Weekly Roundup: Off to a Good Start Despite Santa Arriving Too Late

Here's our game plan as we move past the holidays with CES and earnings season on deck.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This week we closed the books on 2024, which was a great one for the TheStreet Pro Portfolio, and reset the performance clocks and metrics back to zero. For the first two days of 2025, our holdings regained some of the lost ground from December, and that led the overall portfolio to lead the S&P 500 out of the starting blocks for this year. While we are off to a good start, let’s remember that two days does not make a month or a quarter, let alone a year.

While the stock market rallied on Friday, it wasn’t enough to secure a Santa Claus rally given the declines in late 2024 and a weak start to the new year on Thursday, January 2. We discussed this possibility in Thursday’s video but also reminded members there are potentially other seasonal factors at play for the market and its watchers. We’ll see how the “first five days” indicator develops next week but while we’ll be mindful of that and other seasonal factors, we will continue to focus on companies with multi-year structural tailwinds that have superior earnings prospects. That means continuing to do what we got right last year and learning from what we could have done better in 2024.

Moving past the usual lull from the year-end holidays, things will start to pick up next week, due in part to CES 2025. Things will accelerate further the following week as the December-quarter earnings season begins and we will face another leg up the week after that. Factor in the usual monthly economic data and Fed heads returning to the public stage, and it means we will be back in the swing of things after two slower-paced weeks. That will see us taking a refreshed look at consensus EPS expectations for the S&P 500 as well as the portfolio’s holdings early next week.

Newer members to the portfolio, welcome aboard, and for those who were with us through 2024, we look forward to sharing our thoughts, insights, and portfolio moves with you over the coming year!

Enjoy the weekend, and be sure to read our Saturday signals, and Sunday Soup! We’ll see you back here on Monday.

Catching Up on the Portfolio This Week

After multiple moves during Christmas week, we only made one this week and that was to pick up some additional shares of ServiceNow NOW. Following that trade, the portfolio’s cash position is around 8% of its assets. This offers some additional firepower to be opportunistic, and we will continue to keep a close eye on the shares of Marvell Technology MRVL, Nvidia NVDA, and Amazon AMZN, which are approaching 4.5% of the portfolio’s assets. Should further gains in those shares push them past that level, it may lead us to some prudent register ringing.

We also boosted our price target for First Trust Nasdaq Cybersecurity ETF CIBR to $72 from $68 following word the U.S. Treasury Department was hacked. In our Alert, we also explained what could lead us to revisit the current Two rating on CIBR.

Now let’s review what others on Wall Street had to say about the portfolio’s holdings this week:

Bernstein boosted its Apple AAPL price target to $260 from $240 given improving IT hardware spending prospects.

Oppenheimer lowered its Bank of America BAC target to $54 from $57 due to “model tweaks,” but the firm kept its "Outperform" rating on the shares. Counterbalancing that move, Wolfe Research increased its BAC target to $54 from $50.

Evercore ISI also lifted its Bank of America target to $53 from $45 and upped its Morgan Stanley MS target to $140 from $133.

RBC boosted its Eaton ETN price target to $392 from $374, putting it that much closer to our $400 target. RBC explained secular drivers like electrification, reshoring, and data center growth were behind the increase. RBC also increased its price targets on The Trade Desk TTD to $140 from $136 and ServiceNow NOW to $1,210 from $1,045.

Wolfe Research also boosted its Trade Desk target, resetting it at $155 from the previous $140. The firm also hoisted its Meta META target to $730 from $670 and said Amazon AMZN is also among its top picks as it lifted that target to $270 from $250.

BofA reiterated a "Buy" rating on "sector top pick" Nvidia NVDA ahead of the CES tradeshow that starts January 6 with a keynote and other events featuring CEO Jensen Huang. We talk more about what we expect from this year's CES in The Week Ahead section below.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, December 30: Here’s Our Plan for This Oversold Portfolio Holding

Tuesday, December 31: Closing Out 2024, a Great Year for the Portfolio

Thursday, January 2: Here's What We’ll Be Assessing as the Market Focuses on Seasonal Indicators

Friday, January 3: We Have Margin Concerns for Food and Restaurant Companies

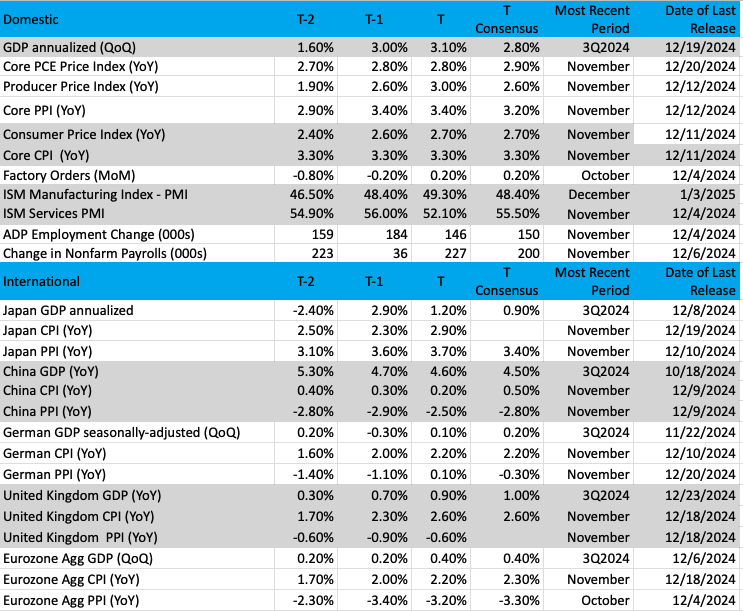

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Roundhill Magnificent Seven ETF (MAGS)

One of the most widely followed group of stocks over the past couple of years has been the Magnificent 7 (Mag 7). This group of stocks, which includes portfolio names Meta Platforms META, Microsoft MSFT, Apple AAPL, Alphabet GOOGL, Nvidia NVDA, and Amazon AMZN has been the "go to" for investors. No question that this group (which also includes Tesla TSLA) is responsible for the lion’s share of performance for the Nasdaq 100 and S&P 500 the past two years. Combined returns for 2023/24 in the Nasdaq 100 were near 80%, dominated by this headstrong group.

But how long will the Mag 7 continue to lead? Can this narrowness of the market be healthy or lead to something more ominous? There was a time during the 1970’s period when the so-called "Nifty 50" was all the rage. Investors climbed over each other to buy more of these stocks such as Coke (KO), General Electric (GE), IBM (IBM), and others. This group of stocks reached a very high valuation, eventually crumbling under its own weight. Can this happen to the Mag 7? Most certainly, but for now, the growth is there whereas the Nifty 50 stocks did not quite have the earnings power (at the time).

But let’s move forward and leave the history books behind. The MAGS is an ETF that tracks these names. We look at the Roundhill Mag Seven ETF, which shows a chart of higher highs, and higher lows. That is our textbook definition of an uptrend. But other indicators have turned lower, the month of December was not kind to any stock, especially the Mag 7. But there is an opportunity here, as we like the six names from this ETF we have in the portfolio.

If the MACD (moving average convergence/divergence) can turn higher and some momentum returns for this group, they are big enough to pull the entire market up.

Other charts we shared with you this week were:

Monday, December 30: S&P 500 - It's Been a Steady Ride in 2024

Monday, December 30: Costco (COST) – Costco’s on Sale

Tuesday, December 31: Lockheed Martin (LMT) - This Holding Is in Need of Some Jet Fuel

Thursday, January 2: Meta Platforms (META) - Lost in the Meta-verse

Friday, January 3: ServiceNow (NOW) - This Holding Is Displaying a Good Pattern to Follow

The Week Ahead

We’ve tippy-toed into 2025 with two trading days under our belt and things will pick up next week even though U.S. equity markets are closed on Thursday, January 9, for a National Day of Mourning following the recent passing of President Jimmy Carter.

Our economic data focus will be on the December Service PMI reports from ISM and S&P Global and what they tell us about the part of the economy that has been carrying the overall U.S. economy and inflation pressures. Piecing those together with this week’s December Manufacturing PMI reports should give us a more complete picture of where the economy stands.

Helping round out that picture will be multiple looks at job creation and wage gains during December. Those will come courtesy of ADP’s December Employment Change Report, the December Challenger Job Cuts Report, and the December Employment Report. The two things we’re looking to determine in that collected data are whether the pace of job creation remains robust enough such that the Fed doesn’t need to rescue it and if wage pressure looks to keep inflation data sticky.

Alongside those reports, we expect a spotlight will be put on the Tech sector starting Monday, January 6, when 2025 CES kicks off with a keynote from Nvidia’s Jensen Huang. The CES event will run through Friday, January 10, and the first 48 hours tend to be the busiest from a new product and press release perspective. Keynotes this year include presentations from Delta Air Lines (DAL), Volvo (VOLVY), Waymo, and X with other presentations from Netflix (NFLX), Mastercard (MA), Comcast (CMCSA), and others. If history holds, the event will introduce a variety of new consumer technology products ranging from PCs and smartphones to other connected devices. Our thinking is the event should be a positive for several of the portfolio’s holdings, notably Universal Display OLED and Qualcomm QCOM.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, January 6

· S&P Global Services PMI (Final) – December (9:45 AM ET)

· ISM Services PMI – December (10:00 AM ET)

· JOLTS Job Openings & Quits – November (10:00 AM ET)

· Factory Orders – November (10:00 AM ET)

Wednesday, January 8

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· ADP Employment Change Report – December (8:15 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Meeting Minutes – December (2 PM ET)

· Consumer Credit – November (3 PM ET)

Thursday, January 9

· Challenger Job Cuts Report – December (7:30 AM ET)

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, January 10

· Employment Report – December (8:30 AM ET)

· University of Michigan Consumer Sentiment Index (Prelim.) – January (10:00 AM ET)

International

Monday, January 6

· Japan: Jibun Bank Services PMI – December

· China: Caixin Services PMI – December

· Eurozone: HCOB Services PMI – December

· UK: S&P Global Services PMI – December

· Germany: Inflation Rate (Prelim) - December

Tuesday, January 7

· Eurozone: Inflation Rate (Flash) - December

Wednesday, January 8

· Japan: Consumer Confidence – December

· Germany: Factory Orders – November

· Eurozone: Consumer Confidence, Economic Sentiment – December

· Eurozone: Producer Price Index - November

Thursday, January 9

· Eurozone: Retail Sales - November

While we have a modicum of earnings reports out next week, the learnings from those results will help set the tone for when the December-quarter earnings season really begins on January 15. We will be interested in comments from Jefferies (JEF) about its investment banking backlog, deal pipeline, and what it sees ahead for 2025. The same goes for KB Home (KBH), obviously switching from learnings on investment banking transactions to single-family housing demand. Breaking down KB’s comments on margins, we’ll be interested in what it says about the use of value-added products like those furnished by Builders FirstSource BLDR.

Comments from airline companies in early December pointed to a vibrant holiday travel season, which was a nice positive for our shares of Mastercard MA and American Express AXP. With the Easter holiday landing in Q2 in 2025 vs. late March last year, we’ll be interested in Delta’s Q1 2025 travel guidance. And between comments from Cal-Maine Foods (CALM), Albertsons (ACI), and MSC Industrial (MSCI), we’ll be parsing what they say about inflation, pricing, and margins.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, January 6

· Open: Apogee Enterprises (APOG), Lindsay Corp. (LNN)

· Close: Cal-Maine Foods (CALM)

Wednesday, January 8

· Open: Albertsons (ACI), Helen of Troy (HELE), MSC Industrial (MSCI)

· Close: Jefferies (JEF)

Thursday, January 9

· Open: Constellation Brands (STZ), Walgreens Boots Alliance (WBA)

· Close: KB Home (KBH), PriceSmart (PSMT), WD-40 (WDFC)

Friday, January 10

· Open: Delta Air Lines (DAL).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.