Weekly Roundup: Portfolio Accelerates as Market Continues to Defy Seasonality

Here's what happened with the Pro Portfolio during a week where the S&P 500 re-entered an overbought condition, but EPS expectations started to inch up for 2025 and 2026.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Another week in September has come and gone, and the market continues to move higher, with all four major market indexes pushing upward. Not only has the market continued to buck historical September performance, but the Pro Portfolio’s performance accelerated this week, benefiting from the combination of moves we made this week and in the last few months.

The week’s gains came as the Fed delivered the 25-basis point rate cut the market was looking for on Wednesday and penciled one more potential rate cut for this year in its latest set of economic projections compared to June. That brought the total number of potential 2025 and 2026 rate cuts to four, also one more than previously telegraphed. Granted, it was less than the market was expecting, but then again, recent economic data and rolling GDP forecasts, such as the Atlanta Fed’s GDPNow or the New York Fed’s Nowcasting models, continue to show the domestic economy remains on a firm footing.

The more than 1% increase for the S&P 500 led that closely watched market index to close at yet another record high this week. This week's gains also left the S&P 500 and the Nasdaq Composite in overbought conditions as their relative strength index levels (RSIs) closed the week above 70. We’ve seen this condition persist in individual stocks, but typically it doesn’t last as long with these market indexes. That means near-term caution is warranted, especially with the S&P 500 P/E valuation near 24.8x as we close out the week.

While that multiple is slightly below the 25.1x peak multiple the S&P 500 traded at in 2024, and the Fed looks to be entering a rate-cutting cycle, we continue to think an increase in expected EPS is needed to drive the market demonstrability higher from here. This past week, we did see a slight increase in consensus EPS figures for 2025 and 2026 for that basket of stocks, per data published by FactSet. The figure for 2025 now stands at $268.83 compared to $268.48 at the end of August. Not the biggest increase, but because of the economy’s continued resilience and prospects for rate cuts, this could be an inflection point to watch.

Again, that is for the market, and as we’ve seen this week, not all parts of the market move in the same direction. Clearly, housing continues to be one of the challenged areas, and with that in mind, we will continue to follow where companies and consumers are spending. We will also continue to focus on multi-year structural changes and pain points, and the companies poised to deliver superior EPS growth relative to the S&P 500 because of them.

While we didn’t necessarily frame it that way, we can say the Pro Portfolio’s newest position in Welltower WELL checks all those boxes. It’s opportunities like those we’ll be hunting for, and we’ll continue to take advantage of ones tied to existing positions. As we discuss below, we did that a few times this week.

Enjoy an easy weekend, and we say that because we are giving you a reprieve. That’s right, we are taking a break from Saturday Signals and Sunday Soup so we can get an early jump on the September Monthly Roundup we’ll be publishing on September 26. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio continued to gain over the last week, in part as the overall market moved higher. However, the week’s outperformance in Marvell MRVL, Palantir PLTR, American Express AXP, Alphabet GOOGL, and Apple AAPL led us to gain ground on the S&P 500’s year-to-date return. Those individual gains more than offset the pullback in Dutch Bros BROS and more modest declines from Costco COST, SuRo Capital SSSS, and Nvidia NVDA. With seven trading days left in the current quarter, the Pro Portfolio is up more than 13% on a year-to-date basis with ~9% of its assets in cash.

On Tuesday, we used the overbought condition in Alphabet and Morgan Stanley MS to lock in some very outsized gains in GOOGL shares and an almost 96% in that slug of MS shares. As we explained in the Alert to you, even after those trades, the Portfolio continued to have sizable positions in both stocks because we continue to see more upside ahead for both.

On Thursday, we scooped up additional shares of Dutch Bros and Universal Display OLED, but we also started a new position in Welltower WELL with an initial price target of $190. As we explained in that trade, should WELL shares either fall back to support near the 100-day moving average, near $157, or if the company can achieve stronger-than-expected margin gains that drive faster net operating income (NOI) and funds from operations (FFO), prompting us to revisit our price target, we would look to reconsider our initial Two rating.

Later on Thursday, we boosted our price target for American Express AXP to $370 from $340 after the company shared details on its long-awaited Platinum card refresh. The company packed on the perks, which makes the increased annual fee easily digestible, in our view. Let’s remember that just like we have seen at Costco, the impact of this card refresh will be a phased-in one as membership renewals occur over the coming quarters. As we see the average card fee tick higher, we will review our price target and our current Two rating as needed, especially if the number of cards in force grows faster than expected. Given the value to members, even after the announced Platinum fee increase, we would not be surprised if it happens.

On Friday, we made a few other price target adjustments, upping Morgan Stanley's and Bank of America's to $170 and $60, respectively, and increased our Palantir price target to $205 from $200.

As we turn to the remaining seven trading days in the quarter, the aggregate moves detailed above leave the Portfolio with 26 positions in play, and roughly 9% of its holdings in cash. With the S&P 500’s RSI level back above 70 as we closed out the week, and the Nasdaq’s even higher, we will remain very selective when it comes to putting that cash to work near-term. We will also continue to track RSI levels for individual Portfolio holdings, and if the prudent thing to do is to convert those gains into cash, you know we’re not afraid to make that decision.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during this busy week for the market:

Monday, Bernstein initiated coverage of Apple AAPL shares with an Outperform rating and a $290 price target. Evercore ISI lifted its Welltower price target to $183 from $175. Melius Research upgraded Eaton ETN to Buy from Hold with a $495 target, up from $412.

Tuesday, citing favorable credit card spending data, Truist increased its Amazon AMZN target to $270 from $250. Wells Fargo boosted its Morgan Stanley price target to $165 from $145 and lifted its Bank of America target to $50 from $56.

On Wednesday, Tigress Financial lifted its Apple price target to $305 from $300, calling for continued Services growth as the company continues to expand its ecosystem. Citi reiterated its Buy rating on Waste Management WM with a new $268 target.

Thursday, Piper Sandler increased its Alphabet target to $285 from $220, which is a bit of a catch-up from the recent antitrust ruling but also a call on Search re-accelerating in 2026. UBS named Dutch Bros a top consumer sector pick, “given industry-leading store growth and ongoing sales and traffic momentum likely sustainable through 2H25 and ’26.”

Noted Apple analyst Ming-Chi Kuo said Apple will bring an organic light-emitting diode display MacBook Pro out in 2026 with expected shipments of 6-8 million in 2026 and 20-25 million in 2027. The same day, Nikkei Asia reported Apple is working on a test production line for the expected foldable iPhone

On Friday, Barclays initiated coverage on Waste Management with an Overweight rating and a $272 target. UBS also initiated coverage on our newest holding, Welltower, with a Buy rating and a $195 price target.

JPMorgan bumped up its Apple price target to $280 from $255, citing “favorable demand indications” for iPhone 17 models and positive anticipation of a foldable iPhone in 2026. We continue to see Universal Display as a direct beneficiary. Citizens JMP boosted its Alphabet target to $280 from $250, and Citi upped its Bank of America target to $58 from $54.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, September 15: It’s Fed Week, But So Much More, Too

Wednesday, September 17: How Many Rate Cuts Will the Fed Telegraph?

Thursday, September 18: Let’s Talk More About the Fed Decision and Today’s Trades

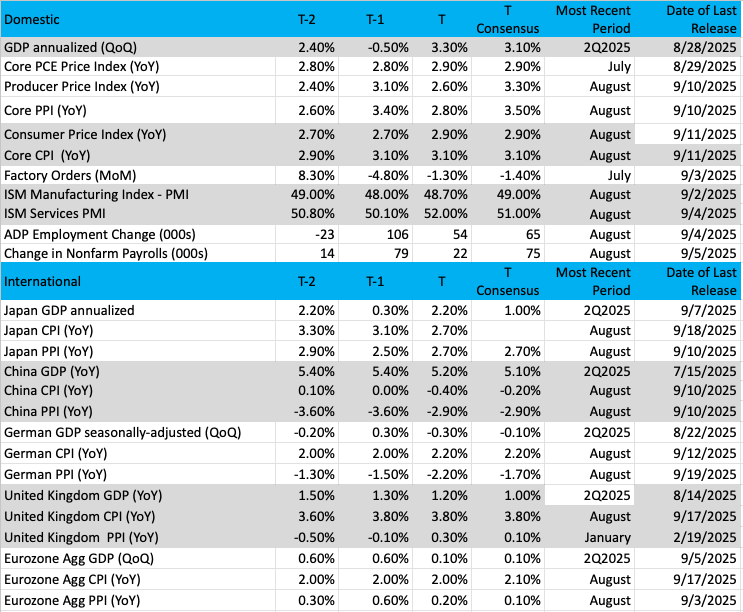

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

Chart of the Week: The iShares Russell 2000 ETF

Small-cap stocks are not looking that small any longer!

After closing this week at an all-time high, the Russell 2000 ETF IWM is sitting pretty here with its sights set on more gains. Fueled by strong volume trends, this index has a nice tailwind behind it. The IWM has rallied smartly since crashing in early April; the IWM has risen some 43% over the past 5 ½ months. That is some performance.

This past week’s action by the Federal Reserve will also serve to guide the IWM even higher. Lower interest rates are critical to small-cap companies that need lower borrowing costs to thrive and survive in a tough business environment. The most recent projections by the Fed indicate two more cuts are likely this year, one in 2026 and one in 2027 (which we believe is likely pulled into 2026).

That sets the table for a strong finish in 2025 by the small-caps, which have been lagging the Nasdaq and S&P 500 the entire year.

But wait, there is more! When the small-caps lead, it tends to drag up the other indexes, so look for continued good performance by the bigger-cap indexes to follow. Sounds too good to be true. Historical performance makes this a strong possibility, so hold onto your bullish positions for now.

The chart of the IWM is remarkable. Higher highs, higher lows in place since the spring show the strong uptrend of this index. This daily chart also shows a high level on the ADX, which tells us the prevailing trend is very strong.

Money flow has backed off a bit, but the MACD (moving average convergence/divergence) remains on a buy signal. The candles have mostly been blue for months, indicating strong bullishness on the GoNoGo composite of indicators.

Other charts we shared with you this week were:

Monday, September 15: S&P 500 – No Denying the Bulls This Time

Monday, September 15: Waste Management (WM) – Waste Management Dips

Tuesday, September 16: ServiceNow (NOW) – ServiceNow is Building the Bullish Case

Wednesday, September 17: American Express (AXP) – American Express Breaks Free

Thursday, September 18: First Trust Nasdaq Cybersecurity ETF (CIBR) - Cybersecurity Stocks Start to Perk Up

The Week Ahead

As we move deeper into the back half of September, we have a modest amount of August economic data coming at us, including a few new pieces for the housing market. We will examine those findings and continue to evaluate what they reveal, including consumer demand and inventory levels.

Coming off the Fed’s policy decision this past week and the number of rate cuts telegraphed in the updated set of economic projections, the data set we’ll be more focused on next week is the September Flash PMI from S&P Global. This will be the first hard look at economic data for the month and one that covers several key areas like inflation, job creation, and new order activity. What’s revealed in that report will help us assess the likelihood of the Fed delivering on those potential rate cuts, especially the one expected for October 29.

We will also see the return of Fed speakers next week, and their comments should bring some additional color to the Fed's decision and updated projections. We’ve already heard from Federal Reserve Bank of Minneapolis President Neel Kashkari that he supported this week's decision to cut the U.S. benchmark short-term interest rate by a quarter of a percentage point. Kashkari also believes that same-sized rate cuts at each of the Fed's final two meetings of the year will be appropriate. Back in June, Kashkari shared expectations for two quarter-point rate cuts.

We recognize Kashkari’s comment for three rate cuts this year should be viewed as a snapshot in time, one that could change, subject to incoming data. Rest assured, we will continue to puzzle through the data and follow what it says about the pace of the economic growth, job creation, inflation, housing, consumer spending, and other parts of the economy. Should that data strongly suggest something other than what is found in the Fed’s September set of economic projections is unfolding, we’ll make adjustments to the Pro Portfolio as needed.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, September 22

· Chicago Fed National Activity Index – August (8:30 AM ET)

Tuesday, September 23

· S&P Global Flash PMI – September (9:45 AM ET)

· Existing Home Sales – August (10:00 AM ET)

Wednesday, September 24

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· New Home Sales – August (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, September 25

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Advanced Inventories, Retail and Wholesale – August (8:30 AM ET)

· Durable Orders – August (8:30 AM ET)

· GDP – Q2 2025 (3rd estimates) (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, September 26

· Personal Income & Spending, PCE Price Index – August (8:30 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – September (10:00 AM ET)

International

Tuesday, September 23

· Eurozone: HCOB Flash PMI – September

· UK: S&P Global Flash PMI - September

Wednesday, September 24

· Japan: S&P Global Flash PMI – September

· Germany: Ifo Business Climate and Conditions - September

Thursday, September 25

· Eurozone: New Car Registrations – August

· Germany: GfK Consumer Confidence – October

· Eurozone: Loans to Companies, Households - August

We have a modest increase in the number of companies reporting quarterly results next week. Among the bunch is our own Costco COST, and based on the company’s monthly revenue reports, it should be a nice one. When we review the results, we will read between the membership fee revenue and member metrics to look for a pickup in the average membership fee. That, along with membership renewal statistics, will confirm Costco is benefiting from its membership price increase last year. We’ll also be looking for an update on warehouse expansion plans, a leading indicator for that high-margin membership fee revenue stream.

Comments from Micron MU will bring additional color on data center demand as well as refine H2 20205 expectations for PC and smartphone demand. When we examine Accenture’s ACN results, AI adoption will be a focal point for us, while in BlackBerry’s BB, it will be comments on corporate cybersecurity spending and matriculation of its automotive design wins, including those for advanced driver assistance systems (ADAS). And as we discussed on Friday, we will be digging into quarterly numbers from KB Home KBH and what those results reveal about housing demand and the company’s homebuilding margins.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, September 23

· Open: AutoZone (AZO),

· Close: Micron (MU)

Wednesday, September 24

· Open: Cintas (CTAS), Thor Industries (THO),

· Close: KB Home (KBH)

Thursday, September 25

· Open: Accenture (ANC), CarMax (KMX),

· Close: Blackberry (BB), Costco (COST)

Friday, September 26

· Open: Carnival (CCL).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.