Weekly Roundup: Here’s Our Near-Term Plan as Multiple Headwinds Come to Bear

This week, we put more capital to work in two holdings, opportunistically locked in big gains in another and, prompted by management concerns, exited a position.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In our October Monthly Roundup, we noted the extended positive run in the S&P 500, Nasdaq, and the Pro Portfolio over the last several months. We also noted that despite that string of gains, there were still several hurdles yet to clear, including the government shutdown, an increasingly bifurcated consumer, and growing layoff activity. Those items weighed on things across the board this week, as did renewed questions over market and stock valuations, and a potential AI bubble.

Those factors, which culminated with the Fear & Greed Index landing back in “Extreme Fear,” led to hasty market behavior even with companies that delivered beat-and-raise earnings reports. Even would-be good news, with rolling GDP forecasts moving higher following the upturn found in the October Services ISM data, was short-lived. That same ISM data also showed input prices stepping up yet again, which reaffirmed our focus on company operating margins.

Amid the dearth of fresh economic data amid the shutdown, the October Challenger Job Cuts report showed job cuts for the month hit the highest level in 22 years, while the ADP’s monthly employment data showed the job market moved back into job gains. However, that 42,000 figure was still far weaker compared to first-half 2025 levels.

As we see it, it will take some time for layoffs to filter their way into the weekly jobless claims and other measures of the job creation. However, the layoff headlines and the preliminary November reading for the University of Michigan’s consumer sentiment index, which hit its second-lowest level on record, are reasons to think consumers could be even thriftier than previously expected.

Approaching Friday’s market close, the S&P 500 and the larger market rebounded following reports that Democrats offered a trimmed-down set of demands to end the shutdown. However, because we are not ones to give into hopium, we will need to see if this is enough to get the Republicans and the White House on board for a deal that would bring an end to the standoff. With the FAA starting to pare flights on Friday and more folks feeling the pinch of what is now the longest ever shutdown, a deal would be a welcome event.

Still, we have to realize that the eventual reopening of the government isn’t like opening a water faucet. By that, we mean it will take a bit of time before things are back up and running. And when that happens, it means we will eventually need to be ready for all the missed economic data to be published and the updated picture it presents.

Netting all of those potential knowns out and being mindful of potential unknowns following the market’s reaction to even positive earnings reports this week, we’ve adopted a more cautious mindset. Given our Stocks & Markets podcast conversation this week with Jay Woods, which flagged the potential for a continued market selloff, we’ll proceed carefully near term and not rush headlong into things.

We will also pay extra close attention to market dynamics and technicals, especially if the S&P 500 breaks support of its 50-day moving average at 6669. If that happens, the next layer of firm support is at the 100-day moving average, which is another 2.7% lower near 6488. We will also keep our eyes on the CBOE Volatility Index, the Fear & Greed Index, and market oscillators. That combination will help keep us on the smarter path as we digest incoming data and developments in Washington, while we look to further flesh out our shopping list beyond what’s on it today.

We were knocked back this week, but by no means were we knocked out. We’ve upped our cash levels, we have our shopping list, and we’ll continue to follow the data, connecting the dots along the way. If we see a sharp market pullback like we saw a few times in 2024 and again earlier this year, we’ll be ready to take advantage.

Enjoy your weekend, Saturday’s signals alert, and Sunday’s bowl of more light-hearted fare. I’ll see you back here on Tuesday, and Bob Lang will have the reins on Monday.

Catching Up on the Portfolio This Week

As much as we like it when the Pro Portfolio does well, we also have to acknowledge when there are setbacks. This first week of November was just that for the Portfolio and the market, with shares of Arista Networks (ANET) , Axon Enterprise (AXON) , Palantir (PLTR) , and Universal Display (OLED) weighing heavily on it.

The Nasdaq Composite declined nearly 3.0% week over week, and the Portfolio was also impacted by its exposure to tech and growthier names. There were, however, several positions that outperformed the S&P 500 and its 1.6% week-over-week decline. Those included Apple (AAPL) , Amazon (AMZN) , American Express (AXP) , Bank of America (BAC) , Costco (COST) , Alphabet (GOOGL) , Morgan Stanley (MS) , TJX Companies (TJX) , Welltower (WELL) , and Waste Management (WM) .

This week, the Portfolio used post-earnings reactions to add shares of Arista Networks and Axon Enterprise at $142.67 and $563.84, respectively. We also took advantage of a new report on some old news for Marvell (MRVL) , which popped the shares and led us to lock in an 89% gain on that slice of our holdings.

On Friday, following a sizable September-quarter earnings miss and underwhelming commentary from the management team, we exited our position in Universal Display (OLED) for a double-digit loss. As we explained in that trade Alert, while this was a painful setback, it was the prudent action to take given concerns over management credibility and visibility.

The combination of those moves left us with 25 active positions and a cash position totaling about 11.5% of Portfolio assets. Upcoming quarterly dividend payments from American Express, Apple, Morgan Stanley, Costco, Welltower, Eaton (ETN) , and United Rentals (URI) later this month will bring us additional cash. Should we get a market bounce, we will be sure to see what that means for some Portfolio names that are approaching a 4.5% position size. While not directly sitting on top of that level, shares of Alphabet, Bank of America, and American Express are in close proximity and bear keeping an eye on.

Our updated wish list of stocks to buy includes Welltower, TJX Companies, Arista Networks, and, as we discussed on Friday, the First Trust Nasdaq Cybersecurity ETF (CIBR) . We also have additional room in a few other positions, such as Meta (META) , but we will balance that against renewed efforts to position the Portfolio for the coming quarters with a new name or two.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday — Wedbush raised its Amazon target by $10 to $340, while Goldman Sachs lifted its Nvidia (NVDA) target by $30 to $240. The same day, Loop Capital made a big increase to its NVDA target, taking it to $350 from $250. Bernstein raised its Apple target to $325 from $290, citing a better-than-expected iPhone outlook. Oppenheimer named Costco a Top Pick.

Tuesday — Baird lifted its Palantir target to $200 from $170, while DA Davidson and Morgan Stanley boosted their respective targets to $215 and $205, from $170 and $155. However, BofA took the lead by upping its PLTR target to $255 from $215. Mizuho increased its Amazon target to $315 from $300, and Baird increased its rating on Waste Management shares to Outperform with a new $242 target.

Wednesday — Barrington Research raised its target for SuRo Capital (SSSS) to $12 from $11 while RBC nudged its Eaton target to $432 from $405. Barclays lifted its Arista Networks target to $183 from $179. Shares of Welltower were upgraded to Outperform with a new $208 target at Evercore ISI.

Thursday — BofA reiterated its Buy rating on Qualcomm (QCOM) and lifted its target to $215 from $200. Susquehanna increased its QCOM target to $210 from $200, TD Cowen boosted its target to $205 from $185, and Piper Sandler reset its QCOM target at $200. TD Cowen upped its Bank of America price target to $64 and reiterated its Buy rating, while Eaton shares saw a price target increase at JPMorgan to $440.

Friday — Morgan Stanley trimmed its Dutch Bros (BROS) target to $84 from $86, reiterating its Overweight rating in the process, and named Bank of America shares a fresh Top Pick with a $70 target. JPMorgan upped its target for Labcorp (LH) to $317 from $291.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Tuesday, November 4: How Will the Government Shutdown Impact Holiday Shopping?

Wednesday, November 5: Stocks & Markets Podcast - Why Big Tech Will Continue to Lead With Jay Woods

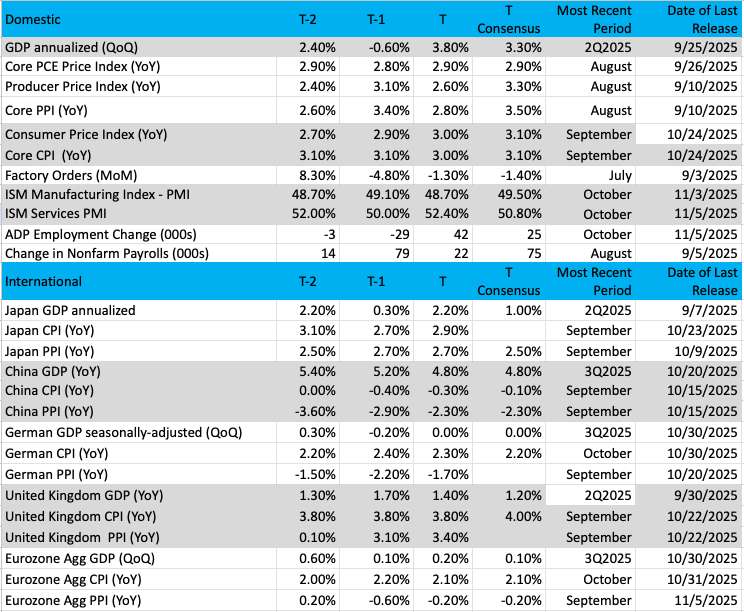

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

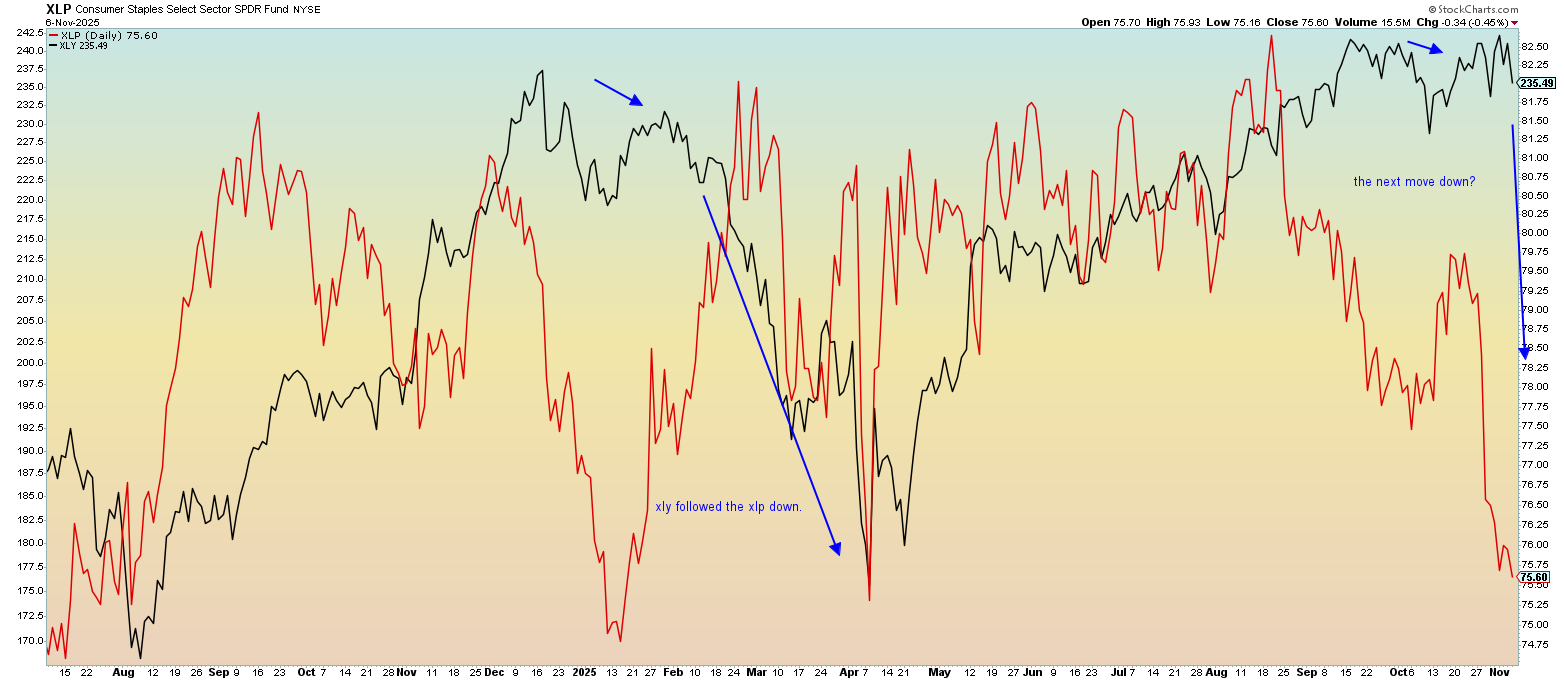

Chart of the Week: Consumer Staples vs. Consumer Discretionary

Let’s look at the difference between two consumer-driven ETFs, the (XLP) and the (XLY) . The XLP is the Consumer Staples Select SPDR Fund, and the XLY is the Consumer Discretionary Select Sector SPDR Fund. Since most names in both ETFs are consumer-related, many like to segregate these by two words: NEED and WANT.

The Staples ETF (XLP) contains names like Walmart (WMT) , Procter & Gamble (PG) , Costco (COST) , Coca-Cola (KO) , and Kimberly-Clark (KMB) . These are your basic needs and necessities in the store that you require on a regular basis. The ETF has performed poorly in 2025.

The Discretionary ETF (XLY) is your mixed bag of wants, not the stuff you need for survival, but rather the items that would make your life better. Names like Amazon (AMZN) , Tesla (TSLA) , Booking Holdings (BKNG) , Starbucks (SBUX) , Nike (NKE) , and Home Depot (HD) are in the XLY. The ETF has performed very well in 2025.

One may wonder if the economy is strong (and it certainly was in the first half of 2025), then why has spending been bifurcated (divided)? One could point to the tariffs as a valid reason, but since the labor market is showing signs of slowing, that too could be a reason. Yet, the XLY (Discretionary) has been thriving. One could point to the strength in Tesla and Amazon; those two mega-caps are mostly driving the performance.

We want to look at these ETFs in comparison to see what is happening at the price level. The daily chart of this comparison looks noisy, but we can see the differences are glaring. There are a few periods when the XLY is weaker than the XLP, but they are not common. Certainly, over the last 15 months, the XLY has been the leader, and looking to the upper right of the chart, that continues to be the case. The dramatic decline in the XLP is concerning, and a bit shocking of late, perhaps illustrating a halt to companies that have put in big price increases.

Whatever the case, we often see Discretionary spending moving towards Staples eventually, and that might signal more pressure on the economy. We’ll see if that happens in 2026.

Other charts we shared with you this week were:

Monday, November 3: S&P 500 - What an 'Inverted Hammer' Might Mean for the Market

Monday, November 3: Palantir (PLTR) - A Close Look at Palantir Ahead of Earnings

Tuesday, November 4: Axon Enterprise (AXON) - There's 'Trouble Brewing' With Axon

Wednesday, November 5: Qualcomm (QCOM) - Is Qualcomm Ready for a Big Move After Earnings?

Thursday, November 6: Trade Desk (TTD) - Troubles for This Bullpen Name Are Far From Over

The Week Ahead

Coming off this week’s October ISM PMI data, ADP’s October Employment Change Report, and other third-party economic data points, the Atlanta Fed’s rolling GDP forecast, better known as its GDPNow model, inched up to 4.0% from 3.9% in mid-October. While that is a positive revision and, on its face, argues against the Fed doing much more this year, let’s be sure not to read too much into it, given the lack of quarter-to-date data. As we’ve discussed several times of late, anecdotal commentary received during the current earnings season points to a different and bifurcated consumer and job market than we would normally see with such a GDP figure.

On Friday, it appeared the current shutdown was likely to enter a seventh week, but nearing the market close, reports indicated Democratic leaders offered a deal to reopen the federal government. The weekend may tell us what’s next for the shutdown, but it will likely hinge on whether Republicans and the White House are willing to swallow a one-year extension of expiring health care subsidies in exchange for Democrat votes on a temporary spending bill. We’ll continue to follow developments and adjust our thinking and Portfolio positioning as needed.

Even if we get a resolution to the shutdown, we still receive just a few pieces of data next week, including the latest NFIB Small Business Optimism Index and ADP’s new weekly Employment Change report. At some point, once the government re-opens and the missing data from September and October is reported, we’ll have a more complete picture of the overall economy. The question is when that will happen, and it would be helpful if it does before the Fed gathers for its December policy meeting.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, November 11

· NFIB Small Business Optimism Index – October (7:00 AM ET)

· ADP Employment Change – Weekly (9:15 AM ET)

Wednesday, November 12

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· CPI – October (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, November 13

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

· Treasury Budget – October (2 PM ET)

Friday, November 14

· Producer Price Index – October (8:30 AM ET)

· Retail Sales – October (8:30 AM ET)

International

Monday, November 10

· China: Inflation Rate - October

· Japan: Leading Economic Index – September

Tuesday, November 11

· Japan: Eco Watchers Survey – October

· UK: Employment Change – September

· Eurozone: ZEW Economic Sentiment Index - November

Wednesday, November 12

· Japan: Machine Tool Orders - October

Thursday, November 13

· Japan: Producer Price Index – October

· UK: Prelim. GDP – Q3 2025

· UK: Industrial Production – September

· Eurozone: Industrial Production - September

Friday, November 14

· China: House Price Index, Industrial Production, Retail Sales, Fixed Asset Investment – October

· Germany: Wholesale Price Index – October

· Eurozone: Prelim, Employment Change – Q3 2025

After back-to-back weeks of multiple Portfolio companies reporting, we catch a breather next week. And even though the overall volume of companies reporting dies down, we will not deviate from the work we’ve been doing. By that we mean poring over earnings reports and conference calls to refresh our thinking as needed and connect those learnings back to the Portfolio.

With that in mind and given the relationship with Nvidia (NVDA) , Microsoft (MSFT) , and SuRo Capital (SSSS) , we will be taking a close look at CoreWeave’s (CRWV) results and look to see if its expected capital spending ramp is tracking. We will also be interested in comments from Surgery Partners (SGRY) about its use and outlook for robotic solutions, given a looming surgeon shortage.

End-market comments from GlobalFoundries (GFS) will be another item we’re following next week. We can say the same about Cisco’s (CSCO) when it comes to networking demand and implications for our positions in Arista Networks (ANET) and Marvell (MRVL) . Comments about consumer spending patterns from Instacart (CART), Treehouse Foods ( (THS) ), and Klarna (KLAR) will also be of interest to us as we get ready for upcoming earnings from TJX Cos. (TJX) on November 19 and Costco (COST) on December 11.

As we collect those items, we’ll also be on the lookout for the October revenue report from Taiwan Semiconductor (TSM) as we get ready for Nvidia’s earnings on November 19 and Marvell's on December 2.

Here's a closer look at the earnings reports coming at us next week:

Monday, November 10

· Open: Ceva (CEVA), Instacart (CART), Monday.com (MNY), Surgery Partners (SGRY), Tree House Foods (THS), Tyson Foods (TSN).

· Close: CoreWeave (CRWV), Paramount Skydance (PSKY).

Tuesday, November 11

· Close: Oklo Inc. (OKLO), StubHub (STUB).

Wednesday, November 12

· Open: GlobalFoundries (GFS), Klarna (KLAR).

· Close: Cisco (CSCO),

Thursday, November 13

· Open: Sally Beauty (SBH), Walt Disney (DIS),

· Close: Applied Materials (AMAT), Beazer Homes (BZH).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Here are some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.