Weekly Roundup: Moving Ahead of Powell at Jackson Hole

Here's our plan for five Portfolio holdings, and why we’ll focus on the August Flash PMI Report next week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market, as measured by the S&P 500, continued to move higher this week, leaving it up almost 4% as we conclude the first half of the September quarter. As we’ll discuss below in "Catching Up on the Pro Portfolio This Week," the Pro Portfolio gained ground as well and remains nicely in the green quarter to date.

The week brought multiple confirmation points for the Portfolio, including upbeat investor conference presentations from Qualcomm QCOM and Universal Display OLED. Quarterly results from Foxconn, Cisco CSCO and Lumentum LITE, as well as CoreWeave’s CRWV capital spending plans for 2H 2025, brought another layer of support for multiple holdings as well.

As we move into the second half of the quarter, we have Federal Reserve Chair Powell’s Jackson Hole keynote address on Friday, August 22, and the Flash August PMI report from S&P Global on Thursday, August 21. That report will be the first hard look at the U.S. manufacturing and services economy in August, and it will set the stage for the GDP inputs that are ISM’s August Manufacturing and Services PMI reports.

As such, the color it will provide on the overall speed of the economy, inflation pressures and job creation may help refine comments made by the Fed chair the following day. If S&P’s report shows inflation pressures unchanged compared to July or escalating further, barring a collapse in August Flash PMI job creation, we could see Powell’s tone skew more hawkish. Again, that’s if he opts to make any comments about monetary policy during his Friday keynote.

Because we won’t know what Powell will share until he says it, we expect the market will hang on Powell’s words during the address. While his comments could provide some fresh indications of what may happen later this year for monetary policy, it’s important to realize Powell may not tip the market off.

Our thinking continues to be that, coming off the increases we saw in the July Core CPI print, the July PPI report and the 0.4% sequential increase in July Import Prices, the Fed is going to want to see more data as it contemplates its next move with interest rates. Gaming it out, the central bank will want to see if those July increases were potential one-offs or the start of something more pronounced. At the same time, the Fed will also want to see if those July gains translate into higher prices as companies look to protect their margins and bottom-line prospects.

Exiting the week, the CME FedWatch Tool still shows the market expecting two 25-basis point rate cuts this year. While several Fed officials and potential ones have voiced their view for multiple rate cuts this year, Atlanta Fed President Raphael Bostic on Wednesday (August 13) reiterated that he continues to see one interest-rate cut as appropriate in 2025 if the labor market remains solid. Note the date — that was before the hotter-than-expected July PPI report on Thursday.

Depending on how the incoming data breaks, the market mindset that sees a more than 90% chance for a 25-basis point rate cut in September could have some re-thinking to do. On July 15, the market’s expectation for a 25-basis point rate cut stood at 54.5%, and we have numerous data streams to go before the Fed concludes its September policy meeting on Wednesday, September 17.

We will continue to follow the data and, based on market conditions and investor mindset, adjust the Portfolio as needed.

As we break for the weekend, on Saturday, you’ll have another batch of Portfolio signals and ripped-from-the-headlines data points to peruse. Sunday brings some lighter fare as well as a new book recommendation, one we’re already consuming.

And with that, we’ll wish you a wonderful weekend. See you back here early Monday morning.

Catching Up on the Portfolio This Week

The Pro Portfolio moved higher this week, propelled by shares of Qualcomm, United Rentals URI, Universal Display and Amazon AMZN. Those gains were held in check by the retreat in shares of Axon AXON, Dutch Bros BROS, Palantir PLTR and Waste Management WM, but as we discuss below, we see that there is a potential opportunity to scoop up more shares.

On Tuesday, we added to the Portfolio’s position in American Express AXP shares at $303.15. That was the only major move we made during the week, and following that trade, the Portfolio’s cash position was around 13.0% of its overall assets. We did downgrade the shares of Vulcan Materials VMC to a Two rating near $285 following the cumulative run of more than from around the $225 level in early April. We will continue to evaluate incoming data as it relates to our VMC price target and rating, but should we see VMC shares continue to chug higher, prudent action may be called for.

On Friday, following the findings of the July Retail Sales report, we bumped up our TJX TJX price target to $140 from $137. Based on what we hear from the company about its 2H 2025 outlook, we may have to revisit our target price yet again. That same July Retail Sales report also brought some hefty support for the Portfolio’s position in Amazon and Costco’s COST positions.

As we get ready for next week, we have five holdings that are on our shopping list: Axon, Dutch Bros, ServiceNow NOW, Waste Management and SuRo Capital SSSS. With SuRo, as the market digests the IPO lockup expiration for CoreWeave CRWV shares, we may pick up a few more shares as SuRo continues to monetize its investment portfolio. With shares of Dutch Bros, they are nearing the 200-day moving average, which could lead us to pick up some shares before too long.

Following the sharp move lower in NOW shares, we like the unfolding trend in their MACD, and that has us closely watching the shares. With Axon, we would look to see a similar pattern emerge like the one we see with NOW shares before making our next move. Ditto for Waste Management shares and their current $0.83 per share per quarter dividend. With Palantir shares, while we see support near $150, we also see a gap in the chart that would close if the shares reached $155 to $160. At such levels, the risk-to-reward tradeoff skews very favorably against our $190 target.

Now, let’s turn and catch up on what Wall Street had to say this week about the Portfolio’s holdings. As you can see below, it was rather modest, and as we move into the back half of August, odds are the volume of comments will remain modest until we’re back from the Labor Day holiday weekend. Nevertheless, we’ll continue to share what we spot.

Mizuho boosted its Nvidia target to $205 from $192, while Piper Sandler upped its target to $225 from $180

Argus upped its price target for United Rentals to $935 from $735 and sees the company benefiting from lower interest rates and on-shoring activities spurring customer projects.

This Week's Portfolio Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, August 11: Here's the Key Inflation Question Facing the Fed

Tuesday, August 12: Market Is Ignoring a Key From CPI, But We’re Not

Wednesday, August 13: Stocks & Markets Podcast: Crypto with David Namdar of CEA Industries

Thursday, August 14: Surprise July PPI Print Likely to Change Rate Cut Projection

Friday, August 15: Breaking Down July Retail Sales and Prepping for Jackson Hole

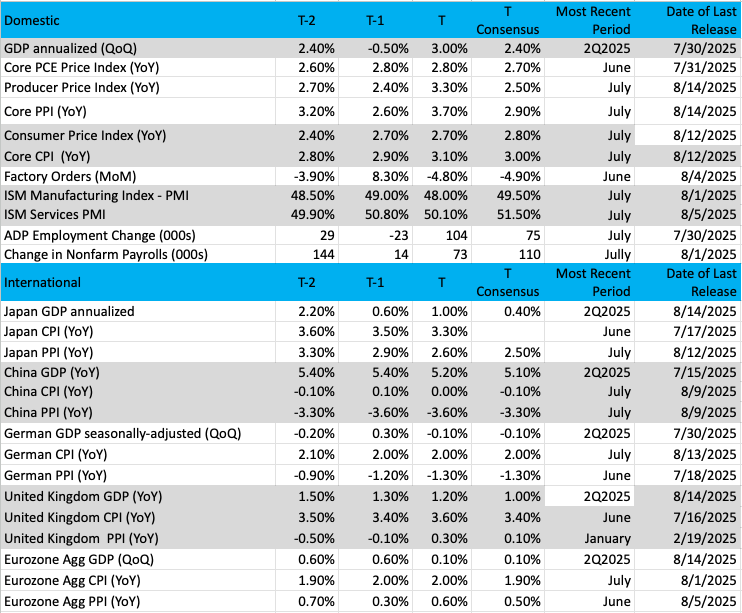

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

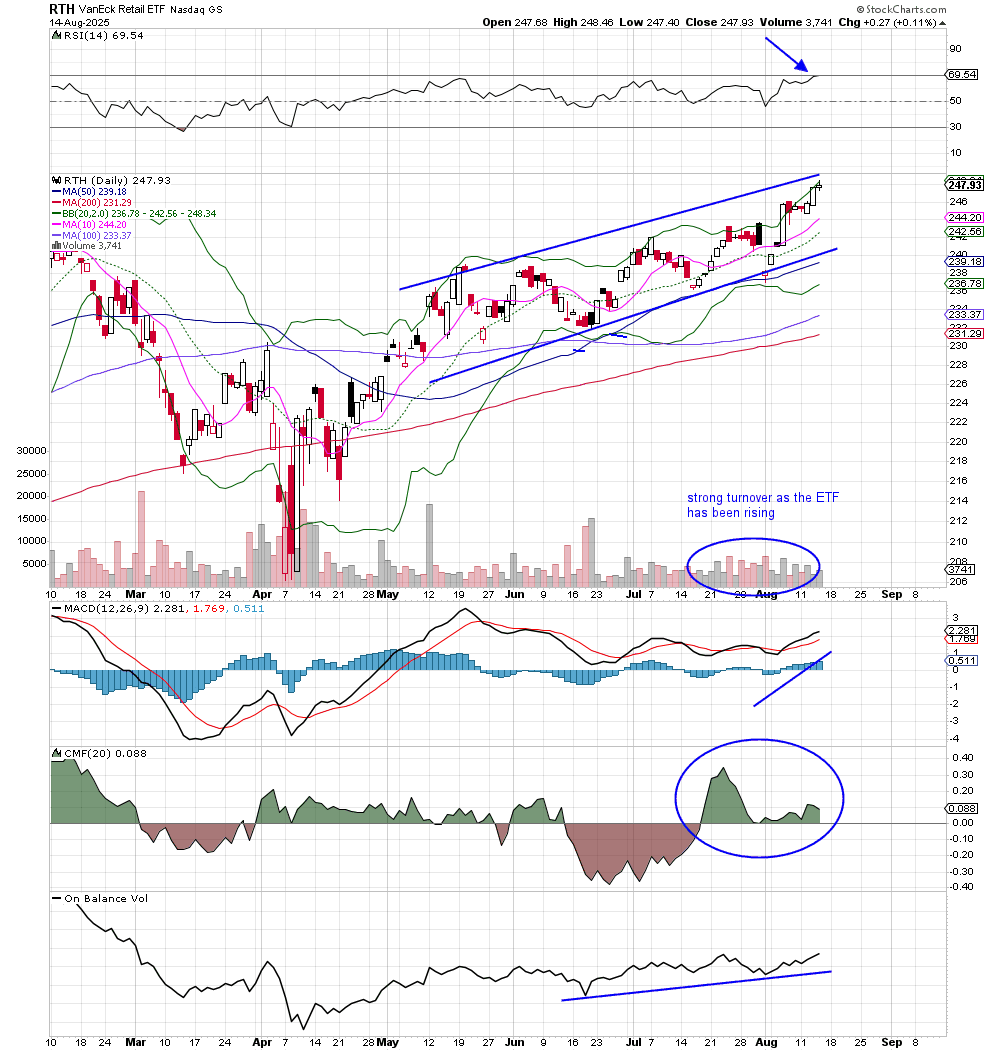

Chart of the Week: VanEck Retail ETF (RTH)

It is going to be a big week coming up for retail stocks.

A surge of earnings reports will hit the tape for names like Walmart WMT, Target TGT, Home Depot HD and other boutique-style companies. It is an important time for retail as not only are these companies trying to get inventory out the door, but they are also preparing for the coming holiday period. Many companies are hoping to continue their momentum through the end of the year with good inventory management, competitive pricing and better margins. A strong holiday season could really make your retail year profitable.

It is not always that easy, though — the "road to riches" is filled with land mines, but if a retail firm plans thoughtfully and responsibly, there is some chance of success. The biggest names in retail, of course, include digital shopping giant Amazon, a staple in TheStreet Pro portfolio. We have held this stock for years and have reaped the benefits of its growth and size, along with diversification in different businesses. The company has a huge influence on the retail ETFs like the VanEck Retail ETF, or the RTH. Amazon has a big weighting, as does Walmart and Costco (also a member of our Portfolio).

With so much at stake in the coming week, let’s look at the chart of RTH to see what is brewing. The ETF is in a solid uptrend, with higher highs and higher lows. That is our textbook definition. Relative strength is right at 70, which signals overbought, but that is simply a condition and not a signal. Money flow is positive but not as strong as it was in July, MACD is on a buy signal, as On Balance volume is improving.

With the RTH hitting new all-time highs this week and pressing forward, there could be a "sell on the news" effect next week, but I suspect, as we have seen over the past few months, any dip is likely to be bought.

Other charts we shared with you this week were:

Monday, August 11: S&P 500 - S&P 500 Raises the Bar and Bulls Respond

Monday, August 11: Axon Enterprise - Beat-and-Raise Holding Rewards Our Faith

Tuesday, August 12: Builders FirstSource BLDR - Closer Look at This Former Holding After Bullish Turn

Thursday, August 14: Bank of America Is Starting to Perk Up

Thursday, August 14: ServiceNow - ServiceNow Rally Could Be Imminent Despite Price Action Concern

The Week Ahead

Given our opening comments in this week’s Roundup about the August Flash PMI report next week and what we could hear from Fed Chair Powell, we’ll spare you a rehash here and head straight to a closer look at the economic data coming at us next week:

U.S.

Monday, August 18

- NAHB Housing Market Index – August (10:00 AM ET)

Tuesday, August 19

- Housing Starts & Building Permits – July (8:30 AM ET)

Wednesday, August 20

- MBA Mortgage Applications Index – Weekly (7:00 AM ET)· EIA Crude Oil

- Inventories – Weekly (10:30 AM ET)· FOMC Meeting Minutes (2 PM ET)

Thursday, August 21

- Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

- Jackson Hole Economic Policy Symposium

- Existing Home Sales – July (10:00 AM ET)

- Leading Indicators – July (10:00 AM ET)

- EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, August 22

- Jackson Hole Economic Policy Symposium – Powell Keynote TBD

International

Wednesday, August 20

- Japan: Machinery Orders – June

- Japan: Exports – July

- Eurozone: Inflation Rate (Final) - July

Thursday, August 21

- Japan: S&P Global Flash Manufacturing & Services PMI – August

- Eurozone: HCOB Flash Manufacturing & Services PMI - August

- U.K.: S&P Global Flash Manufacturing & Services PMI - August

- Eurozone: Flash Consumer Confidence - August

Friday, August 22

- Japan: Inflation Rate – July

- U.K.: Retail Sales - July

We see the expected shift we’ve been waiting for come next week as quarterly results from retailers take center stage. Setting up those July quarter reports, Friday’s July Retail Sales report revealed that retail-only sales rose 3.5% during the July quarter. That, as well as other July quarter line items contained in the report, will provide nice yardsticks by which to measure results from Walmart, Home Depot, Target, Ross Stores ROST, and many others, including our own TJX Companies.

With quick service restaurants like Cava CAVA and Sweetgreen SG serving up softer outlooks than market expectations anticipated, we could see retailers like Target do the same. As that swath of retailers report, we’ll be looking for confirmation of bifurcated consumer spending as well as watching margin expectations for the all-important, holiday spending-filled second half of the year. We suspect tariffs are likely to have an impact on those comments.

Alongside the July Housing Starts report next week, we’ll also be interested in what James Hardie JHX and Toll Brothers TOL have to say about that market in the balance of the year.

Exiting next week, we could see some modest movement in consensus S&P 500 EPS expectations, given Walmart accounts for about 1.37% of the basket and Home Depot another 0.7%. However, the next company that will have a pronounced impact on 2H 2025 EPS expectations for the S&P 500 is Nvidia, which will report after the market close on Wednesday, August 27.

Here's a closer look at the earnings reports coming at us next week:

Monday, August 18

- Close: Palo Alto Networks (PANW)

Tuesday, August 19

- Open: Home Depot (HD)

- Close: James Hardie (JHX), La-Z-Boy (LZB), Toll Brothers (TOL)

Wednesday, August 20

- Open: Analog Devices (ADI), Baidu (BIDU), Dycom (DY), Estee Lauder (EL), Lowe’s (LOW), Target (TGT), TJX Companies (TJX)

- Close: Bath & Body Works (BBWI), Guess? (GES), Williams-Sonoma (WSM)

Thursday, August 21

- Open: Canadian Solar (CSIQ), Walmart (WMT)

- Close: Ross Stores (ROST), Workday (WDAY)

Friday, August 22

- Open: BJ’s Wholesale (BJ), Buckle (BKE).

Portfolio Investor Resource Guide

- Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

- Investing Terminology: 16 Key Terms Club Members Should Know

- 10-Ks: Want to Know About a Stock? Read the Company's Reports

- 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

- Income Statement: Our Cheat Sheet to Understanding This Financial Document

- Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

- Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

- Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.