Weekly Roundup: Iran and Energy Worries Take Their Toll on the Market

We made multiple moves, including exiting a consumer name, adding portfolio protection, and locking in an outsized gain on a domestic play.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Market Drop

Market Drop

The market faced another down week with moves lower in all four major market indexes. Indeed, the S&P 500, the Nasdaq Composite, and the Russell 2000 fell for a third consecutive week. The culmination of those moves has landed all four of the major indexes (including the Dow) in the red on a year-to-date basis, and we are in that camp with them. And while the Cboe Volatility Index (VIX) bounced around this week, as did the market, it closed at levels not far off where they were last Friday. In other words, volatility was elevated as we head into the weekend.

Tracing back the events of the week that weighed on the market and led the VIX to remain at relatively high levels, they are ones we discussed several times over the last few days. The U.S.-Iran conflict, energy prices and concerns over the impact on inflation, consumer spending, and the overall economy.

We can also include private credit worries following reports that JP Morgan (JPM) marked down the value of certain loans to private credit players and will reduce its lending to those funds. Morgan Stanley (MS) limited redemptions at one of its private credit funds, and that added to those concerns as well as weighed on our MS shares. We’ll have more to say on that and private credit as we start off next week.

Despite claims from several in the White House that the U.S.-Iran conflict would be over soon, on Friday, reports indicated the Pentagon is moving additional Marines and warships to the Middle East as Iran steps up its attacks on the Strait of Hormuz. As we discussed during the week, the key to the conflict for us as investors is captured is one word – duration. The greater the duration, the larger the impact higher oil, gas, diesel and other energy prices will have. Recognizing that likelihood, we shed our lone consumer discretionary play, Dutch Bros (BROS) , early this past week and added some Portfolio protection.

While it appears the conflict could be an extended one, we also recognize the likely political risk it poses to the mid-term elections. That, in our view, explains the stepped-up U.S. efforts late this week to bring the conflict to a close.

Weekend developments will be critical and set the stage for how we begin trading for the second half of March on Monday. That means we’ll be rolling up our sleeves over the weekend to assess those developments, but also what they mean relative to key technical support levels for the S&P 500 and the Nasdaq Composite. While the S&P 500 is still hovering above its 200-day moving average near 6604, the Nasdaq Composite moved through that support level at 22,175.

That means before we contemplate making any moves, we will be looking to see if the Nasdaq delivers a positive test of that support level early next week and if the S&P 500 treats its 200-day moving average as a level of support. At the same time, we’ll be eyeing their relative strength index (RSI) levels, which as of Friday’s close did not indicate an oversold condition. We can afford to be patient and bide our time, letting our cash and inverse S&P 500 ETF shares do their job.

Enjoy your weekend and Saturday’s Signals alert. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

With all four major market averages declining week over week, the Portfolio felt that combined weight. We still had several bright spots, however, including the double-digit jump in the shares of SuRo Capital (SSSS) and relative outperformance in more than half a dozen other holdings. However, those gains fell short of making up for the larger moves lower in Axon (AXON) , United Rentals (URI) , ServiceNow (NOW) , Netflix (NFLX) , and Meta (META) .

The market’s drop this week also weighed on the EPS Diplomats basket, but while the S&P 500 moved deeper into a year-to-date loss, the Diplomats remain nicely positive with a mid-single-digit gain YTD. We used Friday’s video to share that when we next reconstitute the Diplomats basket between March 31-April 1, we’ll be doubling the overall position weighting to 4% of the Portfolio, up from 2%.

We started the week off pulling the rip cord on our position in Dutch Bros (BROS) given escalating energy costs that are shaping up to be a consumer-spending headwind. As we made that trade on Monday, we also added a defensive play for the Portfolio in the form of ProShares Short S&P 500 ETF (SH) shares. We do not see SH as a long-term holding for the Portfolio, but one we are employing in the short-term to tamp down market volatility in the current geopolitical environment. Should the U.S.-Iran conflict become a protracted one, given the potential risks to existing consensus EPS expectations, we may be inclined to hold SH as the Q1 2026 earnings season gets underway.

On Monday, we also locked in a nice 30% gain on a slice of Waste Management (WM) shares. The overbought condition that led us to book that gain also led us to downgrade our rating on WM to Two from One.

On Wednesday, we picked up additional shares of Morgan Stanley (MS) and Bank of America (BAC) , upgrading BAC to a One rating in the process. The catalyst for those moves was a combination of the recent pullback in the shares, upbeat data points on M&A activity as well as quarter-to-date market volatility being a nice tailwind for their trading and market-related businesses. Also on Wednesday, we lifted our price target for SuRo Capital (SSSS) to $14 from $12 and laid out our dividend expectations for the company.

Those moves, along with the receipt of the latest quarterly dividends from Welltower (WELL) and Labcorp (LH) left the Portfolio’s cash position near 8.7% as we closed out the week. In Friday’s video, we explained we are closely watching shares of Axon (AXON) and American Express (AXP) with an eye toward buying more of each. We are also continuing our work on recent Bullpen addition, Idexx (IDXX) , as well as a few other stocks. The recent pullback in Netflix (NFLX) also has us examining support levels.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday – BofA trimmed its American Express target to $382 from $420 but reiterated its Buy rating.

Tuesday – JPMorgan increased its Morgan Stanley target to $179 from $173.

Wednesday – TD Cowen initiated coverage on shares of Arista Networks (ANET) with a Buy rating a price target of $170. Barrington Research boosted its SuRo Capital target to $15 from $12.

Thursday – Citizens raised its SuRo Capital target to $13 from $11.

Friday – Wolfe Research initiated coverage on Waste Management shares with a Peer Perform and no price target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our videos. If you happened to miss one or more of them, here are some helpful links:

Monday, March 9: Markets Reverse Late as Oil, War Headlines, and Fed Fears Collide

Wednesday, March 11: Stocks & Markets Podcast: Key S&P 500 Levels to Watch as Oil Prices Surge

Thursday, March 12: Oil Just Hit $100+. Is $150 Next?

Friday, March 13: Updates on 3 Holdings Under Pressure, and EPS Diplomats News

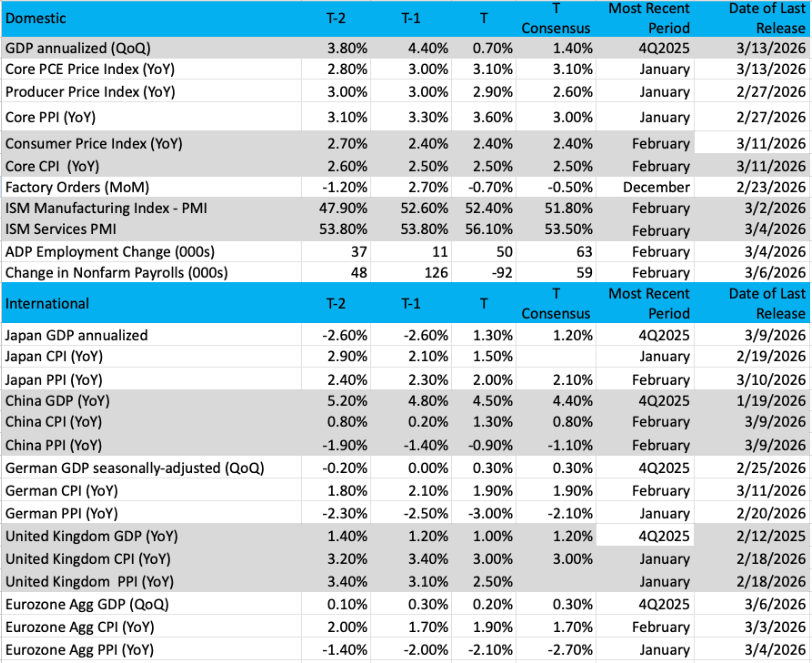

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

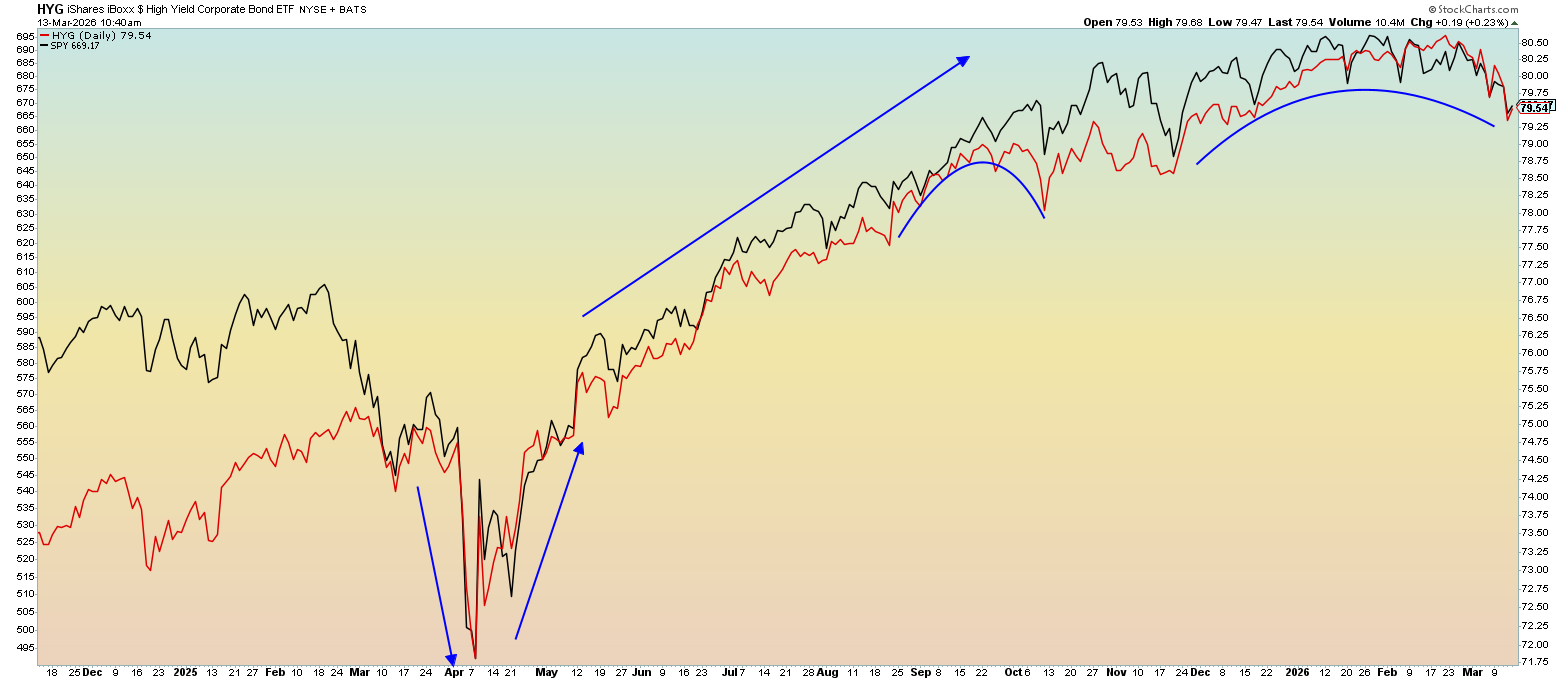

Chart of the Week: iShares iBoxx High Yield Corporate Bond ETF (HYG)

We don’t often talk about bond investing/trading in our reports, but it is very important to monitor the movement in bond prices and yields. As you know, yields move inversely to prices (in equities, the same relationship exists between stocks and dividend yields).

Along the term structure of interest rates (yield curve) there are different maturities and risk levels. When looking at risk, the high-yield segment offers the best returns for bond investors on a standard basis, but the level of risk is highest. Think of high yield/junk as a pseudo stock, instruments that perform well when the economy is strong.

Now, what companies offer high-yield bonds to investors? No question these offerings are made by companies that have very poor credit quality, weak cash flows and are at risk for re-payment. Investors require a higher rate of return for the risk taken on these bonds, so if they do end up being paid off there is an attractive total return.

As one might expect, the high-yield segment has a strong positive correlation to equities. In fact, looking at the chart, below, they are nearly a firm fit on top of each other. They correlate nearly 80% of the time as high yield often acts like a risky asset (stocks being the riskiest in the investment frontier).

Lately, the chart shows both the S&P 500 and high yield area starting to falter. Is it time to be concerned? Yes, but we're not overly worried. Recent failures by both indexes have shown strong rebounds, right through new all-time highs eventually. The chart here shows a rollover, however, with not much power to the upside and a series of lower highs and lower lows, our textbook definition of a downtrend.

This pattern could be interpreted as more than a slowdown, perhaps a recession down the road. But let’s not put the cart before the horse. We did experience a huge drop in high yield and a blowout in spreads about a year ago (see on the chart) and a swift bounce. Keep one eye on the (HYG) or (JNK) ETFs, they will tell us as much about the economy as the data.

Other charts we shared with you this week were:

Monday, March 9: S&P 500 - Cracks Show as Volatility Takes Center Stage

Monday, March 9: Arista Networks (ANET) - Holding Firm at a Reliable Support Zone

Tuesday, March 10: American Express (AXP) - Now Might Be a Good Time to Buy American Express

Wednesday, March 11: The Hershey Company (HSY) - This Bullpen Name Is on Our Radar Amid Shift to Staples

Thursday, March 12: Bank of America (BAC) - Is Good News on the Horizon for Bank of America?

The Week Ahead

As we discussed above and in Friday’s video, we will be closely watching weekend developments for the U.S.-Iran conflict and the Strait of Hormuz. Subject to those developments, when Monday rolls around, we’ll have early comments laying out our thoughts and potential actions.

Outside of that, and from an economic and monetary policy perspective, the two main events next week will be the February Producer Price Index report and the Fed’s latest monetary policy meeting. Both of those come on Wednesday, and our thinking is that if weekend signs point to a continued U.S.-Iran conflict, market watchers will note the February PPI data, but be more focused on gas, diesel, jet fuel, and other prices in March and what they are likely to mean for March inflation data.

For the Fed, the market does not expect a rate cut, but given recent developments on the inflation front and the disappointing February Employment Report, we’ll be listening to see which is viewed by the Fed as a greater risk to the economy — rekindled inflation pressures or the jobs market. Based on those comments and what we see in the updated Set of Economic Projections, we’ll revisit rate-cut expectations tracked by the CME FedWatch Tool. As we pointed out to you on Friday, those expectations have already been reset over the last few weeks, with the next rate cut not expected until December 2026.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, March 16

Empire Manufacturing Index – March (8:30 AM ET)

Industrial Production & Capacity Utilization – February (9:15 AM ET)

Tuesday, March 17

ADP Employment Change Report - Weekly – (8:15 AM)

NAHB Housing Market Index – March (9:00 AM ET)

Pending Home Sales – February (10:00 AM ET)

Wednesday, March 18

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Producer Price Index – February (8:30 AM ET)

Factory Orders – January (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

FOMC Decision – 2 PM ET

Thursday, March 19

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Philadelphia Fed Index – March (8:30 AM ET)

New Home Sales – January (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

International

Monday, March 16

China: Industrial Production, Retail Sales - February

Tuesday, March 17

China: Financial Direct Investment – February

Eurozone: ZEW Economic Sentiment Index - March

Wednesday, March 18

Japan: Import/Exports – February

Eurozone: Inflation Rate - February

Thursday, March 19

Japan: Machinery Orders, Industrial Production & Capacity Utilization – January

Japan: Bank of Japan Interest Rate Decision

UK: Employment Change - January

Eurozone: Labor Cost Index – Q4 2025

Eurozone: European Central Bank Interest Rate Decision

Friday, March 20

Germany: Producer Price Index - February

We have what seems like a rare week on the earnings front, as no Portfolio holdings are reporting. However, we will be very interested in comments and guidance from Micron (MU) as well as FedEx (FDX) when they report next week. Based on recent guidance from Dell (DELL) , Hewlett Packard Enterprise HPE, and others, we suspect Micron’s outlook will be favorable, especially for the AI and data center market. We’ll be interested to see if the demand from that market is so strong that Micron needs to readjust its outlook lower for the smartphone, PC, and other connected devices market.

We will also be paying close attention to what is said about transportation and other input-related items, especially from General Mills (GIS) , Macy’s (M) , and Lululemon (LULU) . Why Lululemon? Because traditional petroleum-based synthetic materials like nylon, polyester, and spandex are heavily used in its products.

Besides the known corporate earnings reports, next week also brings GTC 2026 with a keynote from Nvidia’s (NVDA) Jensen Huang on Monday, March 16, at 2 PM ET. The address is expected to include Nvidia’s latest advancements across the full AI stack, from accelerated compute and AI factories to open models, agentic systems, and physical AI. The larger event should showcase every layer of AI, spanning energy, chips, infrastructure, models, and applications, which means we should expect a flurry of press releases and announcements.

Like the annual Consumer Electronics Show in January, but on a somewhat smaller scale, as we collect those announcements, we’ll assess their implications and tie them back to our holdings.

Jensen will also host a panel at GTC on Wednesday, March 18, titled “Open Models: Where We Are and Where We’re Headed.” He’ll be chatting with representatives from Ai2, Cursor, Langchain, Mistral, and others about open frontier models and what comes next.

Here's a closer look at the earnings reports coming at us next week:

Monday, March 16

Open: Dollar Tree (DLTR), Science Applications (SAIC)

Tuesday, March 17

Open: Tencent Music (TME)

Close: DocuSign (DOCU), Lululemon Athletica (LULU)

Wednesday, March 18

Open: General Mills (GIS), Jabil (JBL), Macy’s (M), SailPoint (SAIL), Williams-Sonoma (WSM)

Close: Five Below (FIVE), Micron (MU)

Thursday, March 19

Open: Accenture (CAN), Darden Restaurants (DRI)

Close: FedEx (FDX)

Friday, March 20

Open: Carnival (CCL)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.