Weekly Roundup: Israel-Iran Conflict, Uncertainty Erase Week's Gains

Middle East developments, trade deals, and the Fed are on our radar. Here's our plan amid a host of unknowns.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market and investors contended with various puts and takes during the week, including sobering findings from U.S.-China trade talks and favorable May inflation data. The net effect led the S&P 500 higher through its close Thursday night, but the week’s gains were erased following Israel's airstrikes on Iran and Iran’s reciprocal attacks. Oil and gold prices surged as did other safe-haven stocks, but continued attacks and related uncertainty led the market to finish lower week over week. Friday morning, we shared our expectation for a late-day sag in the market as short-term traders sought to limit exposure heading into a weekend whose developments will dictate how the market opens on Monday.

Looking at those potential developments, reports indicate Iran will not participate in the sixth round of nuclear negotiations with the United States scheduled for this weekend. We will closely track weekend developments as they will likely shape how next week’s abbreviated market activity begins. We’ll also be monitoring any movement on the trade deal front. While the U.S. and China agreed on a deal framework, it has yet to be approved by Presidents Trump and Xi. There is also the question as to when it might be implemented given a 90-day pause on some tariffs is scheduled to expire in August. We’ll also follow trade conversations between the U.S. and the European Union, but a deal before the July 9 deadline appears less and less likely.

Naturally, we'll be assessing what these developments mean for the economy, sector demand, and earnings prospects for the second half of 2025 and 2026. Our view remains that the longer tariffs are in place and trade remains uncertain, the more likely we’re going to receive cautious guidance. Speaking at the Morgan Stanley U.S. Financial Conference on Tuesday, JPMorgan Chase JPM CEO Jamie Dimon commented that, between trade and geopolitics, there are “a lot of moving parts” but tariffs are “hitting,” and we will see bigger impacts in the coming months. We see that supporting our thinking that, barring trade deals and their details, we are likely to see companies reset earnings expectations further for H2 2025.

Over the last few weeks, consensus S&P 500 EPS expectations for Q2 2025 have fallen almost 6% to $62.85 as the market adapted recent economic data and tariffs into its thinking. While there have also been downward revisions for H2 2025 S&P 500 consensus EPS expectations, they still call for ~8.5% growth compared to H1 2025 with Q3 2025 EPS expected to rebound 7.4% compared to the current quarter. Early this year Q3 2025 EPS was expected to rise 6.0% from Q2 2025, so, barring meaningful trade deal progress near-term, what is fueling that accelerated EPS expectation?

We continue to think the longer we go without final trade deals, terms, and timing for their implementation, the more likely that uncertainty and existing tariffs will combine to foster another round of caution-skewed guidance. Gaming it out, more substantial cuts resulting from company guidance in the soon-to-be U.S. June-quarter earnings season are a potential headwind for the market. The closer to that earnings season we get without trade deals and their details or the passage of Trump’s “big, beautiful deal,” which would bring its own clarity on tax reform and other issues, the more likely that headwind becomes.

As we track these and other developments, we continue to keep an eye on key technical levels. Rest assured that if we need to re-position the Pro Portfolio, we’ll take prompt action and share our moves with you.

Catching Up on the Portfolio This Week

As we discussed above, the bulk of the market’s gains early in the week were erased on Friday following the Thursday night and early Friday attacks by Israel and Iran. While that led the Pro Portfolio’s Safety & Security positions, Axon Enterprise AXON and Palantir PLTR to close the week out on a high note, as we discussed in Friday’s video, it weighed on some of our higher-beta holdings, such as Dutch Bros BROS.

We recognize that stock prices can be volatile week to week, but measured against the quarter-to-date performance for the S&P 500, 18 of the Pro Portfolio’s current 25 positions are outperforming. That performance enabled the pro Portfolio to pull ahead of the market, a position it continues to enjoy even after this week’s developments.

We made no trades in the Pro Portfolio this week. Even though we’ve selectively put some cash to work recently in Elastic ESTC, Marvell MRVL, and SuRo Capital SSSS, moves we made in late May, we still have our cash levels in the low double-digits. That will help insulate the Pro Portfolio near term while giving us resources we can selectively use should the right opportunity emerge.

With that in mind, we’ll continue to heed the ripped-from-the-headlines signals and confirmation points for the Pro Portfolio’s strategies. Our next batch will be in your email on Saturday morning. We’ll also continue to monitor relative strength index (RSI) levels for our holdings and share an updated table containing those figures as well as updated consensus EPS expectations and beta levels on Monday.

Now, let’s see what Wall Street and others had to say about Pro Portfolio holdings this week…

Citing an email a senior executive sent to staff, The Information writes Alphabet's GOOGL Google is offering buyouts to U.S. workers in the knowledge and information division, which includes the company's core search and much of the ads business. We would not be surprised to see Google follow Amazon AMZNand Meta META in using AI to streamline its advertising business. The Information also reports Google has signed a deal with data warehousing startup Databricks to host its artificial intelligence Gemini models.

Rumblings indicate Amazon’s Prime Day will be extended from the usual two days to four days this July.

The Wall Street Journal reports Amazon, Walmart WMT, and Expedia EXPE have explored issuing their own stablecoins in the U.S. Stablecoins are digital tokens designed to be pegged one-for-one to an actual asset, such as a fiat currency, most often the U.S. dollar. This would land under our Digital Payments thematic, and we’ll keep tabs on this to see if this develops further for those three companies and others.

Apple's AAPL iPhone claimed the top spot in China for May smartphone sales, Reuters reported. April and May saw 15% year-over-year growth in global sales, the strongest two-month period since the Covid-19 pandemic.

Barclays raised the firm's price target on Eaton ETN to $323 from $306.

Morgan Stanley raised its price target on Labcorp LH to $283 from $270 and maintained an Overweight rating on the shares.

BofA raised its price target on Meta Platforms to $765 from $690 and kept a Buy rating on the shares, citing easing tariff-related macro uncertainty and multiple expansion in the broader market for its increased price target.

Citi raised its price target on Microsoft MSFT to $605 from $540, keeping a Buy rating on the shares. The firm also added an "upside 90-day catalyst watch" on the shares. Citi says Microsoft remains its top pick in software given the company's "relative defensiveness in a choppy macro environment," artificial intelligence product cycle, and "reinforced conviction" that Wall Street estimates on Azure may be too low for fiscal 2026.

Sticking with Microsoft, Business Insider writes the company is working on a version of its 365 Copilot AI tool for the Pentagon and is expected to become available no earlier than summer 2025.

Wells Fargo raised its price target on Microsoft to $565 from $515 and reiterated it as a Buy, sharing it sees a second half of-the-year rebound in the software sector.

Loop Capital analyst Mark Schappel raised the firm's price target on Palantir to $155 from $130 and keeps a Buy rating on the shares. We recently lifted our PLTR target to $140 from $130 but plan on revisiting it again following the company’s next AIPCon event.

Redburn Atlantic downgraded United Rentals URI to Neutral from Buy with a $760 price target.

Ahead of Waste Management’s WM 2025 Investor Day on June 24, Melius Research initiated coverage of WM shares with a Buy rating and a $263 price target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, June 9: What We Expect From U.S.-China Trade Talks, Apple’s WWDC Keynote

Tuesday, June 10: For Meta, Amazon, and Apple, AI Remains the Name of the Game

Wednesday, June 11: TheStreet Stocks & Markets Podcast #9: Market Pulse Check With Bob Lang

Thursday, June 12: Thematic Investing, 'Real-World' Signals, and My Call With Peter Lynch

Friday, June 13: Why These Positions Are Moving to the Downside

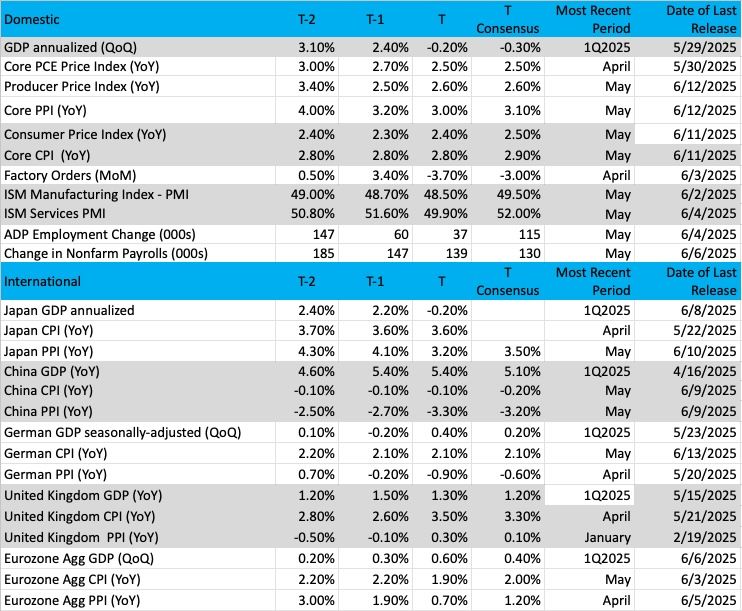

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: The Volatility Index

It is time to watch market volatility closer than ever before. The drop in the VIX over the past few months from about 60 to current levels in the mid-teens has been very bullish for markets. Remember, when there is less fear of a drop in markets the VIX falls and acts as "fuel" for the bulls. In addition, the dip buyers become more active, adding to their holdings and trading much more frequently as the conditions become ripe for profits. Most traders and investors make money when the market is going up, while even the most stubborn bears often have bullish trades working as well (though they will never admit to that).

This drop into the mid-teens in the VIX has trouble written all over it, however. We are not talking about the end of this bull run just yet, rather that buyer exhaustion is starting to set in. What does that mean? Basically, investors and traders are running out of money (at the moment). We see a lack of liquidity in markets with erratic price moves and sharp jumps up/down in equity futures. That is not common when money is flowing big and free in the markets.

This condition can last for much longer than anyone expects, and the longer market complacency exists the less any investor/trader believes the markets will pull back. In other words, it becomes a constant "buy the dip" mentality. Still, we know eventually that logic will fail because that last dip won’t be bought and some investors will be severely hurt. We simply need to be aware of the conditions at all times.

Taking a look at the chart, the VIX is starting to rumble. Investors and traders are getting nervous, and for good reason. We notice in March when the VIX was this low it exploded higher out of nowhere, as the S&P 500 fell about 20% in a short three weeks. That was difficult to stomach. The chart is showing some complacency and a 40% move up to 24 on the VIX might be enough of a move to wash out some of the recent speculation. How does that translate into market action? That would probably be a 5-6% move lower in the S&P 500, so we’ll keep monitoring the move up in VIX.

Right now, the fear index (VIX) is below the 200-day moving average (19.63) and that is okay to rise up too, burning off some of the highly speculative trading that has been happening of late. We see that with the rise of small-caps and even micro-caps, as traders/investors late to the party look to speculate on cheap names. When this happens the market trend is about to change to bearish (at least for a while). This is what makes us worried about this low VIX.

Could it stay low (in the teens) for a long period? Certainly, but that would embolden the bulls even more and make the next large pullback even more difficult to buy.

Other charts we shared with you this week were:

Monday, June 9: S&P 500 - Reaching Toward All-Time High

Monday, June 9: Palantir (PLTR) - Palantir Just Might Be Unstoppable. For Now.

Tuesday, June 10: Apple (AAPL) - WWDC Fails to Move the Needle on Apple

Wednesday, June 11: T-Mobile (TMUS) - T-Mobile Indicator Is Ringing and We're Listening

Thursday, June 12: Bank of America (BAC) - Bank of America Looks a Bit Tired

The Week Ahead

It won't be a typical five-day trading week next week. The market will be closed on Thursday, June 19 for the Juneteenth holiday. And as we near the end of the current quarter, we would not be surprised to see many folks turn the holiday into a four-day weekend. While some may do that, given our discussion about options expiration on Friday, June 20, in this week’s Stocks & Markets Podcast, it will be all hands on deck for us.

But before we get to those last two days of next week, we will first have to traverse the first three. They will bring us the May Retail Sales report, the latest indication of consumer spending, and May Housing Starts. Those are the last two bits of economic data before the Fed concludes its June policy meeting. Exiting that event, the central bank isn’t expected to deliver a rate cut but it will publish its updated set of economic projections.

The last set of such projections delivered in March indicated two 25-basis point rate cuts were on the table for this year and showed the Fed reduced its GDP forecast for 2025. Exiting this week, the New York Fed Staff Nowcast model pegs Q2 2025 GDP at 2.34% while the Atlanta Fed’s rolling GDPNow model has it at 3.8%. We’ll want to revisit the GDPNow model following its next update on June 17.

Data over the last several weeks point to a stronger economy and inflation being tamer than many feared. In breaking down the May CPI report, we explained that what we’re likely seeing in the data is a combination of companies chewing through existing inventories, and some retailers leaning into promotions and discounting to drive comp sales. Walmart WMT, e.l.f. Beauty ELF, Best Buy BBY, Ford F, Procter & Gamble PG, Macy’s M, and Mattel MAT have either recently enacted tariff-related price hikes or plan to do so.

We continue to think the longer we go without trade deals and their agreed-upon and final details, the more likely we will see a more pronounced impact of existing tariffs in the data, on the economy and earnings. Odds are that is what the Fed is thinking as well, which explains why it will likely reiterate that it will want to see and digest more data to determine what’s next for the Fed funds rate. As of now, the market sees the Fed cutting interest rates next at its September policy meeting. While that will provide multiple months of data to chew through it also means the longer we go without finalized trade deals, the more likely the impact of tariffs will show up in the data.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, June 16

· Empire State Manufacturing Index – June (8:30 AM ET)

Tuesday, June 17

· Import/Export Prices – May (8:30 AM ET)

· Retail Sales – May (8:30 AM ET)

· Industrial Production and Capacity Utilization – May (8:30 AM ET)

· Business Inventories – April (10:00 AM ET)

· NAHB Housing Market Index – June (10:00 AM ET)

Wednesday, June 18

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Housing Starts & Building Permits – May (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Rate Decision and Updated Economic Projections – 2 PM ET

Thursday, June 19

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, June 20

· Philadelphia Fed Index – June (8:30 AM ET)

· Leading Indicators – May (10:00 AM ET)

International

Monday, June 16

· China: Industrial Production, Retail Sales, Fixed Asset Investment – May

· Eurozone: Labor Cost Index, Wage Growth – Q1 2025

Tuesday, June 17

· Eurozone: ZEW Economic Sentiment Index - June

Wednesday, June 18

· UK: Inflation Rate – May· Eurozone: CPI (Final) - May

Thursday, June 19

· UK: Bank of England Interest Rate Decision

Friday, June 20

· Japan: Inflation Rate – May

· Germany: PPI – May· UK: Retail Sales – May

· Eurozone: Consumer Confidence (Flash) - June

The volume of quarterly earnings reports declines next week as does the number of investor conferences. This likely means the main drivers of the market will be geopolitical developments, trade deals progress, and the Fed. We will still mine for nuggets where we can and connect what we learn back to the Pro Portfolio. In addition to earnings from Lennar LEN, Accenture ACN, and Kroger KR, we’ll sift through presentations from the Jefferies Consumer Conference and the Wolfe Research Materials of the Future Conference.

Here's a closer look at the earnings reports coming at us next week:

Monday, June 16

· Close: Lennar (LEN)

Tuesday, June 17

· Open: Jabil (JBL),

Wednesday, June 18

· Open: · Close: Smith & Wesson (SWBI)

Friday, June 20

· Open: Accenture (ACN), CarMax (KMX), Darden Restaurants (DRI), Kroger (KR).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.