Weekly Roundup: Our Game Plan as Earnings Heat Up and Trump Takes Office

The moves we made this week helped expand the portfolio's year-to-date lead over the S&P 500.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It may be hard to fathom, but we’ve already put the first half of January into the rear-view mirror. The stock market found its footing this week, took a step back and then rebounded Friday to close out the week. Meanwhile, we are moving further into December-quarter earnings season and the volume of reports is set to explode over the next few weeks.

Typically, the pace of things becomes frenetic during this period as we update our investment mosaic. Adding to that hectic pace, this time around we have the added “benefit” of President Trump taking office, which is expected to bring a potential tidal wave of executive orders. Those will give us much to think about, as will the Fed as its newly installed Federal Open Market Committee prepares for its late January monetary policy meeting.

As we traverse those and other upcoming events as well as data releases, we’ll reflect on the implications for TheStreet Pro Portfolio’s holdings, in addition to other factors, such as the dollar, inflation, and the 10-year Treasury yield, that could influence our strategy and the overall market. We adjusted our panic points earlier this week, and we’ll start next week off by sharing another round of updates following some of the sizable moves across the portfolio’s holdings this week.

With just under 9.5% of the portfolio’s assets in cash, we have sufficient capital to be opportunistic but given the sheer volume of information coming at us, we’re going to utilize a key carpenter phrase — “measure twice, cut once” — before making any moves. More confirmation boosts conviction, and we’d rather have that than get caught in a round or two of conflicting information.

In short, we’ll be sticking to our playbook — looking for opportunities in well-positioned companies at favorable risk-to-reward adjusted entry points, remaining disciplined investors as we do so.

Remember, U.S. equity markets are closed on Monday. Rest up for what’s ahead and enjoy it because the next market holiday isn’t until February 17.

As you do that, do me a favor and check out the portfolio’s “ripped from the headlines” signals Alert on Saturday. I think you’ll find them supportive of what we’re doing at the portfolio and with its holdings. Then swing by again on Sunday for a fresh collection of articles, streaming ideas, and things that caught out attention this week. And if you have yet to vote in our latest member poll, be sure to do so, and we’ll share the results on Tuesday.

Catching Up on the Portfolio This Week

The positive move in the market was felt throughout the TheStreet Pro Portfolio, expanding our lead against the S&P 500. Notable contributors included the double-digit gains registered by Applied Materials AMAT, Morgan Stanley MS, and United Rentals URI as well as strong moves for Vulcan Materials VMC, Marvell Technology MRVL, American Express AXP, and ServiceNow NOW.

A few positions were relative drags on the portfolio, including Apple AAPL and Meta META but based on Apple leading the smartphone shipment pack in Q4 2024 and the ongoing shift to digital advertising, we’ll remain owners of both.

We discussed that we were looking for opportunities to put some of our recently returned capital to work. We did just that on Tuesday following the better-than-feared December PPI report, scooping up additional shares of American Express, ServiceNow, Universal Display OLED, and United Rentals. Tuesday afternoon we boosted our price target on Dutch Bros BROS to $65 from $60, and on Thursday we did the same for Morgan Stanley, lifting our target to $145 from $140.

We also saw a mini-wave of M&A activity with deals announced by United Rentals on Tuesday, The Trade Desk TTD on Thursday, and ServiceNow on Friday. We view this as confirming the robust investment banking pipeline discussed by a variety of big banks when they reported their quarterly earnings this week. As those pipelines become executed transactions, we’ll adjust our MS and Bank of America BAC price targets as needed.

As the pace of earnings season heats up, odds are we will sit on the sidelines when it comes to putting capital to work. The reason for that is we want to test the earnings waters as a wider array of companies start to report. Next week also brings Inauguration Day and that means President Trump will start to make his policy agenda known. We’ll mostly be in "collect and dissect" mode next week, but will keep our eyes open for any glaring opportunities that present themselves.

Now let’s turn to what Wall Street had to say this week about this week about the portfolio’s holdings:

BMO Capital increased its price target on Amazon AMZN to $265 from $236 as it sees growth accelerating at Amazon Web Services and continued adoption of the company’s Same-Day/Next Day retail offering. BMO also upped its Trade Desk TTD target to $160 from $125.

KeyBanc upgraded shares of Applied Materials AMAT to Overweight from Sector Weight with a $225 price target following Taiwan Semiconductor telegraphing a far greater capital spending increase for this year than Wall Street anticipated.

Evercore ISI added Apple AAPL to its “Tactical Outperform” list, saying it expects to see a “stronger for longer” iPhone cycle. That thinking matches ours as Apple continues to bring more Apple Intelligence features to market in the coming quarters.

Bank of America BAC shares saw some price target adjustments, with Argus and Truist boosting theirs to match ours at $53, while Oppenheimer upped its to $55 from $54.

Jefferies lifted its price target for Dutch Bros BROS to $69 from $60.

Barclays made a few price target adjustments, boosting its Nvidia NVDA target to $175 from $160, resetting its Marvell MRVL target at $150 from $115, and bumping its Mastercard MA target to $595 from $576.

Cantor Fitzgerald started ServiceNow NOW with an Outperform rating and a $1,332 target this week. It also initiated coverage of Microsoft MSFT with a $509 target and an Outperform rating.

Lockheed Martin LMT shares fetched a new Buy rating at Truist, which included a $579 price target. The firm argues the Department of Government Efficiency is not “Sequestration 2.0” and sees a very low probability of the F-35 program being curtailed in the near term.

BofA boosted its Marvell MRVL target to $150 from $140, primarily to reflect Marvell’s long-term AI share potential. The firm also upped its Morgan Stanley MS target to $153 from $146.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, January 13: We’re Looking for Opportunity Amid the Market Selloff

Tuesday, January 14: Why This Holding Is Moving Higher and How We're Reacting

Wednesday, January 15: Predicting Next Fed Policy Decisions With Bob Lang

Thursday, January 16: Why We Like This Holding's New Acquisition

Friday, January 17: Why We Boosted Our Price Target for This Financial Holding

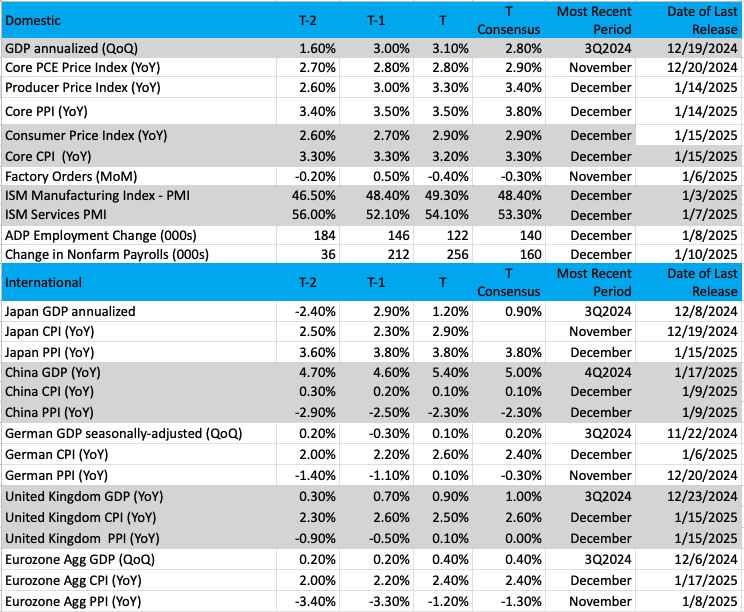

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: US Global Jets ETF (JETS)

The US Global Jets ETF JETS covers all the major airlines and some smaller carriers as well. The group has performed well since last summer, rallying some 52% since that bottom was put in early August. Notice the change in candle color at the turn on August 7 from purple to pink — still bearish but improving.

When the candles finally moved to blue (strong bullish) in early September the buyers were coming out in droves. The nice, steady move in this ETF is indicative of the major airlines’ strength and pricing power.

Recent earnings from Delta Air Lines (which posted strong numbers and even better guidance for 2025) reflect a strong economy, good pricing, and full flights. Wage growth notwithstanding, the sector remains one of the best performers in the S&P universe, receiving a grade of A+ in group Relative Strength (Investor’s Business Daily).

The technical indicators are very bullish, as one would expect with an ETF in a strong uptrend. A series of higher highs, and higher lows is our textbook definition of an uptrend.

MACD (moving average convergence/divergence) has flattened out but is now on a buy signal. Money flow is robust, but the stochastics (momentum) remains bullish. Recent tests of the McGinley Dynamic were successful.

We could see this ETF make a run at $30 before too long.

Other charts we shared with you this week were:

Monday, January 13: S&P 500 - S&P 500 Pulls Back to Critical Level

Monday, January 13: Bank of America (BAC) - Bank of America Tries to Fight the Bearish Trends

Tuesday, January 14: Universal Display (OLED) - Universal Display Flickers, But Don't Look Away

Wednesday, January 15: Dutch Bros (BROS) - Dutch Bros' Outlook Sweetens

Thursday, January 16: First Trust Nasdaq Cybersecurity (CIBR) – A CIBR Glitch

The Week Ahead

We have another shortened week coming up with U.S. equity markets closed for the Martin Luther King, Jr. holiday on Monday, January 20. That is also Inauguration Day and we could see incoming President Trump tip his hand with his inaugural address.

If he doesn’t do that, we are still likely to see a wave of activity as the new administration takes hold. Reports late this week indicate Trump is planning to issue around 100 executive orders on his first day in office. Some are calling this a “shock and awe campaign," but we see it as a potential policy tsunami that could run the gamut from budget cuts, immigration, trade issues, tariffs, and energy policy to reversing the Supreme Court TikTok ban to something on crypto. As we navigate the landscape, we’ll share our thoughts and make any necessary portfolio adjustments.

That activity will make up for a light economic calendar next week. Candidly, the report we are anxiously awaiting is the Flash January PMI report from S&P Global. It’s the first serious look at how the U.S. economy performed during the month, which means it will help shape GDP expectations for the current quarter. What it says about new order activity and hiring will contribute to those formulations, while the insight on inflation and prices will impact January CPI, PPI, and other inflation projections.

With a lack of Fed speakers next week as the central bank gears up for its January 28-29 policy meeting, that report will be one of the last ones we get before that meeting. While the market does not expect any Fed action to result from that meeting, what the Flash January PMI report finds, together with the December CPI and PPI reports, could have some influence over the language choice at Fed Chair Powell’s January 29 press conference. As such, we’ll be digging into those findings and figures closely.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, January 20

· US equity markets are closed for the Martin Luther King holiday

· Inauguration Day

Wednesday, January 22

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Leading Indicators – December (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, January 23

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, January 24

· S&P Global Flash Manufacturing & Services PMI – January (9:45 AM ET)

· Existing Home Sales – December (10:00 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – January (10:00 AM ET)

International

Monday, January 20

· Japan: Machinery Orders, Industrial Production – November

· Germany: Producer Price Index - December

Tuesday, January 21

· China: Foreign Direct Investment – December

· Eurozone: ZEW Economic Sentiment Index - January

Thursday, January 23

· Eurozone: Consumer Confidence (Flash) - January

Friday, January 24

· Japan: Inflation Rate – December

· Japan: Bank of Japan Interest Rate Decision

· Japan: Jibun Bank Flash Manufacturing & Services PMI – January

· Eurozone: HCOB Flash Manufacturing & Services PMI – January

· UK: S&P Global Flash Manufacturing & Services PMI – January

Even though we have a shortened trading week coming up, we will see the volume of corporate earnings reports jump considerably. Among the more than 280 expected reports, 43 S&P 500 constituents and six Dow 30 components are scheduled to deliver their quarterly results and guidance next week.

While the only portfolio holding scheduled to report is American Express AXP late in the week, we will work through the other reports coming at us. Our goal will be to collect insight, data points, and other useful nuggets as we get ready for more holdings to issue their quarterly results.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, January 21

· Open: 3M (MMM), Charles Schwab (SCHW), DR Horton (DHI), Logitech (LOGI)

· Close: Capital One (COF), Netflix (NFLX), United Airlines (UAL)

Wednesday, January 22

· Open: Abbot Labs (ABT), Johnson & Johnson (JNJ), Procter & Gamble (PG), Textron (TXT)

· Close: Alcoa (AA), Discover (DFS), Waste Connections (WCN)

Thursday, January 23

· Open: Alaska Air (ALK), American Airlines (AAL), GE Aerospace (GE), McCormick (MKC), Union Pacific (UNP)

· Close: CSX (CSX)

Friday, January 24

· Open: American Express (AXP), Ericsson (ERIC), HCA (HCA)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.