Capital initiated coverage on SuRo Capital (SSSS) shares with a Buy rating and $12 target.

UBS resumed coverage of TJX Companies (TJX) with a Buy and a target of $184. UBS also increased its TJX price target to $193 from $181. If we see President Trump’s $2,000 stimulus checks become a reality, it would give us a reason to revisit our TJX target, which currently sits at $165, not too far from the market consensus one.

United Rentals caught an upgrade to Buy from Neutral at UBS with a new $1,025 target.

UBS also upgraded Waste Management (WM) shares to Buy from Neutral with a not-too-shabby $260 target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, December 5: We’re Contemplating a Potential Venezuela-Led Play

Tuesday, December 6: The Biggest Investor Takeaways From CES

Wednesday, December 7: CES Re-Energizes AI Trade, Puts 'Second Derivative' Tech Plays in Focus

Wednesday, December 7: Stocks & Markets Podcast: Peter Tchir on Geopolitics, Power Prices and ProSec

Thursday, December 8: Patience Pays Off With Costco, China’s Pending Nvidia Chip Approval

Friday, December 9: Let's Look Below the Surface of the December Jobs Report

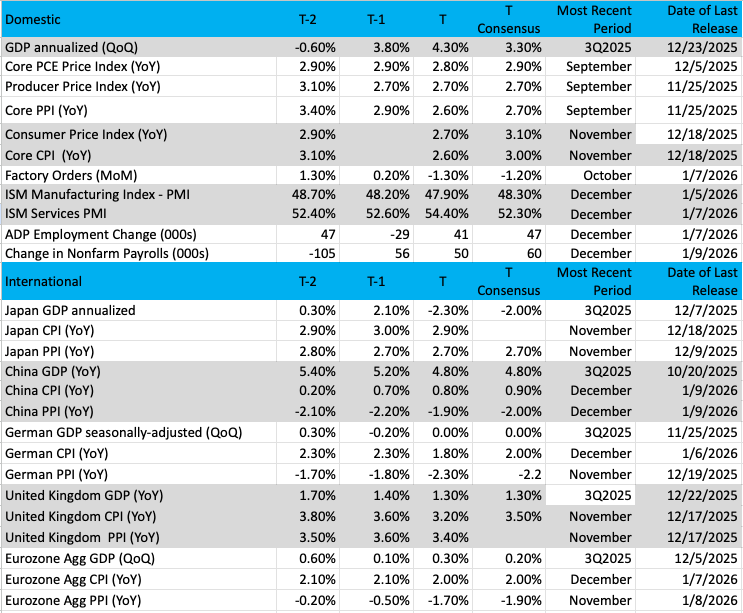

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

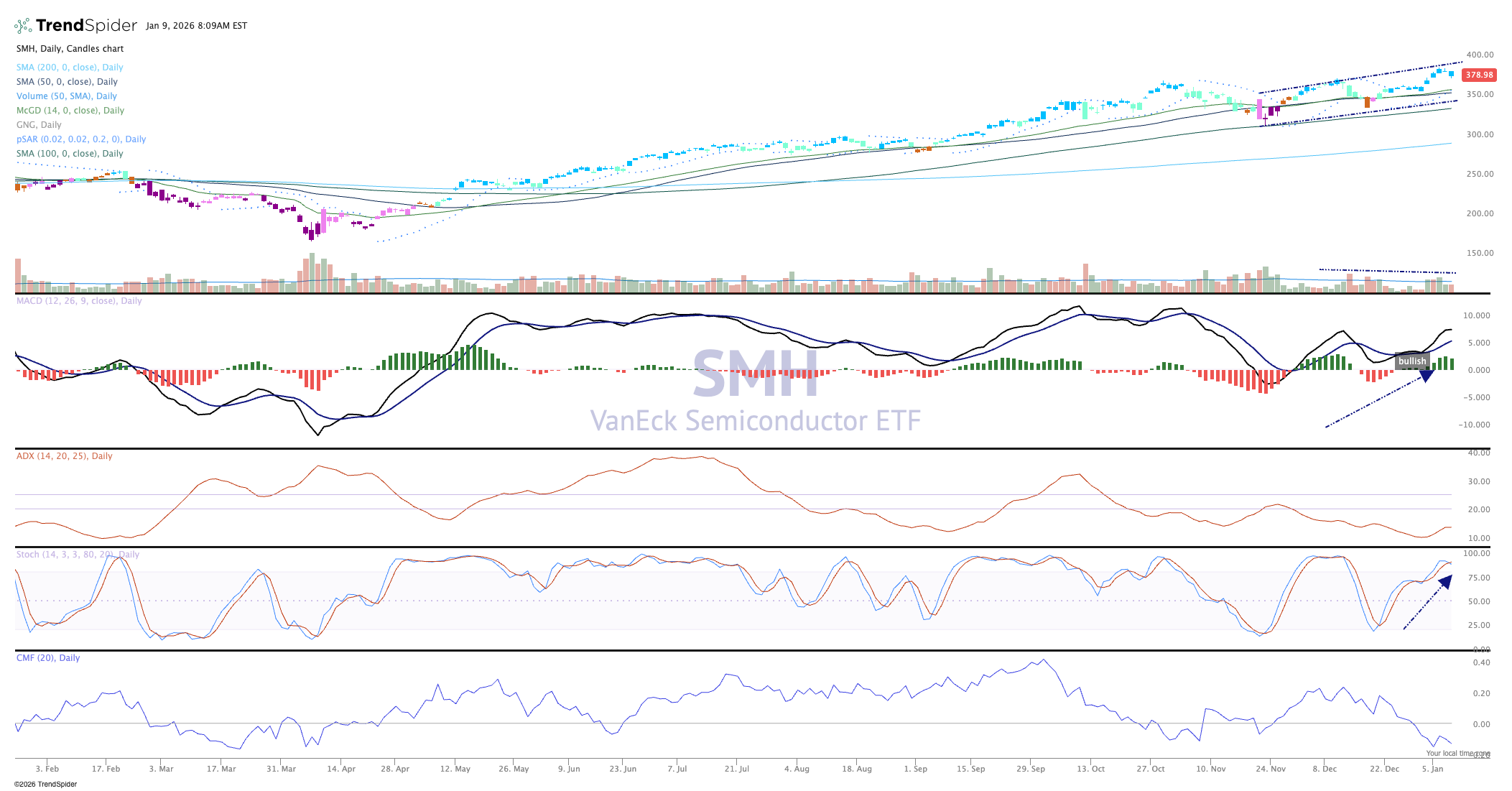

Chart of the Week: The VanEck Semiconductor ETF (SMH)

At TheStreet Pro Portfolio, we are huge fans of the semiconductor sector. We currently have roughly 10% of the Portfolio dedicated to semis, so occasionally it is nice to see how the entire group is doing based on the technical picture.

The fundamental view is well-documented, with new chips coming from Nvidia (NVDA) , support from other names, and new/exciting offerings from Marvell (MRVL) and Broadcom (AVGO) . We like to believe that having the biggest and best names in this group is the way to proceed, and we certainly house those names.

The (SMH) is the VanEck Semiconductor ETF, which represents the entire group, though it is modified cap-weighted. That means the performance is dominated by the most valuable companies in the universe of stocks but is not totally engulfed by a few. Still, one understands that Nvidia would have a strong influence.

The chart of the SMH is extremely bullish, with a series of higher highs and higher lows captured over the last couple of months. That uptrend remains intact, but the ETF is now overbought. What do we do with overbought? We understand this is a condition and not a signal, because overbought can stay that way for quite some time. The price channel is very bullish and looks to continue into this coming earnings season.

MACD (moving average convergence divergence) is on a buy signal, and momentum is strong by looking at the stochastics. The only fly in the ointment is weakness in money flows, but that is not horrible because investors choose to buy individual stocks rather than the ETF.

Other charts we shared with you this week were:

Monday, December 5: S&P 500: Can the Index Rise for a Fourth Straight Year?

Monday, December 5: Lumentum (LITE): This Holding Tops the List of New EPS Diplomats in 2026

Tuesday, December 6: Pan American Silver (PASS): Silver Breakout Powers This New EPS Diplomat

Wednesday, December 7: Morgan Stanley (MS): Morgan Stanley Buyers Stay in Control Ahead of Earnings

Thursday, December 8: Carvana (CVNA): Carvana Cruises Into the Portfolio

The Week Ahead

In getting ready for the week ahead, let’s first recap GDP expectations for Q4 2025, those for the current quarter, as well as what the market expects for Fed rate cuts.

Following this week’s data, the Atlanta Fed’s GDPNow model has a 5.1% figure for Q4 2025 GDP. The New York Fed’s Nowcast model was updated on Friday to 2.62% for Q4 2025 and 2.61% for Q1 2026 from the prior readings of 2.07% and 2.17%.

Ahead of next week’s December CPI and PPI readings, the CME FedWatch Tool sees the Fed’s next 25-basis point rate cut coming in June. Unlike the Fed’s December 2025 set of economic projections that penciled in one rate cut this year, the FedWatch Tool shows the market expecting a second one around the September-October time frame.

Following what we saw in the December Employment Report, softer inflation readings could lead to more dovish comments from Fed speakers next week. And as we think about the Fed, the central bank will enter its pre-policy meeting blackout period on Jan. 18.

Next week also brings us the next iteration of the NFIB Small Business Optimism Index and several pieces of fresh housing data. While the jobs data warrant staying on the sidelines when it comes to homebuilders, we will still want to monitor Existing Home Sales figures over the coming months as we approach the spring selling season. Should we see an uptick in that data set, especially for single-family homes, it would be a confirmation that repair and remodel spending is likely trending up.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, December 13

NFIB Small Business Optimism Index – December

ADP Employ Change Report – Weekly (8:15 AM ET)

Consumer Price Index – December (8:30 AM ET)

New Home Sales – September (10:00 AM ET)

Wednesday, December 14

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Retail Sales – November (8:30 AM ET)

Producer Price Index – November (8:30 AM ET)

Existing Home Sales – December (10:00 AM ET)

New Home Sales – October (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, December 15

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Import/Export Prices – November (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, December 16

Industrial Production & Capacity Utilization – December (9:15 AM ET)

NAHB Housing Market Index – January (10:00 AM ET)

International

Tuesday, December 13

Japan: Eco Watchers Survey Outlook - December

Wednesday, December 14

China: Imports/Exports – December

Japan: Machine Tool Orders - December

Thursday, December 15

Japan: Producer Price Index – December

Germany: Wholesale Prices – December

UK: GDP, Industrial and Manufacturing Production – November

Eurozone: Industrial Production - November

Friday, December 16Germany: Inflation Rate - December

While there will be a slow start to quarterly earnings next week, those companies reporting are important to watch. Once again, big banks will kick things off, and we will want to drink in what we hear about investment banking prospects, loan activity, and the consumer when JPMorgan Chase (JPM) reports on Tuesday. That will set the tone for Bank of America (BAC) and Morgan Stanley (MS) later in the week.

Tuesday also brings results from Delta Air Lines (DAL) , a long-term partner for American Express (AXP) . In addition to its comments about spending on air travel, we’ll be interested in what Delta says about its Delta-Amex co-branded card, including on spending and new card acquisitions.

Alongside quarterly results and guidance from Morgan Stanley on Thursday, given our tech holdings, we will be laser-focused on Taiwan Semiconductor's (TSM) guidance for the current quarter and beyond. We’ll be breaking down that outlook by end market for the first half of the year. Should it match the comments from Foxconn for continued AI and data center strength but seasonal weakness in smartphone, PC, and other end markets, we may opt to trim back the Portfolio’s exposure to Qualcomm (QCOM) .

Outside of quarterly earnings reports, we will be reviewing comments from Labcorp (LH) when it presents at the JPMorgan Healthcare Conference. And even though none of our holdings are presenting at the Needham Growth Conference, we’ll keep tabs on what is said from those that are, connecting the dots back to the Portfolio. We’ll have our other eye on the IPO market.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, December 13

Open: BNY Mellon (BK), Delta Air Lines (DAL), JPMorgan Chase (JPM).

Wednesday, December 14

Open: Bank of America (BAC), Citigroup (C), Wells Fargo (WFC)

Close: HB Fuller (FUL).

Thursday, December 15

Open: BlackRock (BLK), Goldman Sachs (GS), Insteel Industries (IIIN), Morgan Stanley (MS), Taiwan Semiconductor (TSM).

Close: JB Hunt (JBHT).

Friday, December 16

Open: PNC (PNC), State Street (STT).

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.