Weekly Roundup: Making Moves as Uncertainty Rises in a Complacent Market

As we navigate the market with trades and adjustments, we’re watching S&P 500 EPS expectations as second-quarter earnings season kicks off.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The S&P 500 finished lower for the week as investors contended with another wave of Trump tariff uncertainty. It started on Monday when the president said that U.S. tariffs will return to April 2 levels on August 1 if there is no progress on trade deals with the U.S. Shortly thereafter we received word that wave of “take it or leave it” tariff letters were sent out as well as the White House indicating trade deals will be announced in the coming days.

With no trade deals being announced, Trump escalated tariff threats on Friday, saying that he may impose a 35% tariff on certain imports from Canada, and was considering a 15%-20% blanket tariff on most U.S. trading partners, up from the initial baseline of 10%. Combined with the new August 1 deadline, we continue to see this as the president aiming to regain the trade deal narrative. However, the supposed “method” behind Trump’s strategy is accompanied by business uncertainty.

Our concern has been that the effect of tariffs would lead companies to deliver more conservative guidance than expected when they report their June quarterly results. Supporting our view, this week semiconductor test company Aehr Test Systems AEHR said that it is seeing “timing-related delays in order placements due to tariff-related uncertainty…” That led the company to maintain its cautious approach and not reinstate specific guidance beyond what has already been communicated.

Helen of Troy HELE missed June-quarter expectations with the management team saying tariff-related impacts made up “approximately 8 percentage points of the 10.8% consolidated revenue decline.” Also, ConAgra CAG organic net sales fell during its May quarter, and the company now expects its organic sales to be down 1% to up 1% this year as it factors higher costs and U.S. tariffs into its outlook. Thursday night, Levi Strauss LEVI management said that for now, it will absorb what it can of the tariff cost. We take that to mean margin headwinds could blow even harder if Trump ups his baseline tariffs or the ante in some other way.

Given the timing of Trump’s latest round of potential tariff escalations this week against his new August 1 deadline, odds are there will be more company comments like those above in the coming weeks as the June-quarter earnings season unfolds. That likely outcome has us reiterating that we will remain cautious but open to opportunities should they present themselves.

While we assess tariff and trade developments, and connect the dots as the June-quarter earnings season plays out, we will also be following the evolution of H2 2025 EPS expectations for the S&P 500. In The Week Ahead section below, we walk through the latest consensus EPS expectations for the S&P 500. We will be closely monitoring this earnings season and its implications on those expectations for H2 2025, and what that may mean for the market. That includes how investors may view the market multiple, especially if it expands further due to further declines in S&P 500 EPS estimates due to tariff and margin pressures or other forces.

Rest assured, we will re-position the Pro Portfolio as necessary based on how those earnings prospects develop and what we learn as we connect the dots from June-quarter earnings season.

Catching Up on the Portfolio This Week

The Pro Portfolio followed the market’s move lower this week, but remains well in the green, up more than 6% on a year-to-date basis. Notable week-to-week gains in shares of United Rentals URI, Amazon AMZN, Nvidia NVDA, Palantir PLTR, Microsoft MSFT, and SuRo Capital SSSS were offset by larger declines in Axon Enterprise AXON, ServiceNow NOW, Bank of America BAC, and Labcorp LH.

It was a somewhat busy week for the Pro Portfolio. On Monday, we trimmed back our exposure to American Express AXP, locking in a nice double-digit gain. On Friday, we made a similar move with shares of Nvidia NVDA and United Rentals URI, boking gains of 113% and 234%, respectively. We used some of those proceeds to pick up additional shares of Costco COST on Thursday following its June revenue report. On Friday, we took advantage of a big misunderstanding on Axon to pick up more of those shares for the Pro Portfolio.

During the week, we also increased our price target on SuRo Capital shares to $9.25 from $8.75 following the company sharing a preliminary look at its investment portfolio. SuRo also announced it would resume paying dividends, starting soon with one of $0.25 per share. Management also indicated it plans to declare additional dividends throughout the year, confirming that part of our SSSS investment thesis.

Netting out the moves we made with the Portfolio this week, roughly 12.6% of its assets are in cash, which gives us a nice buffer for any return of market volatility. It also doubles as a nice source of firepower for us to be opportunistic should the right situations present themselves. We've discussed our interest in adding further to positions in Dutch Bros BROS and Waste Management WM. Other holdings on our shopping list include SuRo, TJX Cos. TJX, and Palantir. And if we see a continued pullback in Axon shares, we’d be open to adding even more to that position. The same goes for ServiceNow.

Now let’s see what Wall Street had to say about the Portfolio’s holdings this week:

JPMorgan nudged its Alphabet GOOGL price target to $200 from $195.

Piper Sandler raised its Amazon AMZN price target to $250 from $212, while JPMorgan took its target to $255 from $240.

Bank of America BAC shares were lifted to a target of $48 at JPMorgan from $43.50. Truist also reset its BAC target at $53, up a few bucks from $51, but Keefe Bruyette made the biggest move, taking its BAC target to $57 from $52.

HSBC downgraded shares of Labcorp LH to Hold, keeping its $260 target intact. Our target is $265.

Meta META saw a nice price target bump to $795 from $735 at JPMorgan. BofA also upped its target to $765 from $690.

BMO Capital upped its Microsoft MSFT target to $550 from $485 following growing comfort with Azure prospects. Piper Sandler made a bigger move, taking its MSFT target to $600 from $475.

Keefe Bruyette raised its rating on Morgan Stanley MS to Outperform and slapped a new $160 target on the shares.

Goldman Sachs initiated coverage on Nvidia NVDA shares with a fresh $185 price target and a Buy rating. It’s always nice to see Goldman match our price target for a Portfolio holding.

Citing greater confidence in its AI strategy, Wedbush raised its Palantir PLTR price target to $160 from $140. As you know, we recently took our PLTR target to $160.

Citi lifted its Qualcomm QCOM target to $170 from $145, and also took its Nvidia target to $190 from $180.

Barrington Research increased its SuRo Capital SSSS target to $10 from $9.

Daiwa initiated coverage on TJX Cos. TJX with an Outperform rating and a $133 target.

JPMorgan lifted its United Rentals URI target to $950 from $920 as it sees the company benefiting from accelerated depreciation found in Trump’s “big, beautiful bill.”

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns and Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, July 7: Why We Sold Off Some American Express Shares

Wednesday, July 9: Stocks & Markets Podcast: Small Caps & Your Portfolio With Thomas Browne

Thursday, July 10: How 2 Holdings Benefit From Major Acquisition News

Friday, July 11: How Can Market Withstand Latest Trump Tariff Turmoil?

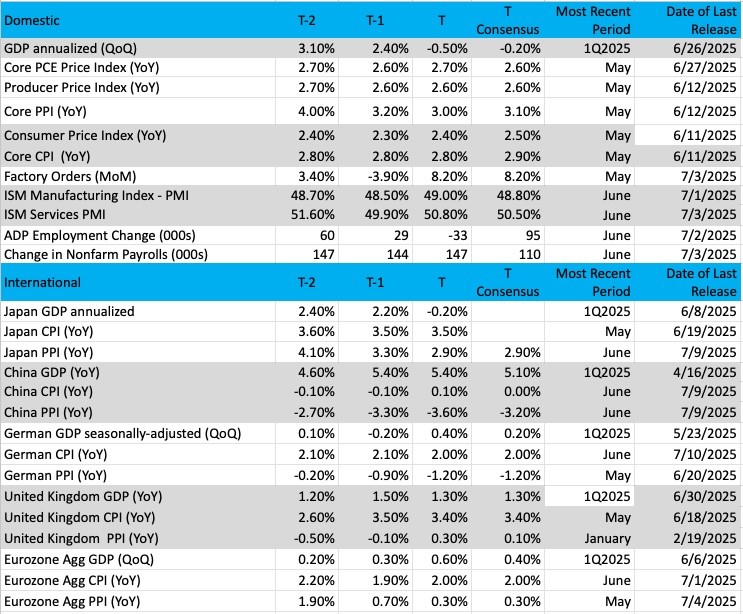

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

Chart of the Week: Financial Select Sector SPDR Fund (XLF)

It’s earnings season time, and the group that usually kicks this off is the banks/financials. There will a heavy dose of those names reporting, including JPMorgan Chase JPM, Wells Fargo WFC, and the Pro Portfolio’s own Bank of America BAC and Morgan Stanley MS. We are looking for strong numbers to carry these stocks, but the worry, of course, is how much good news may already be priced in.

The The Financial Select Sector SPDR Fund XLF has risen sharply since the lows set in April. In just three months, the ETF is up a staggering 25%, and some of the bigger components (named above) are up even more.

With a complacent stock market (low volatility index) and potential selling on the news it seems this group is priced for perfection. Can the banks/financials continue this bull rally that has seen the indexes rise 20% or more?

We think so, but in the short run, there could be bumps along the way. The XLF is sputtering here at all-time highs, which it just exceeded last week. We don’t believe this is a huge problem, though, and there could be some "backing and filling" here to take this group down even up to 5%. The uptrend would still be intact, so any heavy selling should be considered a buy-the-dip opportunity.

The indicators here have started to roll down, except for the MACD, which remains flat. The XLF appears to be building a flat base here, the last few days, which could last a bit longer (maybe a month to six weeks) before we see a breakout move. We see the prior base (shown in the chart) before the next move higher, which was about 6-7% from the base.

ADX (pane 3) is starting to move up, which does not tell us direction, rather that the ETF is on the move. Money flows have weakened over the past few weeks, likely because of some profit taking after a strong rally.

Other charts we shared with you this week were:

Monday, July 7: S&P 500 - The Russell Stars and the S&P Confirms Its Bullish Move

Monday, July 7: Labcorp (LH) - This Key Level Could Signal Labcorp's Move Higher

Tuesday, July 8: Dutch Bros (BROS) - Dutch Bros Makes a Pitstop as It Looks for a Charge

Wednesday, July 9: United Rentals (URI) - A Holding Breaks Out of a Flat Base

Thursday, July 10: Bank of America (BAC) - A Closer Look at Bank of America Ahead of Earnings

The Week Ahead

Following a very slow week for economic data and quarterly earnings, let’s reset the table for GDP and S&P 500 consensus EPS expectations as the pace for both picks back up next week.

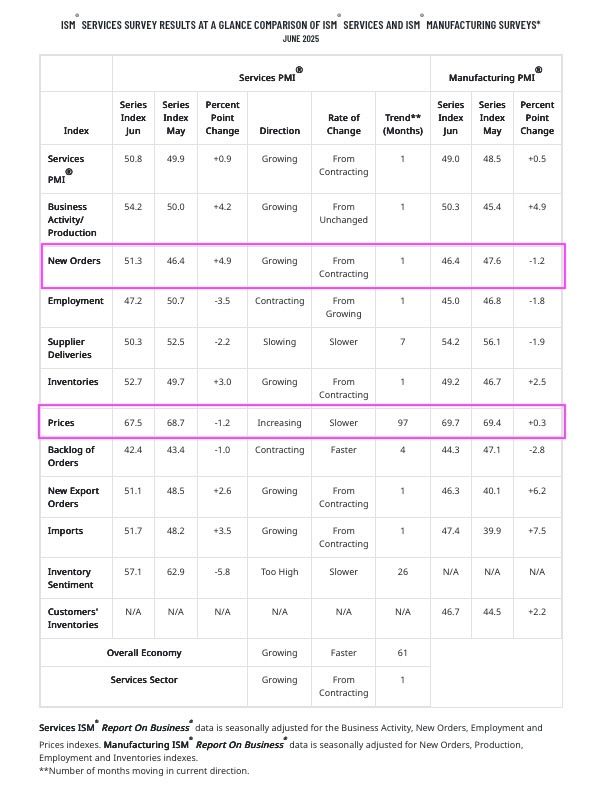

The latest reading for the Atlanta Fed’s GDPNow rolling forecast for GDP pegs Q2 2025 at 2.6%, while the New York Fed’s Nowcast model is at 1.6% for Q2 and has an initial forecast of 1.8% for the current quarter. Not quite heady levels of growth, but ones that point to a growing economy. Supporting the New York Fed’s 1.8% figure is the bounce back found in June ISM Service PMI new order data, which more than offsets the less severe slowdown in June for the manufacturing sector compared to May.

The three big pieces of economic data coming at us next week will be the June readings for the Consumer Price Index (CPI), the Producer Price Index (PPI) and Retail Sales. Given what we saw in the June ISM PMI Prices data, core CPI and PPI figures are expected to tick higher compared to May, with core PPI moving past 3% on a year-over-year basis. We’ll also be looking for what the next iteration of the Fed’s Beige Book has to say about the speed of the economy and inflation when it’s published next week.

Based on what we’ve seen, the driving force will be tied back to the impact of tariffs, and if the reported data matches what’s expected or is even higher, it will keep the Fed in a holding pattern. With Trump now focused on an August 1 deadline for trade deals and tariffs, the market will likely look through next week’s inflation reports, and to some extent, comments from Fed officials making the rounds.

What’s interesting about Trump’s August 1 deadline is that it quickly follows the Fed’s next policy meeting that concludes on July 30. We’ll be tracking tariff and trade developments, but unless we see meaningful progress on that front before the Fed concludes its policy meeting, we should expect to see Powell reiterate that the Fed is monitoring the impact of tariffs on inflation. Should Trump pull the trigger on the higher tariff rates he’s telegraphed, barring a sharp downturn in the jobs market, odds are we’ll see expectations for a September rate cut get pushed out.

Without question, we will have to follow the economic data as well as trade and tariff developments very closely in the coming weeks.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, July 15

· Consumer Price Index – June (8:30 AM ET)

· Empire State Manufacturing Index – July (8:30 AM ET)

Wednesday, July 16

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Producer Price Index – June (8:30 AM ET)

· Industrial Production & Capacity Utilization – June (9:15 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Beige Book (2 PM ET)

Thursday, July 17

· Retail Sales – June (8:30 AM ET)

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Import/Export Prices – June (8:30 AM ET)

· Philly Fed Index – July (8:30 AM ET)

· NAHB Housing Market Index - July (10:00 AM ET)

· Business Inventories – May (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, July 18

· Housing Starts & Building Permits – June (8:30 AM ET)

· University of Michigan Consumer Sentiment (Prelim.) – July (10:00 AM ET)

International

Monday, July 14

· Japan: Machinery Orders, Industrial Production - May

Tuesday, July 15

· China: Industrial Production, Retail Sales, Fixed Asset Investment, New Yuan Loans - June

· Eurozone: Industrial Production – May

· Eurozone: ZEW Economic Sentiment Index - July

Wednesday, July 16

· UK: Inflation Rate - June

Thursday, July 17

· Japan: Imports/Exports – June

· Eurozone: Inflation Rate - June

Friday, July 18

· Japan: Inflation Rate – June

· Germany: Producer Price Index – June

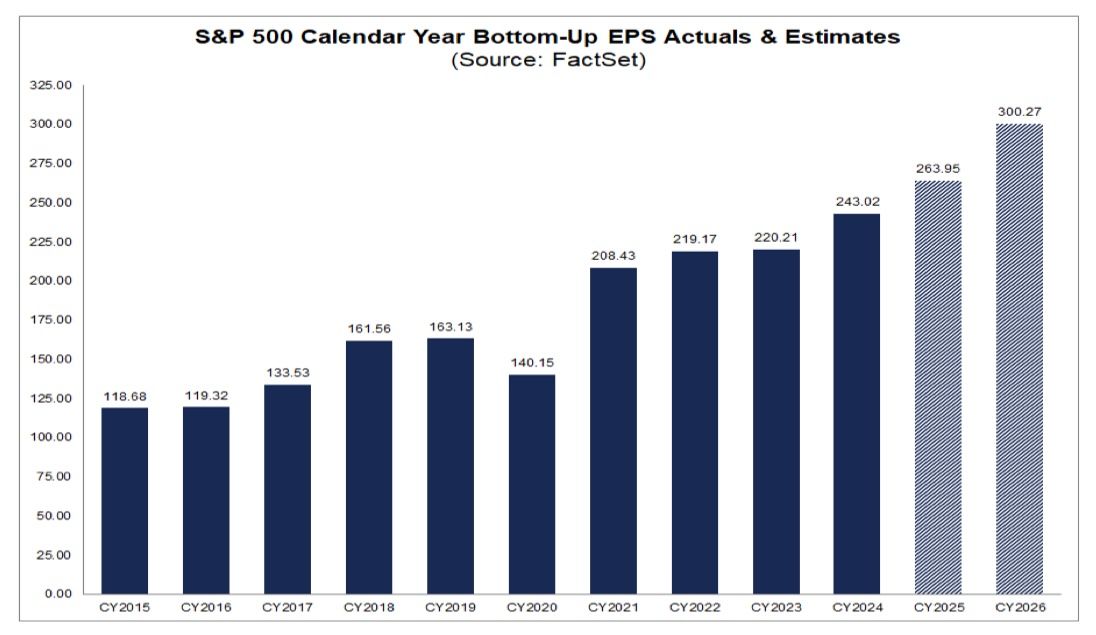

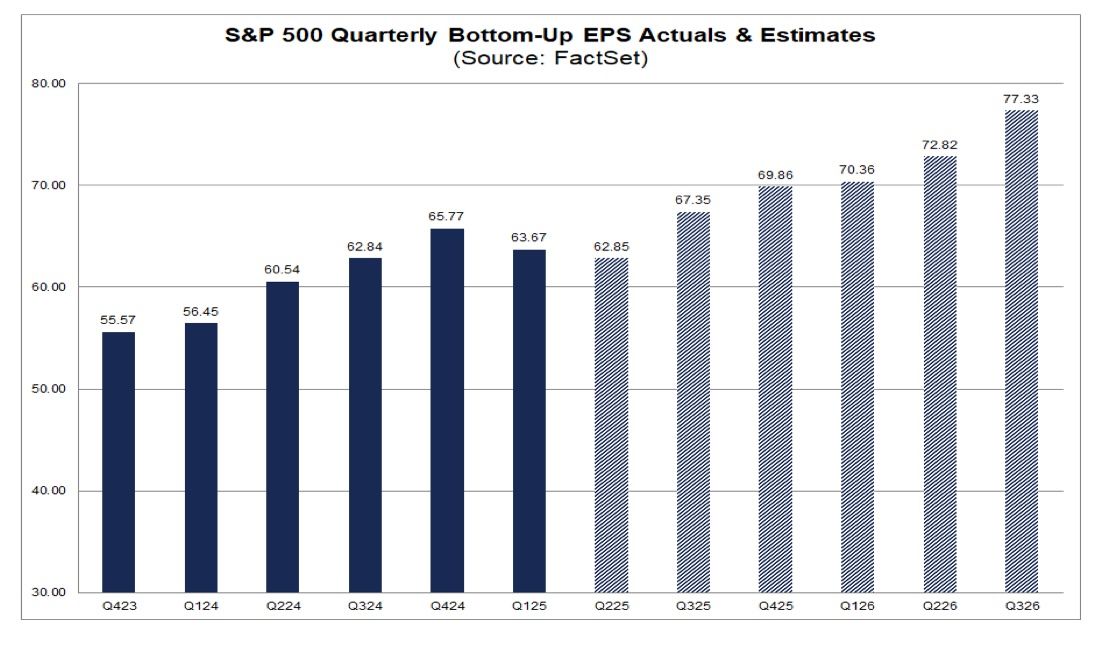

As we get ready for the June-quarter earnings season, let’s revisit consensus EPS expectations for the S&P 500.

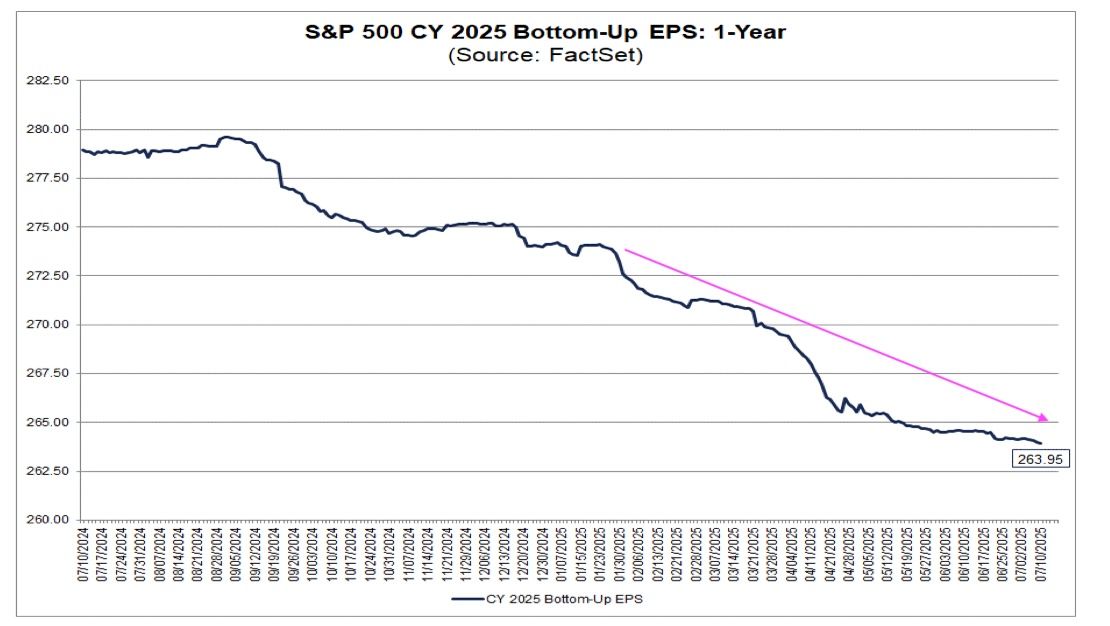

As of July 11, data collected by FactSet has consensus EPS expectations for the S&P 500 rising 8.6% year over year to $263.95. However, as the below chart clearly shows, the expectation for EPS growth compared to 2024 has been declining over the last several months.

The key to hitting the market’s 2025 EPS growth expectations will hinge on the second half of the year, and, as we’ve discussed several times, those expectations have also declined in recent months thanks to the onset of tariffs and concern over their impact. As of July 11, the basket of companies that comprise the S&P 500 is expected to deliver aggregate EPS growth of 8.4% in the H2 2025 compared to H1 2025. While steady week over week, it’s still a far cry from the 13.9% figure that the market had penciled in at the end of March.

We share this with you because what we learn from companies in the next few weeks about their Q2 2025 performance and expectations for the current quarter will foster further changes in those EPS growth expectations. The same is true with what may or may not happen on the trade deal and tariff front, and until we see meaningful progress in that area, we continue to think related uncertainty will prompt companies to skew their updated guidance conservatively.

The degree to which that is the case will become clear in the next few weeks, but an initial look will come with next week’s quarterly earnings reports. As we digest those reports and their implications, we’ll connect the dots to the economy, market sectors, and the Pro Portfolio’s holdings.

In terms of Pro Portfolio companies reporting next week, Morgan Stanley MS and Bank of America BAC will deliver Q2 2025 results on Wednesday, July 16. We’ll get a preview of sorts the day before when JPMorgan Chase JPM, Citigroup C, and Wells Fargo WFC report. Coming off the results of the Fed’s stress tests and improving investment banking activity, we expect upbeat reports and, at a minimum, reiterated guidance. Should the outlooks shared by Morgan Stanley and BofA be revised higher, we’ll revisit our corresponding price targets as necessary.

Next week also brings quarterly results and guidance from Taiwan Semiconductor TSM on Thursday, July 17. Because the company reports monthly revenue figures, we will be interested in its segment performance for the June quarter and its end-market outlook for the current one. We suspect we won’t be the only ones assessing those remarks as they relate to the Pro Portfolio’s positions in Nvidia NVDA, Marvell MRVL, Apple AAPL, Qualcomm QCOM, and Universal Display OLED.

Here's a closer look at the earnings reports coming at us next week:

Monday, July 14

· Open: Fastenal (FAST)

Tuesday, July 15

· Open: Albertsons (ACI), BlackRock (BLK), BNY Mellon (BK), Citigroup (C), Ericsson (ERIC), JPMorgan (JPM), Wells Fargo (WFC)

· Close: JB Hunt (JBHT),

Wednesday, July 16

· Open: ASML (ASML), Bank of America (BAC), Goldman Sachs (GS), Johnson & Johnson (JNJ), Morgan Stanley (MS)

· Close: Alcoa (AA), United Airlines (UAL)

Thursday, July 17

· Open: Abbott Labs (ABT), Cintas (CTAS), Elevance Health (ELV), PepsiCo (PEP), Taiwan Semiconductor (TSM)

· Close: Interactive Brokers (IBKR), Netflix (NFLX)

Friday, July 18

· Open: 3M (MMM), American Express (AXP), Charles Schwab (SCHW)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.