Weekly Roundup: Market and Portfolio Power Higher, But Volatility Lies Ahead

The stock market hitting new highs raises the standard for investors to be impressed this earnings season.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

After a bit of a setback last week, this week's stock market, as measured by the S&P 500 and the Nasdaq Composite, and the Pro Portfolio moved higher, adding to their year-to-date gains. On Thursday, the S&P 500 hit its ninth record close of the year at 6297.35 and went on to hit an intra-day high of 6315.61 before finishing the day at 6296.79. From a technical perspective, with the Nasdaq’s relative strength index (RSI) closing out the week above 72, it is once again in overbought territory, while the S&P 500 is once again flirting with that status with its RSI level just shy of 69.

In last week’s Weekly Roundup, we discussed why quarterly earnings would be the near-term driver of the market while we wait and see what happens on the trade front ahead of President Trump’s August 1 deal deadline. From the big banks, including our own Morgan Stanley MS and Bank of America BAC, to Taiwan Semiconductor TSM, ABB Ltd. ABB, Netflix NFLX, and even American Express AXP, the results this week were better than expected. In some cases, shares of those names moved higher, while others, including Netflix and American Express, declined.

With market expectations for 2025 S&P 500 EPS falling over the last few months, and the market bumping up against all-time highs, we continue to think guidance will be a key factor for stock prices as we move through the current earnings season. In the case of stocks that were on fire during the June quarter, beat-and-raise quarters will need to meaningfully surprise the market to the upside. We’re looking at you, Taiwan Semiconductor and Netflix. In other cases, like with American Express, a strong June-quarter beat that isn’t accompanied by raised guidance is likely to weigh on the shares despite the underlying favorable outlook.

As the pace of quarterly earnings picks up next week and even further the following one, we could see the market become volatile, especially if company guidance skews more conservatively as we’ve been thinking it could. While the Volatility Index (VIX) isn't exactly screaming complacency, its reading of 16.46 to close out the week skews more toward the market being complacent than not. We have ample cash on hand to make moves with existing positions should those opportunities arise. We’re also keeping an eye out for new ones.

We’ll also be following trade talk developments, and we suspect sparks could fly on that front the closer we get to August 1. That could contribute to greater market volatility, especially if countries look to use the media to drive those conversations. Fortunately, the economic data calendar next week is on the lighter side, but we will be very interested in what the Flash July PMI data has to say. Next week will also be quiet when it comes to the Fed as the central bank enters its pre-policy meeting quiet period.

Across all those items we’ll be watching, we’re pleased to present another round of Portfolio Signals to you Saturday. On Sunday, we'll have some more lighthearted fare, but, as you’ll see, the boys behind the Acquired podcast have a great interview with JPMorgan Chase’s JPM Jamie Dimon.

Have a wonderful weekend, and we’ll see you back here on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio moved higher this week, benefiting from strong week-to-week performances in shares of Palantir PLTR, SuRo Capital SSSS, Eaton ETN, Nvidia NVDA, and some others. Those gains more than compensated for the Friday decline in shares of American Express AXP, Labcorp LH, and Universal Display OLED.

We have more on Amex shares below, and as for Labcorp, we’ll be interested in quarterly results next week from competitor Quest Diagnostics DGX. Meanwhile, the next data point we are watching for OLED shares will be quarterly results next week from LG Display LPL, and what it says about organic light-emitting diode adoption.

After locking in some simply impressive gains on Nvidia and United Rentals URI last week, when we also bought more Axon Enterprise AXON, we made no Portfolio trades this week. We started off the week by increasing our NVDA price target to $200 from $185. Then, on Wednesday, we shared our take on the better-than-expected quarterly results from Bank of America BAC and Morgan Stanley MS as well as where we would be interesting in adding more shares.

For BAC, we would consider a rating revision from Two if the shares positively test support near the 50-day moving average, just below $45, but a much more compelling pick-up point would be near $42 to $43. As for MS, we’re keeping an eye on the $125 level, which offers a much more favorable risk-to-reward entry point as well as firm technical support.

The following day, we connected the dots between Taiwan Semiconductor’s TSM beat-and-raise June quarter to multiple Pro Portfolio holdings. In that note, we noted the reporting dates for other companies, like LG Display LPL and Qorvo QRVO, that we’ll be watching ahead of quarterly earnings from Qualcomm QCOM, Apple AAPL, and Universal Display.

We then walked through the June Retail Sales report, tying back its findings to our positions in American Express, Costco COST, and TJX Companies TJX. That report also showcased why we called out COST shares during the Tuesday “Good Buy or Good Bye” segment on Yahoo! Finance’s Market Domination.

Thursday afternoon, we discussed Asset-Lite businesses, and why we like companies with IP licensing business models, including Pro Portfolio holdings Qualcomm and Universal Display.

After reviewing June-quarter results and guidance from American Express, which confirmed why we focus on its membership business model and net card fee revenue, we boosted our price target to $340 from $310. We also indicated that after trimming the position back near $327 earlier in the month, the subsequent pullback has us eyeing adding back some shares. In our Alert, we discussed potential levels at which we may do that.

On Friday, we also explained why June-quarter results from ABB Ltd. ABB and the findings in the June Associated Builders and Contractors’ Construction Backlog Indicator and Construction Confidence Index keep us bullish on Eaton, United Rentals, and Vulcan Materials VMC.

When we return on Monday, we’ll have an updated look at consensus EPS expectations for the Pro Portfolio’s holdings, their RSI levels and a few other things. Along with that, we’ll have a revised Portfolio shopping list.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, July 14: Earnings From These 3 Holdings Could Shape the Week

Tuesday, July 15: Bank Earnings Show Not All Banks Are the Same

Wednesday, July 16: Stocks & Markets Podcast: Inside Big Oil With Prairie Operating Co.’s Ed Kovalik

Thursday, July 17: Why We Are Bullish on Costco and Steering Clear of Target

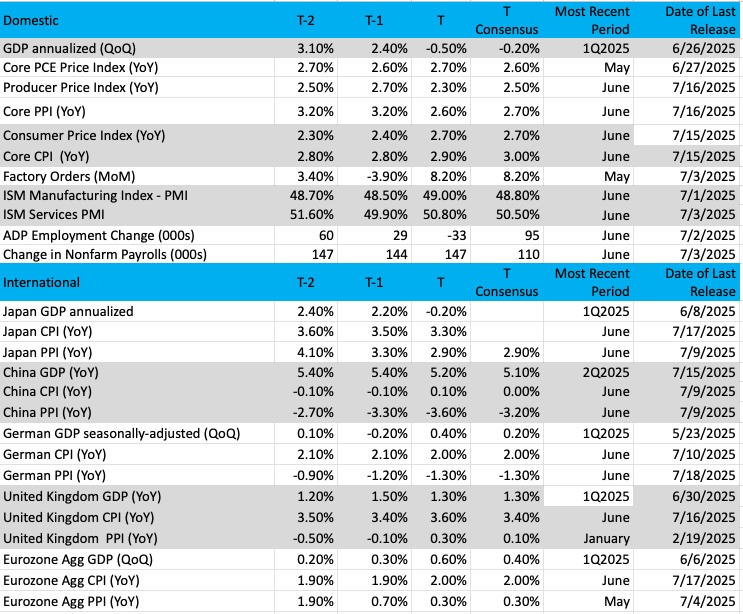

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

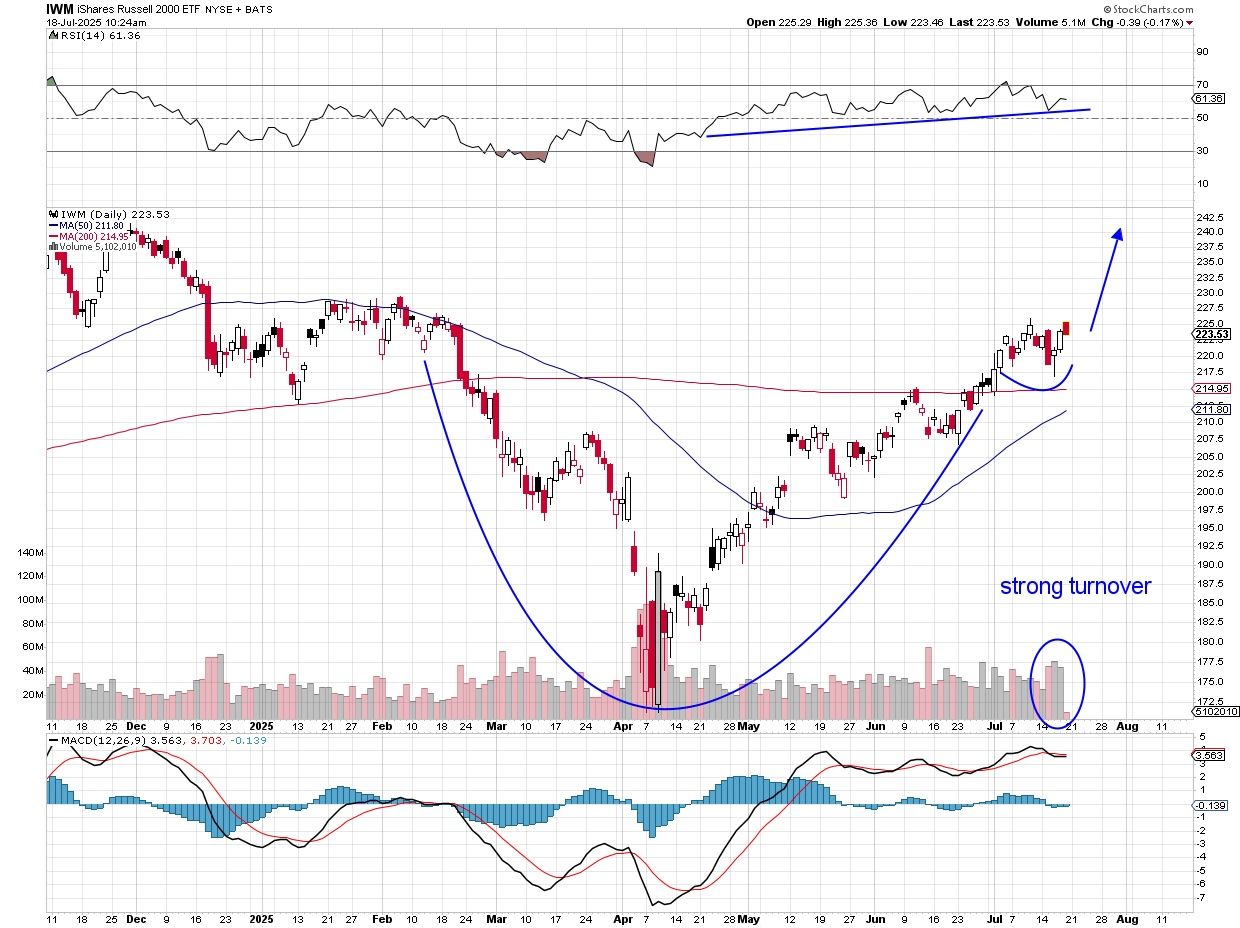

Chart of the Week: iShares Russell 2000 ETF (IWM)

Since the April lows, small-cap stocks have been quite large! They tend to move markets.

The Russell 2000 is a giant index that includes just about every sector in the markets. The iShares Russell 2000 ETF IWM is the one we follow to determine if there is interest or not by investors in small-caps. Now, we should remember that along the investment frontier, the IWM is considered far riskier than mid-cap or large-cap stocks.

By their very nature, with small capitalization and index weighting, these companies are not often the first look for fresh, new institutional money. However, most managers like to diversify in terms of size to have a balanced approach (large, medium and small).

For the Russell 2000, its success is very simple: The index thrives in a low or reducing interest-rate environment. When the cost of funds starts to fall, we look very closely at these small-cap stocks for investment purposes. Why is that so? Basically, small-cap companies are looking for financing at the lowest possible cost, so if market rates are low, it offers the opportunity to finance their businesses more cheaply. A high-rate environment makes it much more challenging to compete.

As for markets, there is no question that the small-caps often lead the market trends. When the IWM is strong, it leads to many more up sessions and brings the Nasdaq and S&P 500 along with it. The patterns we see over time show that small-caps can exert power over the markets when breadth expansion and volume are rising.

With respect to the chart, the IWM shows a bullish cup/handle pattern with the current price about to make a move above the top of the handle. That is extremely bullish, especially with the successful test of the recent lows on Wednesday.

The 50-day moving average is about to cross above the 200-day moving average for the first time since late March, which is also bullish. The IWM is just under 10% away from the all-time highs, which are now in its sights. As the IWM rolls, so rolls the rest of the market.

Other charts we shared with you this week were:

Monday, July 14: S&P 500 - Are Buyers Getting Fatigued?

Monday, July 14: Costco (COST) - For Costco, Which of These 2 Scenarios Will Play Out?

Tuesday, July 15: American Express (AXP) - A Close Look at American Express Ahead of This Week's Earnings

Wednesday, July 16: Utilities Select Sector SPDR Fund (XLU) - Utility Play Makes a Stunning Move

Thursday, July 17: Marvell (MRVL) - Is This Holding's Pullback a Gift to Investors?

The Week Ahead

The pace of quarterly earnings reports accelerates considerably next week, as does the number of S&P 500 constituents reporting their results. More than 200 companies reported this past week, of which 42 were S&P 500 constituents. Those figures jump to more than 600 and 112 next week, respectively, per data culled from Zacks. You’ll quickly realize that by the end of next week, only about a third of the S&P 500 will have reported, which means we have a ways to go until the current earnings season is over. As such, we will continue to parse quarterly results and updated outlooks, connecting the dots back to the Pro Portfolio and its holdings.

There is a modicum of fresh economic data out next week, which means we’re not likely to see any major movement in the rolling GDP forecasts for Q2 2025. Exiting this week, the Atlanta Fed’s GDPNow model is at 2.4%, while the New York Fed’s Nowcast model is at 1.7%. Interestingly enough, the New York Fed Nowcast model for the current quarter has the economy revving up to 2.4%. Between that trio of figures, it doesn’t telegraph meaningful warning signs for the economy, but as you know, we will follow the data.

We’ll have the opportunity to think more about that Q3 2025 Nowcast figure when we dig into S&P Global’s July Flash PMI data next week. Our interest will be on the findings for new orders, inflation pressures, and job creation. We’ll be comparing the trend line for those data points and what they mean for the economy and monetary policy.

Speaking of monetary policy, ahead of the Fed’s next policy meeting that runs July 29-30, we are entering into the FOMC's blackout dates from July 19-31. Given that timetable, we doubt Fed Chair Powell will say anything new when he delivers a speech at the Integrated Review of the Capital Framework for Large Banks Conference in Washington on the morning of Tuesday, July 22.

A quick check of the CME FedWatch Tools as we close out the week shows a 93.5% probability the Fed won’t deliver a rate cut exiting the July meeting, and just under a 58% probability for a 25-basis point rate cut when the September policy meeting concludes. Pulling back the lens a bit further, current probabilities suggest the market expects additional rate cuts of that magnitude following the Fed’s October and December policy meetings.

We have a lot of economic data to come before we get to September and October policy meetings. There is also the August 1 trade deal deadline for President Trump’s tariffs. Rather than follow the herd, we’ll follow the data and course correct as needed.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, July 21

· Leading Indicators – June (10:00 AM ET)

Wednesday, July 23

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Existing Home Sales – June (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, July 24

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Chicago Fed National Activity Index – June (8:30 AM ET)

· S&P Global Flash PMI – July (9:45 AM ET)

· New Home Sales – June (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, July 25

· Durable Orders – June (8:30 AM ET)

International

Wednesday, July 23

· Eurozone: Flash Consumer Confidence - July

Thursday, July 24

· Japan: Jibun Bank Flash PMI – July

· Eurozone: New Car Registrations – June

· Germany: GfK Consumer Confidence – August

· Eurozone: HCOB Flash PMI – July

· UK: S&P Global Flash PMI - July

· Eurozone: European Central Bank Interest Rate Decision

Friday, July 25

· UK: Retail Sales – June

· Eurozone: ECB Survey of Professional Forecasters

· Germany: Ifo Business Climate and Expectations – July

· Eurozone: ECB Consumer Inflation Expectations - June

As we discussed, there's a sharp ramp in the volume of quarterly earnings coming up next week. Waste Connections WCN, Lazard LAZ, Digital Realty Trust DLR, and Intel INTC are some of the ones we’ll be decoding for our positions in Waste Management WM, Morgan Stanley MS, Bank of America BAC, Nvidia NVDA, and Marvell MRVL.

As for the Pro Portfolio, Alphabet GOOGL, ServiceNow NOW, United Rentals URI, and Labcorp. LH report next week. They are all clustered toward the back half of next week, but that means we can mine what’s said by SAP SE SAP, Quest Diagnostics DGX, and others earlier in the week.

Here's a closer look at the earnings reports coming at us next week:

Monday, July 21

· Open: Domino’s Pizza (DPZ), Verizon (VZ)

· Close: Alexandria RE (ARE), NXP Semiconductor (NXPI)

Tuesday, July 22

· Open: Coca-Cola (KO), DR Horton (DHI), General Motors (GM), Lockheed Martin (LMT), MSCI (MSCI), Northrop Grumman (NOC), Paccar (PCAR), PulteGroup (PG), Quest Diagnostics (DGX), Sherwin-Williams (SHW)

· Close: SAP SE (SAP), Texas Instruments (TXN)

Wednesday, July 23

· Open: GE Verona (GEV), General Dynamics (GD), Hilton (HLT)

· Close: Alphabet (GOOGL), Chipotle (CMG), Crown Castle (CCI), CSX (CSX), IBM (IBM), Las Vegas Sands (LVS), ServiceNow (NOW), Tesla (TSLA), United Rentals (URI), Waste Connections (WCN)

Thursday, July 24

· Open: ADT (ADT), American Airlines (AAL), Comcast (CMCSA), Honeywell (HON), Keurig Dr Pepper (KDP), Labcorp (LH), Lazard (LAZ), Mobileye (MBLY), Union Pacific (UNP)

· Close: Digital Realty Trust (DLR), Intel (INTC)

Friday, July 25

· Open: AutoNation (AN), Booz Allen Hamilton (BAH), HCA (HCA).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.