Weekly Roundup: Marvell and These 5 Holdings Propel Portfolio Higher

Here's how things played out and how we'll be watching the market’s technicals ahead of next week’s Fed meeting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market rebound that began on November 21 continued this week, leaving the S&P 500 up more than 2.5% quarter to date. Positive comments about the holiday shopping weekend helped continue the market’s upward move from last week, while Amazon’s (AMZN) AWS re:Invent 2025 and Marvell’s (MRVL) quarterly results spurred the market and the Pro Portfolio higher.

November job losses and a quicker pace of job cuts in the month reported by ADP and the Challenger Job Cuts report gave more legs to the market’s rise as expectations grew for a Fed rate cut next week. Friday’s September core PCE Price Index reading opened the door for the Fed to deliver on that expectation.

While the RSI levels for the S&P 500 and the Nasdaq Composite exiting the week are well below levels that would signal an overbought condition, the market rebound has the S&P 500’s P/E valuation back at roughly 25.4x expected 2025 EPS. That’s close to bumping up against the 25.6x multiple the S&P 500 peaked at in late October. That tells us expectations are running high, and in the past, when that’s been the case, it doesn’t take much to spook the market.

Before we get to the Fed’s policy decision on Wednesday, we’ll be keeping a very close watch on oscillator levels for the market as well as overbought conditions for the Pro Portfolio’s holdings. If conditions warrant, we may opt to take some chips off the table ahead of the outcome of Wednesday’s Fed meeting. In that decision, we’ll be closely following not only Fed Chair Powell’s comments about further potential rate cuts, but also the language he uses.

We’ll match that up against the Fed’s updated set of economic projections (SEP). The consensus among economists is that the central bank will deliver between two and three 25-basis-point rate cuts next year. If the Fed’s updated SEP continues to show just one 25-basis point rate cut, and Powell’s message is more hawkish than expected, that could deliver a setback for the market.

As we discuss below, there are several investor conferences next week, and attention will be on management comments about the current quarter and, to the extent they are shared, initial ones about 2026 EPS prospects. Currently, consensus expectations call for EPS growth to accelerate to more than 14% next year, up from the penciled-in 11.4% figure tallied by FactSet. Here too, if indications are that a 14%-ish figure is a bit aggressive, it could lead the market to give up some recent gains as investors reset expectations.

Those scenarios explain why we’ll be watching the market’s technicals early next week. To the extent they signal the market moves well into an overbought condition, the more likely some prudent register ringing would be the smart move.

Now, let’s see what the next few trading days bring and position the Portfolio accordingly.

Enjoy your weekend, Saturday’s signals alert, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

We kicked things off this week with our November Monthly Roundup, complete with a blow-by-blow look at all the Pro Portfolio’s holdings. Fast forward to the end of the week, and while the S&P 500 moved higher and the Nasdaq Composite rose at a brisker pace, the Pro Portfolio outpaced both of those market barometers.

Fueling that outperformance were shares of Marvell (MRVL) and their double-digit post-earnings pop. We also benefited from significant moves in Palantir (PLTR) , Qualcomm (QCOM) , ServiceNow (NOW) , Morgan Stanley (MS) , and Meta (META) . Other gainers included Axon Enterprise (AXON) , American Express (AXP) , Nvidia (NVDA) , SuRo Capital (SSSS) , and Bank of America (BAC) .

Offsetting those gains were net moves lower this week in shares of Arista Networks (ANET) , United Rentals (URI) , Welltower (WELL) , and Waste Management (WM) .

We made no trades in the Pro Portfolio this week, and closed the week out with 25 active positions plus the eight that comprise our EPS Diplomats exposure. We discussed how we are well aware of the cumulative moves of late in Morgan Stanley and Bank of America, and that should one or both move past a 4.5% position size, you should expect some prudent portfolio management and very profitable register ringing.

Even though we made no trades this week, the Portfolio’s cash position improved as we collected dividends from TJX Companies (TJX) and SuRo Capital. The next few weeks should bring in more dividend payments to the Portfolio, and we'll be listening for a few potential special dividend announcements before we close out 2025.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday – Morgan Stanley raised its Nvidia (NVDA) price target to $250 from $235 following channel checks in Asia and the U.S. Amazon (AMZN) saw a target increase at Oppenheimer to $305 from $290, while Guggenheim took its Google (GOOGL) target go to $375 from $330. JPMorgan increased its Waste Management target to $265 from $255, calling it a “top defensive growth long idea.”

Bullpen resident Home Depot (HD) saw a price target cut to $350 from $370 over at Stifel as it sees a “weaker underlying category not fully captured by expectations.”

Tuesday – Loop Capital nudged its Apple (AAPL) target to $325 from $315.

Wednesday – Jefferies raised its Marvell price target to $120 from $80, Craig-Hallum took its target to $141 from $111, and BofA reset its MRVL target at $105, up from the prior $88. Evercore ISI upped its MRVL target to $156 from $122 while Roth Capital moved its target to $135 from $105. RBC raised its Dutch Bros (BROS) target to $80 from $75, and BofA took its Amazon target to $303 from $272.

Thursday - Mizuho reiterated an Outperform rating and $815 price target on Meta Platforms, saying it sees a "significant rally ahead" for the shares. Mizuho also increased its price target for Dutch Bros shares to $80 from $70.

DA Davidson reiterated its $650 target on Microsoft (MSFT) , saying that the company offers the “best AI exposure.” As we discussed with you the same day, given our positions in MSFT, GOOGL, AMZN, META, and SSSS shares, we have diversified AI model exposure.

Also on Thursday, UBS lifted its price target on Welltower shares to $232 from $203, and Baird boosted its TJX target to $165 from $160.

Friday – CLSA boosted its Apple price target to $330 from $265, Truist lifted its Google target to $350 from $320, and Pivotal Research took its GOOGL target to $400 from $350, citing “continued momentum in the core business.” Citi resumed coverage on Marvell with a Buy rating.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Portfolio videos. If you happened to miss one or more of them, here are some helpful links:

Monday, December 1: Upcoming Reports Tied to Key Nvidia Levels

Tuesday, December 2: Responding to OpenAI's Google 'Code Red'

Wednesday, December 3: Stocks & Markets Podcast: Fighting Cancer With GT Biopharma CEO

Thursday, December 4: Today It’s Meta, But This Is Bound to Be a Big Topic in January

Friday, December 5: Our Questions About the Netflix-Warner Bros Discovery Deal

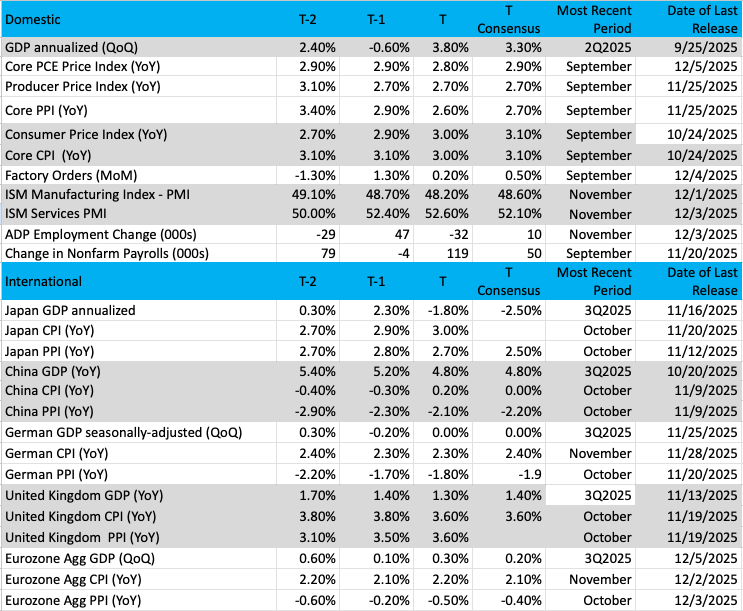

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

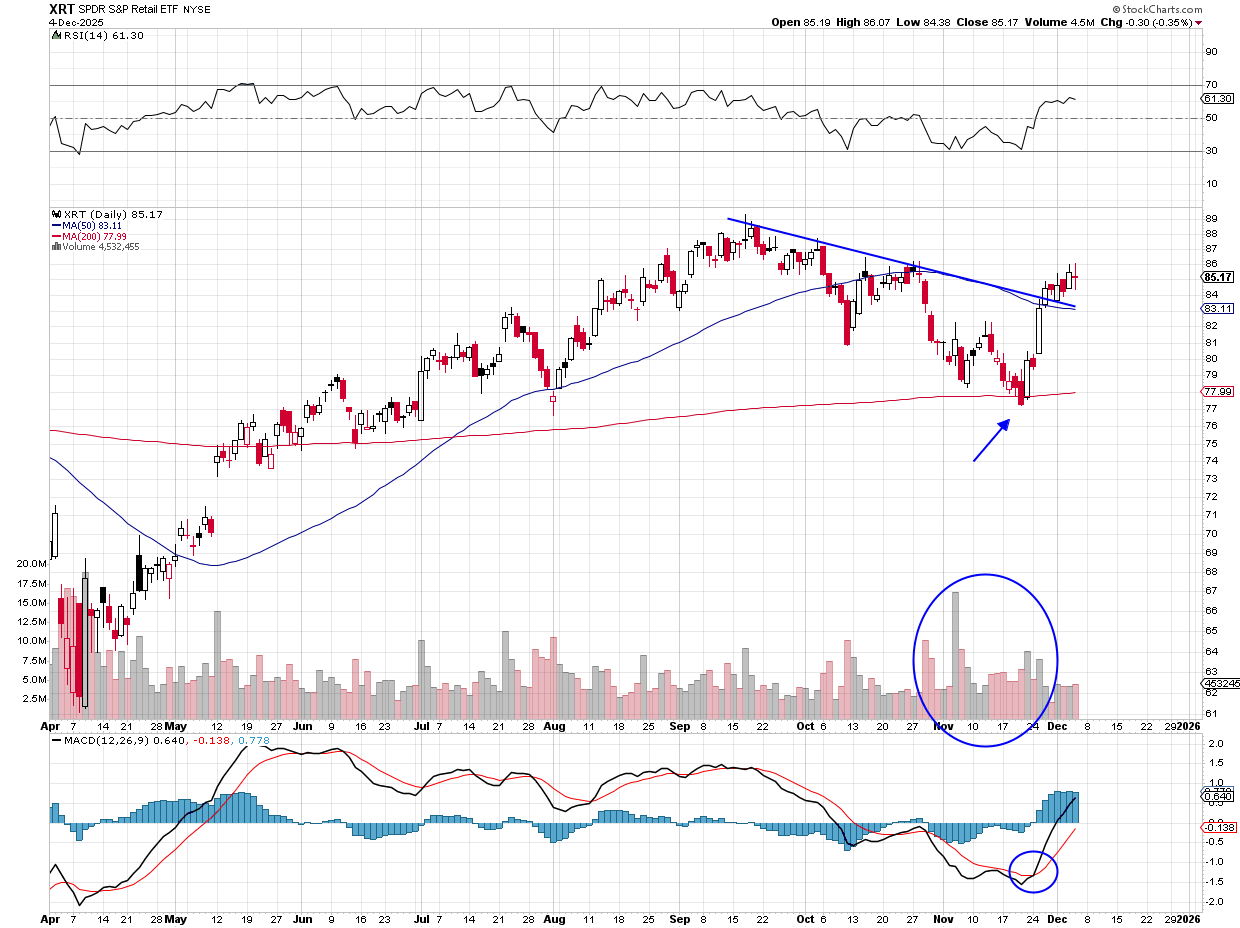

Chart of the Week: The SPDR S&P Retail ETF

Retail names are starting to warm up, and it is not just Amazon (AMZN) , Walmart (WMT) , and Costco (COST) . The latter, of course, is a holding in TheStreet Pro Portfolio and has been a terrible performer of late, but Amazon (also a holding) and Walmart seem to have gained some traction.

The worries are always out there about the consumer. Are they downshifting, buying fewer items, not paying up for higher prices? The eternal question, "Is the consumer failing to buy," is always on our minds, but if this most recent earnings season is any indication, then channeling Mark Twain, "the death of the consumer has been greatly exaggerated."

If we look across the retail landscape at different companies, we see the same stories/themes: robust consumer buying at any price, shopping big at discount stores, and heavy buying for the holiday season. Recent earnings from Victoria’s Secret (VSCO) , Urban Outfitters (URBN) , and Macy’s (M) tell this tale, but also Walmart, which has been seeing traffic online and throughout its stores. These are just a few examples and explain why the (XRT) has shown good relative strength of late.

The XRT is the SPDR S&P Retail ETF, and while it is only close to an all-time high, there is optimism that that level ($89) could be exceeded rather soon. A bounce off the 200-day moving average last month when it appeared the ETF was down and out is impressive, with strong volume as well. Last week saw the XRT piercing through the 50-day moving average, and it still resides above there, with strong volume trends across the board.

Moving average convergence divergence (MACD) is on a buy signal, and the relative strength index (RSI) is not quite overbought yet, so there is room to go higher. With only 5% away from the all-time highs, the XRT looks ready for a continued run to those levels.

Other charts we shared with you this week were:

Monday, December 1: S&P 500 - Bulls Take Control of the Trend

Tuesday, December 2: Progressive Corp. (PGR) - Making 'Progress' With a New Holding

Tuesday, December 2: Marvell (MRVL) - Watch Out, Marvell Could Make a Sudden Move

Wednesday, December 3: Seagate Technology (STX) - This 'Diplomat' Has a Bullish Look

Thursday, December 4: United Rentals (URI) - United Rentals Finds Support After Nasty Downturn

The Week Ahead

The coming week will bring additional November economic data points, including the latest NFIB Small Business Optimism Index and the October Jolts report, but the focal point will be the Fed’s policy decision. In Friday’s video, we recapped how the data we received this week boosted expectations for a 25-basis point rate cut.

In the same discussion, we also shared why, given that expectation, the greater focus for us is what Fed Chair Powell and the updated set of economic projections telegraph for rate cuts in the first half of 2026. The last time the Fed updated those projections back in September, it saw just one 25-basis point cut in the cards for 2026. Since then, we’ve seen greater signs of weakness in data reflecting the employment market from ADP and the Challenger Job Cuts report.

We could see the Fed Chair leave some flexibility in his comments as we collectively wait for the November Employment Report on December 16 and the November CPI report on December 18. Those reports and others received between now and then will have the potential to reshape, potentially in a meaningful way, rolling GDP forecast models. As we fade into the weekend, the Atlanta Fed’s GDPNow Model pegs current-quarter GDP at 3.5%, while the New York Fed’s Nowcast model is nearly half that at 1.7%.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, December 8

· Consumer Inflation Expectations Index – November (11 AM ET)

Tuesday, December 9

· NFIB Small Business Index – November (6:00 AM ET)

· Unit Labor Cost & Productivity – Q3 2025 (8:30 AM ET)

· JOLTS Job Openings & Quits – October (10:00 AM ET)

Wednesday, December 10

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Employment Cost Index – Q3 2025 (8:30 AM ET)

· Wholesale Inventories – October (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Policy Decision and updated Economic Projections (2 PM ET)

Thursday, December 11

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Producer Price Index – November (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

International

Monday, December 8

· Japan: Q3 2025 GDP

· Japan: Eco Watchers Survey - November

· China: Imports/Exports - November

Tuesday, December 9

· Germany: Imports/Exports - October

Wednesday, December 10

· China: Inflation Rate - November

Friday, December 12

· Japan: Industrial Production – October

· Germany: Inflation Rate – November

· UK: GDP, Manufacturing Production – October

Next week brings quarterly results from Costco (COST) , which, following the company’s November sales report this week, looks to top the market consensus of $67.0 billion in total revenue. We’ll look for the continued influence of the company's 2024 membership price hike on its high-margin membership fee revenue stream, as well as an update on its growing warehouse footprint. We could also see the topic of a special dividend this year emerge on the company’s earnings call, and as we discussed on Friday, such an announcement isn’t out of the realm of possibility.

Sticking with the Portfolio’s holdings, Arista Networks (ANET) is presenting at the Raymond James TMT and Consumer Conference on Dec. 9. The following day, Bank of America (BAC) will present at the Goldman Sachs Financial Services Conference. On Dec. 11, at the Barclays Global Technology Conference, Axon (AXON) , Microsoft (MSFT) , and Arista are on the docket.

Next week also brings quarterly results from homebuilder Toll Brothers (TOL) , and while we’ll be interested in its backlog and delivery expectations, our real focus will be on the use of incentives and Toll’s margins. Quarterly results from Ciena (CIEN) and Broadcom (AVGO) are also on tap, and we’ll be mining those reports and conference calls for the latest on AI chip demand, smartphone volumes, and networking demand.

Here's a closer look at the earnings reports coming at us next week:

Monday, December 8

· Close: Toll Brothers (TOL).

Tuesday, December 9

· Open: AutoZone (AZO), Campbell Soup (CPB), Ollie’s Bargain Outlet (OLLI), SailPoint (SAIL),

· Close: Dave & Buster’s (PLAY), GameStop (GME).

Wednesday, December 10

· Open: Chewy (CHWY),

· Close: Synopsys (SNPS), Vail Resorts (MTN).

Thursday, December 11

· Open: Ciena (CIEN),

· Close: Broadcom (AVGO), Costco (COST), Lululemon (LULU), Netskope (NTSK).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

· Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.