Weekly Roundup: Market Jumps on Tariff Ruling, But Braces for New Trade Moves

It was a nice end to a short week, but questions linger over how sustainable it is. Let's break it all down and get you ready for next week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It was another short, but eventful trading week, which began with China’s Lunar New Year and Spring Festival, saw U.S-Iran tensions escalate, brought the latest Fed meeting minutes, and more indications inflation is at best sticky, but more likely to tick higher in the coming months. However, it was Friday’s U.S. Supreme Court ruling striking down President Trump’s tariffs that led the market to rebound from last week’s selloff. Despite that gain, the S&P 500 is up only modestly year-to-date, while the tech-heavy Nasdaq Composite is down more than 1%.

Subsequent to the court’s ruling, we laid out potential ways Trump could proceed to rebuild his wall of tariffs. Soon after we shared those thoughts, the president announced, as many suspected he would, the use of different tools to work around the ruling. This included plans to impose a flat 10% levy on foreign goods in the coming days, and to order a raft of trade investigations that should allow him to enact more permanent tariffs. Friday afternoon, the Treasury Department said the new use of alternative legal authorities for tariffs “will result in virtually unchanged tariff revenue in 2026…"

While we saw tariff-sensitive stocks rise on Friday, including the Portfolio’s position in Amazon (AMZN) , our concern is that, given the president's remarks on Friday, there could be more to come on the tariff front. As we look to gauge that possibility over the weekend and early next week, we’ll also be closely following developments between the U.S. and Iran. Late Friday, Trump acknowledged he is weighing a limited strike on Iran.

Looking back over the shortened week, the biggest drop in all the major market indicators was for the Cboe Volatility Index (VIX), which fell more than 5% on Friday. That helps explain the market’s gain on Friday, but there are reasons to think that dip in the VIX could be short-lived. With that in mind, we’ll keep a close watch on that indicator as we start the final week of trading for February, and we’ll do the same for the S&P 500 relative to its 50-day moving average.

Enjoy your weekend, and Saturday’s Signals alert. We'll see you back here, bright and early on Monday with our updated Portfolio table.

Catching Up on the Portfolio This Week

The Pro Portfolio edged higher week over week as gains in multiple holdings, such as Apple (AAPL) , Amazon (AMZN) , and United Rentals (URI) , outweighed declines in Dutch Bros (BROS) , Eaton (ETN) , Costco (COST) , and a few others. The week-over-week decline in Eaton and Welltower (WELL) shares brings nice confirmation for our recent moves to lock in gains in both stocks when they were recently overbought.

As we explained during the week, while folks were impressed with Walmart’s (WMT) comps sales, those at Costco were even more compelling. As far as Dutch Bros goes, there were no developments this week that warrant the move lower, especially after the management reiterated its footprint and menu expansion plans. We’ll have more to say on this when we share an updated table of consensus EPS estimates and other metrics with you Monday morning.

In last week’s Weekly Roundup, we noted that our EPS Diplomats basket was up 13.1% since we reconstituted the basket back on January 2. The good news continues on that front, as that basket closed this week up just over 18% quarter to date. The week-over-week improvement can be traced to the double-digit moves in Lumentum (LITE) and Pan American Silver (PAAS) , as well as a high-single digit increase in Equinox Gold (EQX) .

The only trade we made this week was with Palantir (PLTR) , adding to our holdings following a trifecta of customer wins. As we explained in the Alert, two of the wins should lead to further gains for its commercial-facing business, while all three should help Palantir deliver another quarter of total contract value gains.

During the week, we did not receive any dividend distributions from our holdings, but next week we will get the latest quarterly dividend from United Rentals (URI) . Looking ahead to March, we see seven such quarterly payments on the horizon, all of which will be credited to our cash position. Closing out this week, that position tallies near 7.7% of the Portfolio’s assets, giving us room to maneuver.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during this shortened but electric week for the market:

Tuesday: CIBC increased its Waste Management (WM) target to $242 from $231 following a meeting with the management team.

Wednesday: Mizuho upgraded shares of Palantir to Outperform from Neutral and reiterated its $195 target. Citi increased its Welltower price target to $245 from $215. JPMorgan increased its Labcorp (LH) price target to $330 from $319.

Thursday: Tigress Financial reset its Alphabet (GOOGL) target at $415, up from $280, and reiterated its Strong Buy rating.

Friday: Citi reiterated its Buy rating and raised its price target on Microsoft (MSFT) shares to $635, citing Copilot momentum and strength in the company’s Azure cloud unit.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Pro Portfolio videos. If you happened to miss one or more of them, here are some helpful links:

Tuesday, February 17: Software's 'Unfair' Sell-Off With Schwab Network

Friday, February 20: Stock Market Reacts to Supreme Court's Tariff Decision

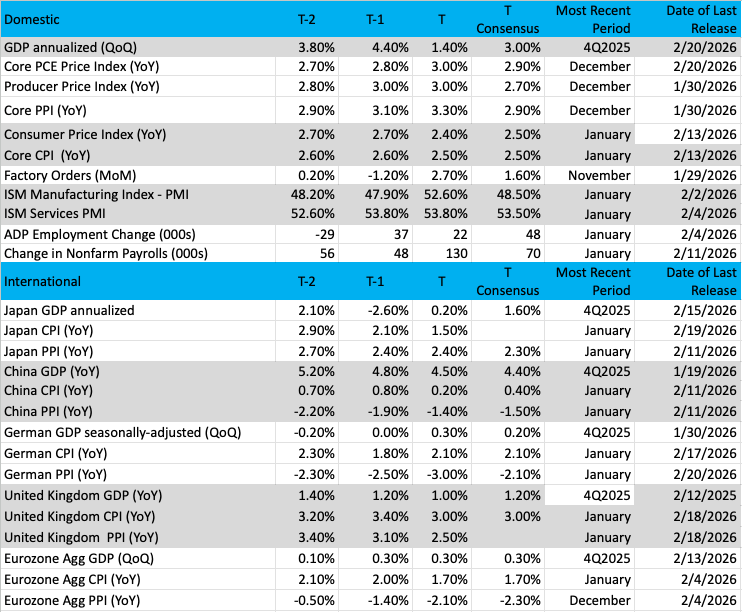

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

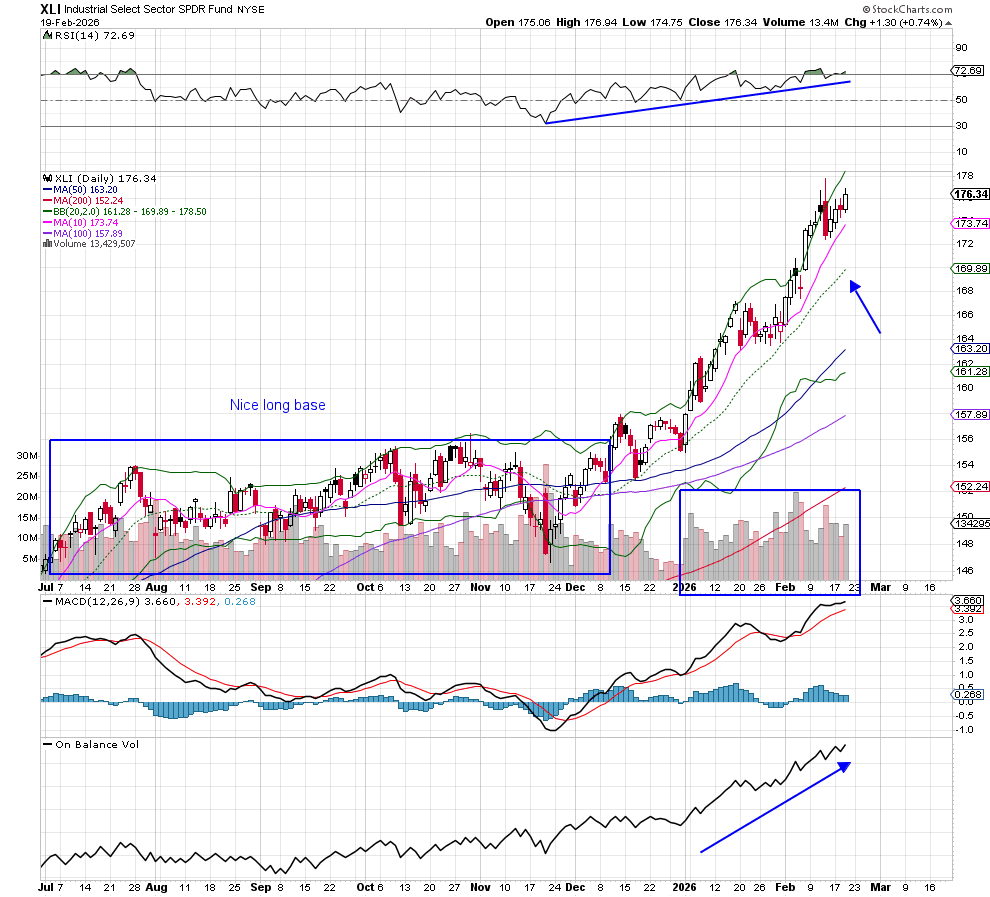

Chart of the Week: State Street Industrial Select Sector SPDR ETF

With the constant chatter of how Artificial Intelligence is going to reshape our lives and help us become smarter, it is a bit surprising to find that an old group of names has taken the leadership role in the markets. If you look at the performance of the Industrial Select Sector SPDR Fund (XLI) , you will notice the amazing strength since bottoming last summer.

The rally up from the November low is impressive, but if you go back a few months before the first bottom was made, then a long basing period ensued. That basing period is what we like to see, and the longer it lasts, the better-quality rally will follow. I would categorize the move from Thanksgiving to current levels as a high-quality rally.

Now, don’t get me wrong, the XLI is overbought and due for a pullback. It is deeply stretched away from the 20-day moving average (arrow), and when it does, there is either a pullback or a pause that occurs to let the moving average "catch up" to the price.

Indicators are all bullish, with the MACD confirmed, and balance volume at the bottom is very impressive and has been for months, with higher highs and higher lows. This indicator, when rising, tells us the best volume lands on the days when the ETF is higher.

What I find particularly strong is the higher level of volume during the first two months of 2026 (box). This tells us big money is coming after names in the XLI without regard to price, which only means one thing: the big money players believe higher prices are coming, and soon!

What names are in the XLI? Companies such as Caterpillar (CAT) , GE Aerospace (GE) , Boeing (BA) , Deere (DE) , RTX (RTX) , Eaton (ETN) , Uber (UBER) and Honeywell (HON) . Not your garden variety AI names, for sure! Some of these stocks have had extraordinary moves so far in 2026, and if they pull back a bit, you might consider adding this bullish ETF.

Other charts we shared with you this week were:

Tuesday, February 17: Nasdaq Composite - The Nasdaq Loses Its Edge

Tuesday, February 17: ServiceNow (NOW) - Is ServiceNow Finally Bottoming?

Wednesday, February 18: Alphabet (GOOGL) - Google's Recent Touch of This Spot May Be Important

Thursday, February 19: Bank of America (BAC) - It Could Be the Time to Buy the Dip in This Holding

The Week Ahead

Typically, the last week of the month is a relatively slow one when it comes to fresh economic data, but next week we’re getting some outstanding catch-up pieces. Both of those come on Friday and include the January Producer Price Index and Construction Spending data for November and December.

Ahead of those data points, we have Fed officials making the round, and while we’ll be tracking their comments, given what we saw in the inflation data and findings contained in the Flash February PMI report from S&P Global, there is little reason to think they will be calling for additional rate cuts in the near-term.

And with only a few inputs for the Atlanta Fed’s GDPNow model, which currently pegs Q1 2025 GDP at 3.1%, we’ll look to revisit that model and others like it once we close the first week of March. Those first few days of the final month of the current quarter will bring several key pieces of economic data, including ISM’s PMI reports and multiple looks at job creation in February. If they reaffirm the findings from S&P’s Flash February PMI data, we could see the Atlanta Fed’s GDPNow model poised for some downward revisions. But there is a difference between a slow-growing economy and a contracting one, especially if inflation continues to percolate.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, February 23

Chicago Fed National Activity Index – January (8:30 AM ET)

Tuesday, February 24

ADP Employment Change Report (Weekly)

S&P Case Schiller Home Price Index – December (9:00 AM ET)

Consumer Confidence – February (10:00 AM ET)

Wholesale Inventories – December (10:00 AM ET)

Wednesday, February 25

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, February 26

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

30-Year Mortgage Rate – Weekly (12 PM ET)

Friday, February 27

Producer Price Index – January (8:30 AM ET)

Construction Spending – November, December (10:00 AM ET)

International

Monday, February 23

Germany: Ifo Business Climate - February

Wednesday, February 25

Germany: GfK Consumer Confidence – March

Germany: GDP – Q4 2025

Eurozone: Inflation Rate (Final) - January

Thursday, February 26

Japan: Leading Economic Index (Final) – December

Eurozone: Economic Sentiment, Consumer Confidence - February

Friday, February 27

Japan: Industrial Production, Retail Sales, Housing Starts – January

Germany: Import Prices – January

Germany: Inflation Rate (Prelim) - February

We have three of our holdings reporting next week – Axon (AXON) , TJX (TJX) , and Nvidia (NVDA) and ahead of each of those reports, we’ll be sharing market expectations for both the reported quarter and forward guidance. We’ll also detail what we’ll be focusing on when we walk through their earnings releases and digest their earnings call comments. And as we barrel toward the end of the current earnings season, we’ll continue to connect the dots between comments from other companies and our holdings.

Next week also brings several investor conferences, which we’ll be mining for quarter-to-date comments, tying them back to the Portfolio’s positions and ones we may be contemplating:

Monday: Barclays Communications and Content Symposium (February 23-24), BMO Global Metals Mining & Critical Minerals Conference (February 23-24)

Tuesday: Oppenheimer Healthcare Life Sciences Conference (February 24-25), Bernstein Insights Tech Media Telecom Forum (February 24-26), Bank of America Global Agriculture and Materials Conference (February 24-25)

Wednesday: Susquehanna Technology Conference (February 25-26)

Of those conferences, given our thoughts about what it will take for software companies like ServiceNow (NOW) to rebound on a sustained basis, Susquehanna’s conference will be the one we focus more closely on. That will prep up for what a wider array of tech companies are likely to say at Morgan Stanley’s Technology, Media, & Telecom Conference the following week.

Here's a closer look at the earnings reports coming at us next week:

Monday, February 23

Open: Domino’s (DPZ), Freshpet (FRPT)

Close: Bed Bath & Beyond (BBBY), Ovinitiv (OVV), USA Rare Earth (USAR)

Tuesday, February 24

Open: American Tower (AMT), Armstrong World (AWI), Elanco Animal Health (ELAN), First Watch (FWRG), Henry Schein (HSIC), Home Depot (HD), Keurig Dr Pepper (KDP), Planet Fitness (PLNT),

Close: Axon (AXON), Cava (CAVA), First Solar (FSLR), HP (HPQ), Interparfums (IPAR), Realty Income (O), Tanger Factory (SKT), Trex (TREX)

Wednesday, February 25

Open: Bloomin’ Brands (BLMN), Clear Secure (YOU), Dine Brands (DIN), Lowe’s (LOW), Owens Corning (OC), Photronics (PLAB), TJX (TJX)

Close: BJ Restaurants (BJRI), California Water (CWT), GoodRx (GDRX), IMAX (IMAX), Joby Aviation (JOBY), Nvidia (NVDA), Pure Storage (PSTG), Salesforce (CRM), Snowflake (SNOW), Teladoc (TDOC), Veeco Instruments (VECO)

Thursday, February 26

Open: Cars.com (CARS), Celsius (CELH), Hertz Global (HTZ), Hormel Foods (HRL), Installed Building Products (IBP), JM Smucker (SJM), Nomad Foods (NOMZ), Papa John’s (PZZA), Shake Shack (SHAK), TopBuild (BLD)

Close: Ambarella (AMBA), American Healthcare REIT (AHR), Block (XYZ), CoreWeave (CRWV), Dell (DELL), Elastic (ESTC), Intuit (INTU), NetApp (NTAP), Sweetgreen (SG), Zscaler (ZS)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.