Weekly Roundup: Gaining Ground Despite the Obstacles

Multiple developments on our radar are keeping us prudent but opportunistic.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We entered this week with escalating geopolitical tensions amid the Israel-Iran conflict, and exited it with Iranian Foreign Minister Abbas Araghchi meeting counterparts from the U.K., France, and Germany to discuss what’s being called “nuclear and regional issues” around the ongoing conflict. Friday afternoon reports indicated those conversations yielded hopes of further talks but no indication of any immediate concrete breakthrough. Meanwhile, Israel shows no signs of backing off with reports its Defense Minister Israel Katz instructed the military to continue attacking Iran’s nuclear facilities and to bring about a widespread evacuation of Tehran.

We will continue to monitor developments in the coming days, including the potential role of the U.S., something President Trump is expected to make clear in the next two weeks. We see that timetable giving room for a diplomatic solution, one that we would prefer to see rather than a wider Middle East conflict that would raise uncertainty, likely stall trade deals, and stoke both oil prices and inflationary pressures.

Meanwhile, as expected, the Fed left interest rates unchanged Wednesday exiting its June policy meeting. As we suspected, the central bank’s updated set of economic projections (SEP) continued to pencil in two potential rate cuts this year and dialed back next year’s to one. However, the same SEP update showed expectations for both a slower economy this year and higher inflation expectations compared to the Fed’s December and March SEP forecasts.

Fed Chair Powell explained this as tariff-related inflation “making its way through the system.” The Fed Chair went on to say that:

"It takes some time for tariffs to work their way through the chain of distribution to the end consumer. A good example of that would be goods being sold at retailers today, may have been imported several months ago before tariffs were imposed. So we're beginning to see some effects and we do expect to see more of them overcoming months…"

Taking our cue from that comment as well as our modus operandi of following the data, we’ll be very interested in the inflation commentary contained in Monday’s Flash June PMI data from S&P Global. Should those comments for input and output prices show rising pressures compared to April and May, they would support Powell’s assertion for what’s to come. And because we are not ones to rely on any one single data point, we’ll want to analyze the Price components of ISM’s June Manufacturing and Service PMI reports when they are published on July 1 and July 3, respectively.

The S&P 500 dipped modestly during the shortened trading week, doing little to disrupt its modest gain so far this year. As we’ll discuss in a moment, the Pro Portfolio widened its lead against that market benchmark and its quarter-to-date move moved into the low-double digits.

While we’ll enjoy that move, we recognize we have a long road ahead of us, and that means following the data and remaining prudent investors as we look to position the Pro Portfolio for what’s ahead. That gauntlet includes upcoming June economic data, Israel-Iran developments, Trump trade deals and the July 9 deadline, the start of the June-quarter earnings season, and corporate guidance for the second half of 2025. It’s going to be a busy few weeks, but we’ll be here to guide you through it.

Catching Up on the Portfolio This Week

While it was a shortened trading week, the Pro Portfolio widened its year-to-date lead against the S&P 500, due in part to strong performance from our position in Marvell Technology MRVL. Despite the Wednesday afternoon and Friday pullback in the market that led the S&P 500 to be little changed, MRVL shares closed the week up roughly 10%. Other standout positions that helped the Pro Portfolio move further ahead against the S&P 500 were Eaton ETN, Elastic ESTC, American Express AXP, Bank of America BAC, and Morgan Stanley MS.

As impressive as this week’s move in MRVL is, with six trading days left in the quarter it pales in comparison to far larger ones in Palantir PLTR, Axon Enterprise AXON, Nvidia NVDA, Eaton, and Microsoft MSFT. Indeed, on Friday, we took advantage of that significant rebound in MSFT from its April low and overbought status to lock in a slice of those gains. As we made that move, we upped our MSFT price target to $515 from $480, sharing that we intend to keep a sizable exposure to the shares to capture ongoing AI adoption that should benefit Microsoft’s cloud business in the coming quarters.

In Friday’s video, we noted we are keeping a close watch on Elastic, ServiceNow NOW, and Costco COST with an eye to potentially nibble further. Despite triple witching on Friday, we suspected we could see lower-than-usual trading activity closing out the week given the timing of this year’s Juneteenth holiday on Thursday. If Monday’s Flash June PMI shows another leg up in input and output costs as tariffs, to borrow Fed Chair Powell’s words on Wednesday, “make their way through the system,” we may have an opportunity to make any such moves at better prices than we are seeing Friday. Depending on what we see in the Flash June PMI data, we may want to wait for Powell’s testimony on Tuesday in front of the House Financial Services Committee.

Now let’s see what Wall Street and others had to say about the Pro Portfolio’s holdings over the last few days.

Oppenheimer raised the firm's price target on Amazon AMZN to $250 from $215 and kept an Outperform rating on the shares.

Research firm Moffett Nathanson said Amazon is "chipping away at The Trade Desk's TTD "moat" noting Amazon Ads and Disney (DIS) Advertising have launched an integration between Disney's Real-Time Ad Exchange and Amazon ad platform. This builds on reports we’ve shared previously about Amazon taking share from The Trade Desk.

First Shanghai Securities upgraded Apple AAPL shares to Buy from Hold with a $230 target.

Labcorp LH launched Labcorp Whole Health Solutions, a comprehensive testing initiative designed to support functional, integrative, and primary care providers in delivering holistic, personalized care. The program introduces specialized test panels and a curated menu of over 1,000 scientifically validated biomarkers targeting cardiometabolic health, hormones, micronutrients, longevity, and full-body wellness. We view this as another foot forward in expanding its higher-margin Diagnostic Services segment. Like several others in the Portfolio, LH shares have been a strong performer and could be ripe for the picking as they approach our $265 target.

B. Riley raised its Marvell target to $115 from $110 and reiterated its Buy rating. BofA also boosted its MRVL target to $90 from $80 and kept its Buy rating.

Reports indicate Meta META will expand its smart glasses lineup as launches products with EssilorLuxottica ESLOY under the Oakley and Prada brands. This adds another layer of support for the IoT market, one that we are participating in not only with META but Qualcomm QCOM as well. Early this week, Oppenheimer boosted its META target to $775 from $665 citing a stronger-than-feared advertising market. We discussed Meta’s plans to monetize its WhatsApp platform, sharing that could be a catalyst for us to revisit our META target.

Citi upped its Morgan Stanley price target to $130 from $125 following the rebound in capital markets activity, but it also likes the “steady engine” that is Morgan’s wealth management business. We agree on both counts.

Barclays lifted its price target for Nvidia to $200 from $170, and as we explained on Tuesday, we’ll revisit our NVDA target once we have June revenue reports from Taiwan Semiconductor TSM and Foxconn in hand.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, June 16: Our Take on the Holdings Making Big News Today

Tuesday, June 17: Wall Street Lifts Nvidia Price Target

Friday, June 20: 3 Stocks on Our Shopping List

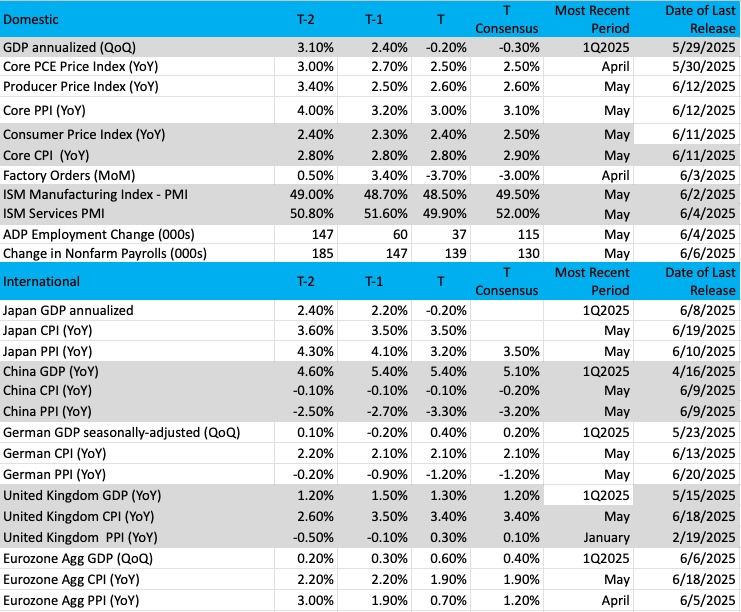

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: iShares TIPS Bond ETF (TIP)

This week the Federal Reserve left interest rates alone for the fourth time in 2025. They continue to work towards slaying the "inflation dragon" once and for all, and believe this is the appropriate monetary policy for where the economy is at right now. The committee continues to monitor the data, which will be the main driver of policy moves going forward.

While Chair Powell did admit the data has been favorable on inflation, the committee remains concerned price pressures may start to arise from tariffs levied. Historically, this has resulted in some sharp increases in inflation that have spiraled out of control, but today most economists believe any inflation would be short-lived and eventually controlled.

The Fed won’t be complacent, however, and will look for several prints of data to make sure inflation fires are under control and that inflation expectations are anchored. In the Fed's statement this week, the committee believes two rate cuts will be coming in 2025, and one in 2026. That is mostly in line with the Fed Funds futures market.

We can view how inflation is operating through the lens of a stock chart. We’ll use the iShares TIPS Bond ETF TIP to see how the market is viewing inflation from a risk standpoint.

What is the TIP and how can it be used by investors? Tracking inflation, TIP is an ETF that rises when inflation rises and "protects" U.S. government bonds that get cheaper when inflation rises. In other words, protecting the investor from rising prices that can spiral out of control. Investing in TIP alongside your bond portfolio is a smart way to protect yourself from inflation.

Now, why would you need this protection if the Federal Reserve is already protecting you with higher interest rates (trying to bring inflation down)? Good question! Because the Fed is not the market and is only one piece of the puzzle. Markets and the Fed often see eye to eye but at times there is a difference of opinion. When TIP is rising it means inflation concerns are high.

The chart of the TIP is mildly bullish, with a series of higher highs and higher lows. Recent bullish trends in U.S. Treasury bonds have been snuffed out by bond sellers not wanting the exposure to inflation risk. We see that happening in the TIP, which is sporting good relative strength and a bullish MACD (moving average convergence/divergence) crossover.

Keep a close eye on this ETF. As we heard this week, the Fed’s work on inflation is not over, but if the TIP starts to roll over that might be a sign that rate cuts could soon follow. But if it continues higher, we may have some inflation down the road.

Other charts we shared with you this week were:

Monday, June 16: S&P 500 - How Long Can an Overbought Condition Last?

Monday, June 16: Eaton (ETN) - Is This Holding Base-Building Before a Run at All-Time Highs?

Tuesday, June 17: Vulcan Materials (VMC) - A Holding Finds Itself in No-Man's Land

Wednesday, June 18: Microsoft (MSFT) - This 'Freight Train' Is at the Top of an Elite Class

The Week Ahead

We hit the ground running on Monday with what, in our view, could be a very telling set of data. We’re referring to the Flash June PMI report from S&P Global, which, as Fed Chair Powell discussed this week, could show the impact of tariffs working their way through the system. In addition to seeing what that report shows on the inflation front, we’ll be assessing its findings on job creation and what new orders say about the pace of the economy entering Q3 2025.

Amid a few other pieces of May data, the other economic data point we’ll be focused on next week is the Personal Income & Spending report. With that, we’ll be doing a deeper dive into spending on services during the month following this week’s May Retail Sales report. We’ll also compare the wage data found in the May Employment Report against the various Personal Income data line items.

We expect many will focus on the May Personal Consumption Expenditure (PCE) price index, in part because it is a favorite of the Fed’s. However, given the expectation expressed by Powell about inflation rising over the summer months, we’ll place a greater emphasis on Monday’s June Flash PMI.

We are likely to hear Powell reiterate those “inflation through the system” and summer increase expectations on Tuesday when he testifies before the House Financial Services Committee. Before and after Powell’s testimony we have multiple Fed speakers making the rounds. We’ll be interested to see how many of them share the view expressed by Fed Governor Waller on Friday about the potential for a July rate cut.

We have heard rumblings that that "cut-friendly tone" could be Waller jockeying to replace Powell as Fed Chair next year. While that may be a possibility, we’ll be better served by following the data as that is what will drive the committee that determines Fed policy. Friday afternoon Atlanta Fed President Thomas Barkin commented that there's no rush to cut interest rates given the still-unresolved risk that new import taxes might raise inflation, and with the U.S. job market and consumer spending holding up. We’ll have more to say on this after Monday’s Flash June PMI report.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, June 23

· S&P Global Flash PMI – June (9:45 AM ET)

· Existing Home Sales – May (10:00 AM ET)

Tuesday, June 24

· FHFA Housing Price Index – April (9:00 AM ET)

· S&P Case-Shiller Home Price Index – April (9:00 AM ET)

· Consumer Confidence – June (10:00 AM ET)

Wednesday, June 25

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· New Home Sales – May (10:00) AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, June 26

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· International Trade, Retail & Wholesale Inventories (Advanced) – May (8:30 AM ET)

· Durable Orders – May (8:30 AM ET)

· GDP (3rd estimate) – Q1 2025 (8:30 AM ET)

· Corporate Profits (Final) – Q1 2025 (8:30 AM ET)

· Pending Home Sales – May (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, June 27

· Personal Income & Spending – May (8:30 AM ET)

· PCE Price Index – May (8:30 AM ET)

· University of Michigan Consumer Sentiment (Final) – June (10:00 AM ET)

International

Monday, June 23

· Japan: Jibun Bank Flash PMI – June

· Eurozone: HCOB Flash PMI – June

· UK: S&P Global Flash PMI – June

Tuesday, June 24

· Germany: Ifo Business Climate and Conditions - June

Wednesday, June 25

· Eurozone: New Car Registrations – May

· Japan: Leading Economic Index (Final) - May

Thursday, June 26

· Germany: GfK Consumer Confidence - July

Friday, June 27

· Japan: Tokyo CPI, Retail Sales, Housing Starts – May

· China: Industrial Profits – May

· UK: GDP Growth Rate (Final) – Q1 2025

· Eurozone: Economic & Consumer Sentiment - June

Following this week’s Marvell MRVL event, which led to multiple price target increases across Wall Street, next week we have Waste Management’s WM 2025 Investor Day. During that event, we expect to hear about productivity efforts as the company continues to roll out automated trucks across its residential footprint. We will be interested in the discussion around its Stericycle acquisition, how management plans to drive those margins higher, and how the business will serve as a launchpad for other acquisitions. Based on what we learn, we’ll revisit our WM price target as needed.

We’ll also be interested in what data center real estate investment trust (REIT) company Equinix EQIX says about AI adoption and capital spending plans during its 2025 Analyst Day on June 25. That same day, Nvidia NVDA conducts its annual shareholder meeting, and we’ll be on the lookout for any incremental comments about chipset demand.

As we move through the last few trading days of the current quarter, comments and guidance from FedEx FDX, Micron MU, and Nike NKE about demand patterns, inflation, and consumer spending will be worth noting. We’ll also be interested in what Jefferies JEF says about its investment banking pipeline and its timetable given that IPO activity tends to slow as we enter the summer doldrums.

Here's a closer look at the earnings reports coming at us next week:

Monday, June 23

· Close: KB Home (KBH)

Tuesday, June 24

· Open: Carnival (CCL)

· Close: Blackberry (BB), FedEx (FDX)

Wednesday, June 25

· Open: General Mills (GIS), Paychex (PAYX), Winnebago (WGO)

· Close: Jefferies (JEF), Micron (MU)

Thursday, June 26

· Open: McCormick & Co. (MKC), Walgreens Boots Alliance (WBA)

· Close: Nike (NKE)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.