Weekly Roundup: Markets Take a Breath Ahead of Earnings Bump and Trump at Davos

During the week, we exited one profitable position, added to three holdings, and lifted another’s price target.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

After starting January off with a bang, the S&P 500 and Nasdaq Composite drifted lower this week. However, despite the modest setback, the S&P 500 still closed the week less than 0.5% off its recent record high. A quick look at the charts for those two market indexes shows they are neither overbought nor anywhere close to being oversold. The biggest “winner” this week when tracking market indicators was the CBOE Volatility Index (VIX), which rose more than 6%, putting it back above 15.

There were several factors that led to those moves this week, including questions about potential credit card caps, Venezuela, Greenland, and Iran, while there were raised eyebrows over the Department of Justice probe surrounding Fed Chair Jerome Powell.

Checks in the positive column included Taiwan Semiconductor (TSM) calling AI a megatrend, which was very constructive for multiple Pro Portfolio holdings. The U.S. and Taiwan inked a $250 billion trade deal that includes investing $250 billion in U.S. industries such as semiconductors, artificial intelligence applications, and energy. Gas prices continue to tick lower, and expectations are for higher tax refunds this year due to changes enacted in President Trump’s “big, beautiful bill.”

One of the more interesting developments late in the week was President Trump pushing for an emergency wholesale electricity auction with technology companies to fund new power plants. TBD if this will happen, but if it does, it would be a boon for our shares of Eaton (ETN) . Still, we’ll want to understand how it would impact Big Tech capital spending plans.

Next week, the volume of corporate earnings results jumps higher, but, as we discuss below in The Week Ahead, no Pro Portfolio names are scheduled to report. Still, how the market reacts to the corporate earnings we do get will be important to gauge the market’s mindset. Heading into the weekend, the Fear & Greed Index is flashing “Greed,” but again neither the S&P 500 nor the Nasdaq Composite is overbought or oversold. If anything, their respective RSI readings near 58 and 53-54 are not too far off the middle ground.

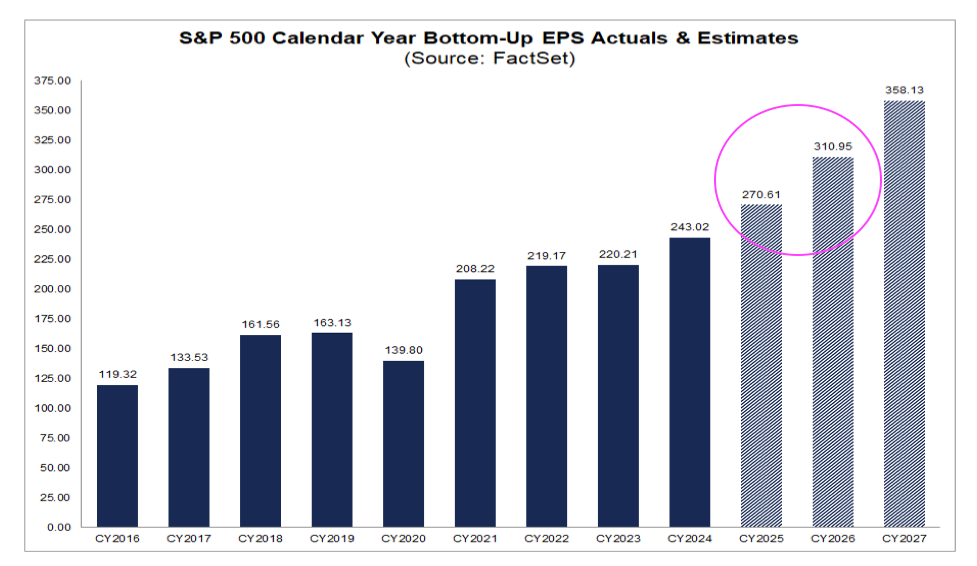

Our view remains that the aggregate forward guidance coming in the next few weeks and how it stacks up against consensus EPS growth expectations for 2026 will be a sizable factor in the market’s next sustained move. Based on the average peak multiple for the S&P 500 over the 2015-2025 period (excluding 2020 due to the pandemic) of 23.6x, if the market sees a path to the S&P 500 delivering EPS near $311 this year, we can see a path to 7350 for the S&P 500.

Based on where the market index closed this week, that suggests upside of around 5.5%. Nice, especially after the S&P 500’s collected move over the 2022-2025 period, but to outperform, we’ll need to focus on companies with superior EPS growth prospects backed by multi-year tail winds. From time to time, we may need to cull from the Portfolio’s herd, like we did this week with Qualcomm (QCOM) .

When we return on Tuesday (remember, U.S. equity markets are closed on Monday for the Martin Luther King Jr. holiday), we’ll have an updated set of consensus earnings and related metrics for the Portfolio. In the same Alert, we’ll share a list of those holdings that have published their upcoming reporting dates.

Enjoy your weekend, Saturday’s Signals, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

Like the S&P 500 and Nasdaq Composite, the Pro Portfolio slipped a bit lower compared this week, but we remain firmly in the black January to date. We can credit that performance to the double-digit gains in Axon Enterprise (AXON) , Costco (COST) , and United Rentals (URI) , as well as strong showings in Amazon (AMZN) , Eaton (ETN) , Alphabet (GOOGL) , Labcorp (LH) , Morgan Stanley (MS) , and Welltower (WELL) . Those gains have outweighed the biggest drag on the Portfolio, ServiceNow (NOW) (more on that below).

The basket of stocks that comprises our EPS Diplomats strategy, something I discussed in detail this week with Bob Lang, continued to be an outperformer for us compared to the S&P 500. SiTime Corp (SITM) had a strong finish to the week, while Kinross Gold (KGC) remains the strongest performer of the bunch with its near 20% gain so far this year.

We made several changes to the Portfolio this week. Late Tuesday, we downgraded Qualcomm (QCOM) to a Four rating and started the process of working our way out of the position Wednesday morning. We used those proceeds to pick up more shares of Broadcom (AVGO) and the First Trust Nasdaq Cybersecurity ETF (CIBR) . Following quarterly results and guidance from Taiwan Semiconductor (TSM) that reaffirmed our reasons for making the moves we did with Qualcomm, we closed out the balance of the position on Thursday.

Friday, we used some of those proceeds to pick up some deeply oversold shares of ServiceNow. In that note, explained what we will be watching leading up to the company’s earnings report and guidance later this month. The same day, we reiterated our $65 target for Bank of America (BAC) but noted why the shares could be rangebound near-term. We did, however, increase our price target for Morgan Stanley (MS) to $205 from $185, and discussed what could lead us to take that target even higher in the months ahead.

Exiting the week, the Portfolio’s cash levels stand at ~8.5% of its assets, which gives us flexibility as earnings season heats up, potentially bringing some opportunities with it. In terms of our shopping list, after scooping up additional NOW shares, we are still interested in owning more shares of Welltower and Broadcom, but we’re also eyeing other things as well.

Two things we did not discuss during the week were SuRo Capital’s (SSSS) Q4 2025 investment portfolio update and a small nip-and-tuck acquisition announced by Dutch Bros. (BROS) . Let’s tackle both here:

SuRo booked gains of ~$6.6 million during the quarter primarily by exiting some additional shares of CoreWeave (CRWV) and Forge Global (FRGE). At the end of 2025, SuRo still had roughly 68% of its CoreWeave investment. SuRo also said that in January it invested $5 million with an option for another $15 million in AI infrastructure company TensorWave. What we did not hear from SuRo was a rough net asset value (NAV) per share assessment, but we should get that figure when the company reports its quarterly results the week of March 9. We will also be interested to see what is said about SuRo’s next dividend payment, given those realized gains during Q4 2025.

Turning to Dutch Bros, it announced a deal to acquire Clutch Coffee and its 20-store drive-thru-only coffee shops across the Carolinas. We see this as a nice move that builds on Dutch’s efforts to expand its footprint at a brisk pace. No word yet when Dutch will report its December-quarter results, but we’ll tune into comments from Starbucks (SBUX) when it reports on Jan. 28.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday – RBC boosted its American Express (AXP) target to $425 from $390. Citi upgraded Palantir (PLTR) shares to Buy, taking its target to $235 from $210, following CIO survey findings that Palantir’s use cases are accelerating in the enterprise. Following Goldman’s new Buy rating on ServiceNow with a $205 target, Citi opened up an “upside 30-day catalyst watch” on the shares. Citi’s rating and target for NOW shares is Buy and $250.60.

Tuesday – BofA upped its Alphabet target to $370 from $335, while Goldman lifted its to $375 from $330. Citi lifted its target for United Rentals to $1,090 from $950.

Wednesday – RBC initiated coverage on Marvell (MRVL) shares with an Outperform and a $105 target, but also shared its view that the company could be an M&A target down the line. RBC also initiated coverage of Nvidia (NVDA) with an Outperform rating and a fresh $240 target. Baird boosted its price target for Labcorp shares to $313 from $307. TD Cowen nudged its Amazon target to $315 from $300 following the results of its Q4 2025 advertiser survey.

Thursday – Citi picked up coverage on Broadcom shares with a buy rating and a $480 target. Wells Fargo upped its AVGO rating to Overweight from Equal Weight as it sees gross margin concerns being “overdone.” Raymond James trimmed its Amazon target to $260 from $275, but at the same time shared that it sees Amazon Web Services growth estimates as conservative.

Friday – HSBC upgraded Eaton shares to “Buy, “ citing “above-market growth prospects and lifted its target to $400 from $390. RBC and Bank of America increased their respective targets for Morgan Stanley shares to $207 and $220 from $185 and $210. Jefferies lifted its Nvidia target to $275 from $250, but the firm's top pick in the group is Broadcom. Citi trimmed its Waste Management (WM) target to $263 from $270, but that still offers more than 19% upside, which explains why they stuck with their Buy rating.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, January 12: After Trump Noise We're Expecting More Volatility Ahead

Tuesday, January 13: Stocks & Markets Podcast: S&P Indicators, Fed Moves, and Portfolio Strategy With Bob Lang

Wednesday, January 14: An Intriguing Area of Interest for the Bullpen... Maybe the Portfolio

Thursday, January 15: Stocks & Markets Podcast: Why Portfolio Construction Matters With Louis Llanes

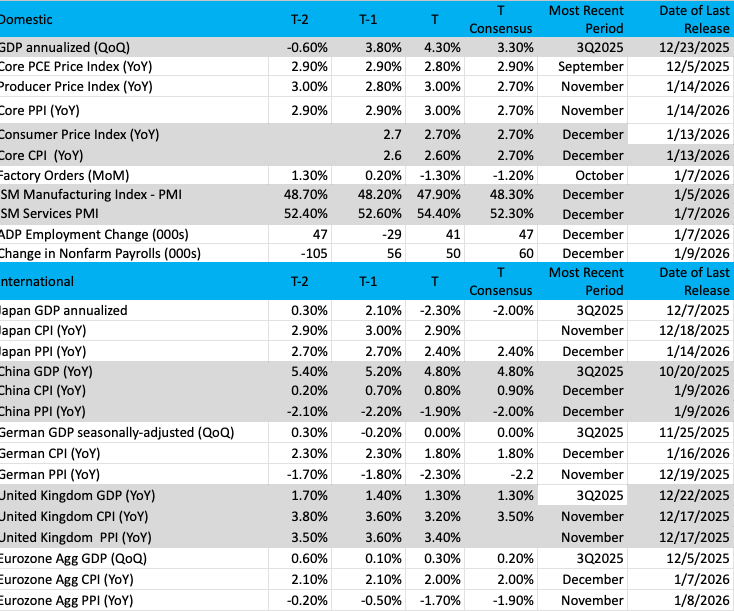

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

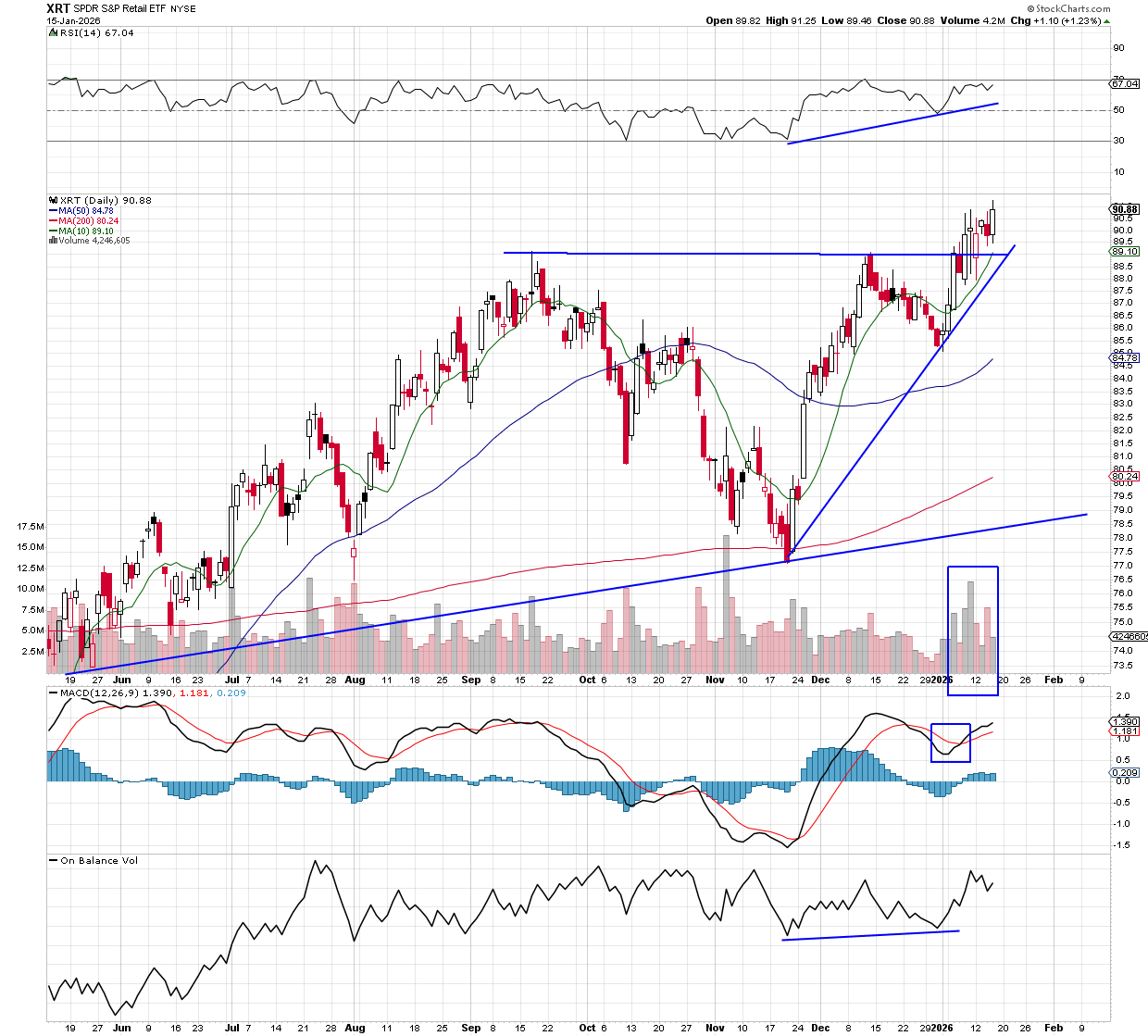

Chart of the Week: State Street SPDR S&P Retail ETF (XRT)

As we embark on another big earnings season, we consider what charts are looking best and make assumptions about a company’s future. We also understand the big money moves in well before the news breaks — that's always evident when we see large flows during times that don’t really make sense.

What do we mean by that? Well, basically, we are taught to "buy low and sell high" if we want to move our portfolios upward. That makes total sense, but there are times when you have to consider "buying high and selling higher," which takes you out on the risk curve a bit. Buying a stock after a sharp drop to oversold is considered a low-risk entry point, while buying a stock at a higher price has the risk of sellers taking profits.

But when it comes to big money investors, they often see opportunity at every marker on a stock price, or in this case, an ETF. Take (XRT) , for instance, the SPDR S&P Retail ETF, which just recently slammed through resistance for a new all-time closing high. The XRT includes all of the big retail names such as Walmart (WMT) , Amazon (AMZN) , Target (TGT) , Home Depot (HD) , and others.

The ETF was quite volatile in 2025, as we see from the chart, below, rising sharply into the fall after a sizable dip, but then rallying off the 200-day moving average in November. Since Thanksgiving, the XRT is up a whopping 18% and looking stronger than ever.

Notice the surge through the double top at the $89 level, stiff resistance from the old high created in September, and matched in early December. That first try to break the highs was rejected, but only with a modest 4% retreat, unlike the massive drop following the September high.

There is improvement in the indicators, the MACD (moving average convergence divergence) is on a strong buy signal, on-balance volume indicator is bullish, and the RSI (relative strength index) is nearly overbought. The price chart is extremely bullish as well, with higher highs and higher lows printed.

The surge by the XRT in 2026 (price and volume) is notable, especially with earnings season here. Do these stocks have more left in the tank? We think they do, as we look for the XRT to run soon toward $100, another 10% higher.

Other charts we shared with you this week were:

Monday, January 12: S&P 500 - New Target After Yet Another Milestone

Monday, January 12: United Rentals (URI) - Investors Excited About This Industrial Holding

Tuesday, January 13: Bank of America (BAC) - Keep a Close Eye on Bank of America as Earnings Land

Wednesday, January 14: SiTime (SITM) - Time's Right for SiTime

Thursday, January 15: American Express (AXP) - A Dip in This Holding Is Another Buying Opportunity

The Week Ahead

With U.S. equity markets closed on Monday, we have another abbreviated trading week ahead of us. Across those four days, we’ll continue to get catch-up data for October and November, as well as some for December. Chief among those will be the October and November Personal Spending data and the corresponding PCE price index figure.

Data from the Cleveland Fed’s Inflation Nowcast model pegs October and November core PCE figures between 2.70%-2.76% compared to the official reading of 2.8% for September. With Fed rate-cut expectations now sitting at mid-2026, it would take a far more meaningful improvement in the core PCE data than that to dramatically pull those expectations in. Remember too that this weekend the Fed enters its pre-policy meeting blackout period ahead of its Jan. 28 policy decision.

What we see in the Construction Spending data may give us reason to revisit our United Rentals (URI) price target. Based on housing data for October and November, we’re not expecting a big surprise on the residential construction spending side of the ledger. As such, our focus will be on the non-residential side as we get ready for quarterly results from United Rentals on Jan. 29.

Not all of the data will be of the “catch-up" variety, though. In fact, one report could be rather timely. We’re talking about the January Flash PMI report from S&P Global. For those who have been with us for a while, you know the drill when it comes to this report, but for newer folks, it’s the first hard look at job creation and inflation during the month. Its findings on new orders will help set expectations for the current quarter. Even the Atlanta Fed’s GDP Now model still only reflects Q4 2025. So much for the “now” part of the model.

We will also continue to keep close tabs on developments in and around Washington and President Trump. The president will address the World Economic Forum on Wednesday at 8:30 ET as part of Davos 2026, but we could see much more activity from the White House. Given recent developments with Venezuela, Greenland, and Iran, as well as topics from housing affordability, credit card caps, and even China trade talks, next week will be one to watch on several fronts. Should we see geopolitical tensions rise further, we have multiple exposures to gold in the EPS Diplomats basket.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, January 20

ADP Employment Change Report (Weekly) – 8:15 AM ET

Wednesday, January 21

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Housing Starts & Building Permits – December (8:30 AM ET)

Construction Spending – September, October (10:00 AM ET)

Pending Home Sales – December (10:00 AM ET)

Thursday, January 22

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Personal Income & Spending – October, November (8:30 AM ET)

PCE Price Index – October, November (8:30 Am ET)

GDP (Revised) – Q3 2025 (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

EIA Crude Oil Inventories – Weekly (12:00 PM ET)

Friday, January 23

S&P Global - Flash Manufacturing & Services PMI – January (9:45 AM ET)

University of Michigan Consumer Sentiment Index (Final) – January (10:00 AM ET)

International

Monday, January 19

China: GDP – Q4 2025

China: Industrial Production, Retail Sales – December

Japan: Machine Orders – November

Eurozone: Inflation Rate – December

Tuesday, January 20

China: Foreign Direct Investment – December

Germany: Producer Price Index – December

Eurozone: ZEW Economic Sentiment Index - January

Wednesday, January 21

UK: Inflation Rate, Producer Price Index, Retail Price Index – December

Thursday, January 22

Japan: Imports/Exports – December

Eurozone: Consumer Confidence (Flash) - January

Friday, January 23

Japan: S&P Global Flash Manufacturing & Services PMI – January

Japan: Bank of Japan Interest Rate Decision

Eurozone: HCOB Flash Manufacturing & Services PMI – January

UK: S&P Global - Flash Manufacturing & Services PMI – January

Given our comments above, you may be relieved to know that we have no Pro Portfolio companies reporting next week. That will change in a big way the following week, however, but let’s not get ahead of ourselves. We will use next week’s reports to connect the dots back to our holdings and Bullpen residents. Those learnings will help us prepare and potentially position ourselves for their quarterly results and guidance.

As we called out in our ServiceNow (NOW) trade Alert on Friday, we will be listening intently for comments about AI adoption, usage, and spending. We will also be sizing up aggregate forward guidance relative to the expected ~15% EPS growth for the S&P 500 in 2026 compared to 2025.

We will also be watching for earnings pre-announcements and gauging the market’s reaction to earnings beats, in-line results, and shortfalls relative to consensus expectations. While neither the S&P 500 nor the Nasdaq Composite’s relative strength levels (RSIs) are near an overbought condition, Helene Meisler’s findings suggest we will want to tread carefully in the near term.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, January 20

Open: 3M (MMM), D.R. Horton (DHI), U.S. Bancorp (USB)

Close: Interactive Brokers (IBKR), Netflix (NFLX), United Airlines (UAL), Waste Connections (WCN)

Wednesday, January 21

Open: Charles Schwab (SCHW), Johnson & Johnson (JNJ)

Close: CACI International (CACI)

Thursday, January 22

Open: Abbott Labs (ABT), GE Aerospace (GE), McCormick (MKC), Mobileye (MBLY), Procter & Gamble (PG)

Close: Alaska Air (ALK), CSX (CSX), Intel (INTC), Intuitive Surgical (ISRG)

Friday, January 23

Open: Booz Allen Hamilton (BAH), Ericsson (ERIC).

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.