Weekly Roundup: Friday’s Selloff Pulls the Rug Out From the Market

We booked another big winner this week, and have plans to put those gains to work near-term.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market looked to continue its recent string of gains this week, but developments on Thursday night and Friday led the S&P 500 and Nasdaq Composite to give back gains from earlier in the week.

Recapping the week, Monday and Tuesday were largely wait-and-see days ahead of the Fed’s policy decision and updated set of economic projections. On Wednesday, the Fed delivered the expected 25-basis point rate cut the market was looking for, but maintained just one 25-basis point rate for next year in its updated set of economic projections. However, it was Fed Chair Powell’s more dovish than expected comments that led the market to power higher, with Powell indicating a boatload of fresh economic data next week could alter the Fed’s monetary policy plans.

The rate cut was notable for having three dissents — the most since September 2019. In The Week Ahead section below, we talk more about that upcoming data and how it could alter rate-cut expectations.

Thursday, the market rally continued and broadened as financials and other sectors helped lead the S&P 500 to a fresh record close at 6901. However, tech stocks were under pressure, weighing on the Nasdaq Composite, due to weaker-than-expected quarterly results, concerns over margin pressure, and a big step up in capex at Oracle (ORCL) . Those three items overshadowed the $35 billion rise in the company’s remaining performance obligations (RPOs) to $455 billion, rekindling concerns some have about AI spending.

We saw a similar development Thursday night and Friday with quarterly results from Broadcom (AVGO) . While the company said its backlog swelled to levels that granted significant visibility over the coming quarters, it was CFO Kirsten Spears' comment about margins that hit AVGO shares on Friday. During the earnings call, Spears shared expectations for Broadcom’s gross margin to fall 100 basis points sequentially as AI revenue becomes a larger part of the overall mix. Lingering concerns from Oracle’s results and a report that some of its expected data centers had been pushed back added to the Friday drop in AVGO shares, leading the S&P 500 and Nasdaq Composite to shed the week’s gains.

Despite the pressure brought about by Oracle-related concerns, our "North Star" for AI will be adoption and usage levels. During the week, we discussed the favorable findings from OpenAI on enterprise adoption. On Thursday, we explained why a deal between Walt Disney (DIS) and OpenAI has the potential to drive consumer AI adoption, and also why the video aspect of that agreement could pressure digital networks and infrastructure in a big way.

Based on developments we’ve seen before, especially with video adoption, and the robust backlog levels at Marvell Technology (MRVL) , Broadcom, and others, we remain bullish. We recognize others may need to catch up to our thinking on adoption and usage, especially when it comes to the implications of AI-generated video, but we can be patient so long as the incoming data are supportive.

Heading into the weekend, the Nasdaq Composite is ~0.5% away from its 50-day moving average, while the S&P 500 is roughly 1% away from its corresponding level. As we digest next week’s economic data and assess its implications, we’ll keep a close watch on those support levels.

Enjoy your weekend, Saturday’s Signals Alert, and Sunday’s bowl of "soup." See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

Friday’s selloff pulled the rug out, not only from the gains the stock market was tracking for this week, but also those for the Pro Portfolio. Still, despite the renewed pressure on Marvell (MRVL) shares following quarterly results from Oracle (ORCL) and Broadcom (AVGO) , and the sharp move lower in Welltower (WELL) , the Portfolio outperformed the S&P 500 on a relative basis. That allowed it to make additional progress, narrowing the gap on a year-to-date basis.

Enabling that were the positive week-over-week moves registered across just over half of our holdings. Notable positive moves were those by Axon Enterprise (AXON) , Dutch Bros (BROS) , Labcorp (LH) , Qualcomm (QCOM) , United Rentals (URI) , Waste Management (WM) , Morgan Stanley (MS) , American Express (AXP) , and Bank of America (BAC) .

Looking at the basket of holdings that power our EPS Diplomats strategy, Friday's selloff took its toll across the basket. However, gains over the last 20 days in Barrick Gold (B) , Kinross Gold (KGC) , and SeaGate Technology (STX) leave the basket’s return up more than 5% since we implemented the strategy. By comparison, the S&P 500 is up ~1.5% over the same time frame.

On the dividend front, this week we credited the Pro Portfolio’s cash position with the latest $0.72 per share quarterly payment from Labcorp. Exiting the week, after locking in an almost 112% gain on a slug of Morgan Stanley shares on Tuesday and adding a few more Marvell shares following CEO Matt Murphy coming out swinging Tuesday night, our cash position stood at roughly 7.5% of the Portfolio’s assets. On Thursday, we noted that we have a close eye on Welltower shares following their recent decline, and the technical levels that could spur us into action, potentially as early as next week.

In Friday’s video, we discussed a potential move we are considering for the Portfolio’s current chip exposure, should we decide over the weekend to make some room for Broadcom (AVGO) in that mix. One factor that could tip our decision, in addition to the $73 billion AI backlog expected to be delivered over the next 18 months, is whether AVGO shares hold support at the 50-day moving average. That level for AVGO shares is $362.06. Should we make this move, the goal would be to improve our chip exposure as AI adoption and usage growth accelerate, especially when it comes to video usage.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday: Wedbush upped its Apple (AAPL) price target to $350 from $330, and we provide our take on the rationale behind that move.

Tuesday: RBC named Dutch Bros shares a “favorite 2026 idea,” reiterating the firm's Buy rating and $80 target. Citi boosted its Apple target to $330 from $315 as it sees better than previously expected iPhone demand. Wolfe Research upgraded Eaton (ETN) shares to Outperform from Peer Perform with a $413 target.

Wednesday: TD Cowen reiterated its Buy rating on Amazon (AMZN) shares as well as its $300 price target. Guggenheim initiated coverage of Amazon with a Buy rating and $300 price target and also started TJX Companies (TJX) shares with a Buy rating and a $175 target.

Thursday: Piper Sandler raised its Bank of America target to $56 from $55 and took its Alphabet (GOOGL) target to $365 from $330.

Friday: TD Cowen upped its Alphabet target to $350 from $335 following what it saw in its proprietary U.S. survey data that pointed to ramping Gemini usage. JPMorgan, however, upped its GOOGL target to $385 from $340. Bernstein raised its Costco (COST) target to $1,146 from $1,134 while BMO Capital reiterated the shares as a “core holding” as well as its $1,175 target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, December 8: Apple Defections Could Be an Opportunity for This Holding

Tuesday, December 9: Explaining Surprise Reaction to Trump's Nvidia Decision

Wednesday, December 10: Stocks & Markets Podcast: Getting Ready for 2026 With Freedom Capital

Friday, December 12: Why We Might Adjust the Portfolio After Broadcom Selloff

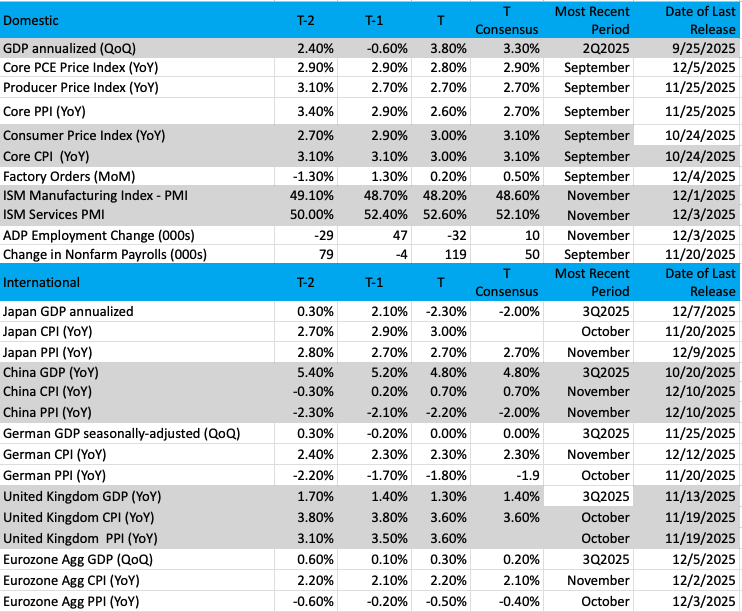

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

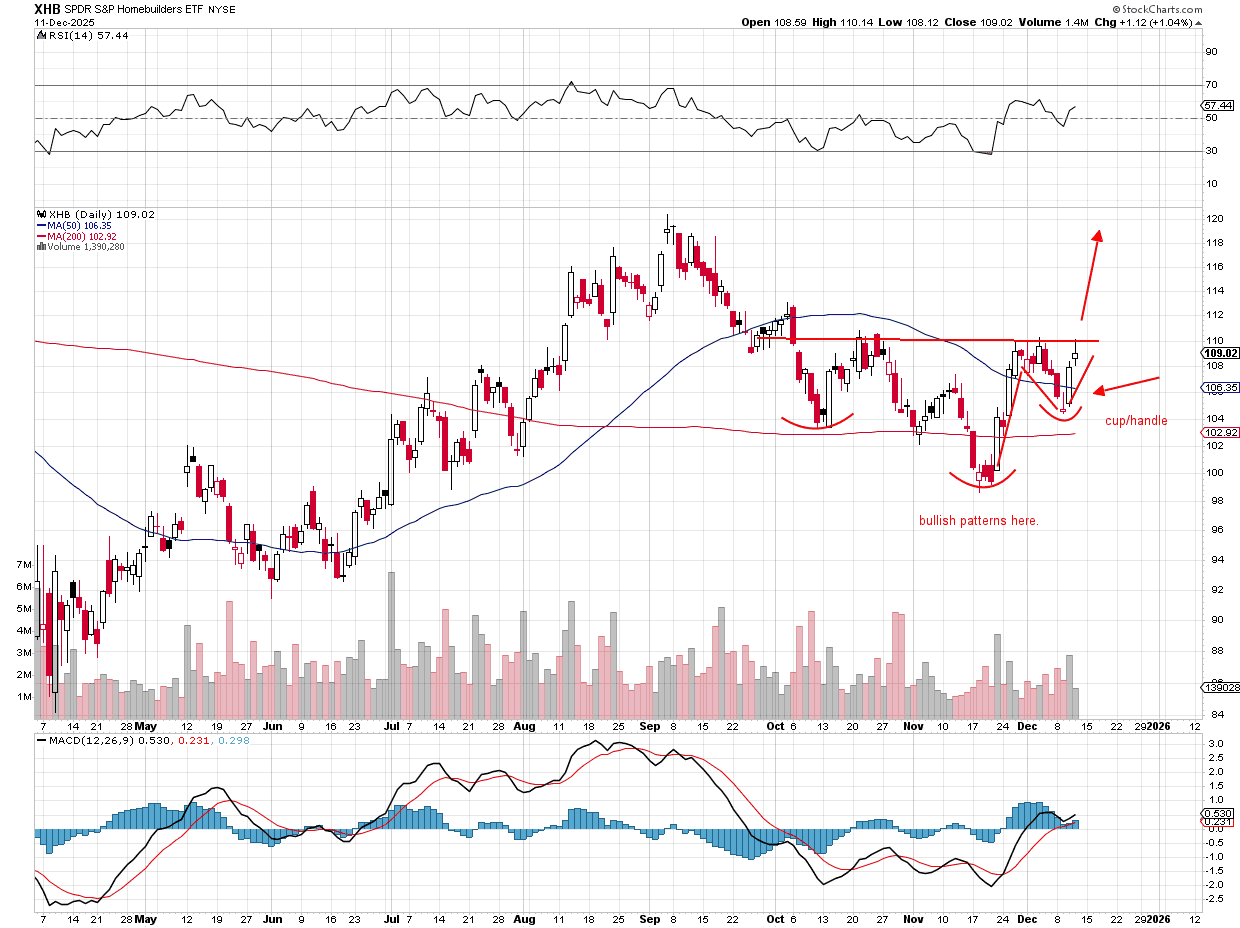

Chart of the Week: SPDR S&P Homebuilders ETF

A bullish pattern has emerged in the SPDR S&P Homebuilders ETF (XHB) that is just impossible to ignore.

There is no better pattern to follow than cup/handle (strong right-side base followed by a consolidation) or the inverse head/shoulders, where the price tests two levels (shoulders) and a drop below in between (head), which signals strong support at two or more levels.

The XHB is the key indicator of homebuilder health. When this ETF is strong, it tells us much about the economy: jobs are plentiful, wages are strong, inflation is under control, and home ownership is growing. Along with homebuilders, we often see additional strength in the banks, financials, and commodity-related companies and several other sectors (like retail). So, the reach from homebuilders is vast, and if the chart has budding strength as it shows right now, then there are several more opportunities to gain.

But back to the XHB, which shows good relative strength but is not overbought here. The MACD is on a strong buy signal while the ETF is comfortably above the 50-day and 200 moving averages. There is some resistance on the chart at $110, but once that is exceeded, there is little in the way for the ETF to make a run at those September highs at the $120 level.

Strong volume trends are always the hallmark of a good run higher in the XHB. We are starting to see that right now. This could be one of the better performers in 2026.

Other charts we shared with you this week were:

Monday, December 8: S&P 500 - S&P 500 Is Right at the Top of a Wide Range

Monday, December 8: Comfort Systems USA (FIX) - This 'Diplomat' Is Getting a Big Promotion

Tuesday, December 9: First Trust Nasdaq Cybersecurity ETF (CIBR) - One Name May Move the Cybersecurity Group This Week

Wednesday, December 10: Costco (COST) - Is This Another Great Costco Buy Opportunity?

Thursday, December 11: Welltower (WELL) - Welltower Offers Bulls a Good Opportunity

The Week Ahead

Following the Fed’s more dovish than expected policy meeting this week, and as Fed Chair Powell alluded to, we have a bonanza of October and November economic data coming next week. Given the dearth of data since the government shutdown began and ended, we’ve tapped into the published data received from the likes of ADP, ISM, S&P Global, Mastercard, Visa, and others to get a handle on the vector and velocity of the economy.

As we get ready for that swath of data, we still see a wide variance between the Atlanta Fed’s GDPNow Model, at 3.6% for the current quarter, and the New York Fed Nowcast model at 1.8%. The Cleveland Fed Inflation Nowcasting model sees year-over-year core CPI figures between 2.95%-2.99% for October, November, and December. The same source calls for core PCE figures to rise from 2.76% on a year-over-year basis in October to 2.93% in December.

We expect many will be going over the October and November jobs data carefully, given Powell’s comments on Wednesday afternoon that the Fed is more attuned to downside risks for the job market. We will too, but we’ll also be paying close attention to revised figures for earlier months as well. Should the data confirm the softening job market picture seen in data published by ADP, ISM, and S&P, the market is likely to warm up to the idea that the Fed could do more than one rate cut it telegraphed for 2026. In other words, bad news for the economy would be good news for rate cuts and the market.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, December 15

Empire State Manufacturing Index – December (8:30 AM ET)

NAHB Housing Market Index – December (10:00 AM ET)

Tuesday, December 16

ADP Employment Report Weekly Change (8:15 AM ET)

Employment Report – November (8:30 AM ET)

Housing Starts & Building Permits – November (8:30 AM ET)

Retail Sales - October (8:30 AM ET)

Industrial Production & Capacity Utilization – November (9:15 AM ET)

S&P Global Flash Manufacturing & Services PMI – December (9:45 AM ET)

Business Inventories – September (10:00 AM ET)

Wednesday, December 17

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Retail Sales – November (8:30 AM ET)

Business Inventories – October (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, December 18

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Consumer Price Index – November (8:30 AM ET)

Philly Fed Index – December (8:30 AM ET)

Leading Indicators – November (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, December 19

Personal Income & Spending – November (8:30 AM ET)

PCE Price Index – November (8:30 AM ET)

Existing Home Sales – November (10:00 AM ET)

University of Michigan Consumer Sentiment Index (Final) – December (10:00 AM ET)

International

Monday, December 15

· China: Industrial Production, Retail Sales – November

Germany: Wholesale Price Index - November

Tuesday, December 16

Japan: S&P Global Flash Manufacturing & Services PMI – December

Eurozone: HCOB Flash Manufacturing & Services PMI – December

UK: S&P Global Flash Manufacturing & Services PMI - December

Eurozone: ZEW Economic Sentiment Index - December

Wednesday, December 17

UK: Inflation Rate – November

Germany: Ifo Expectations Index – December

Eurozone: Inflation Rate and Consumer Price Index - November

Thursday, December 18

UK: Bank of England Interest Rate Decision

Eurozone: European Central Bank Interest Rate Decision

Friday, December 19

Japan: Inflation Rate – November

UK: Retail Sales – November

Eurozone: Consumer Confidence (Flash) - December

While the main focus will be on next week’s economic data, we still have some companies reporting their quarterly results. These include Micron (MU) , and we’ll be following what it says about AI and data center, as well as smartphone and PC demand. That goes for the current quarter, but also any initial indications about 2026.

Following disappointing guidance from Lululemon (LULU) , and weak results from J. Jill (JILL) and Vera Bradley (VRA) , next up on the consumer apparel front is Nike (NKE) . NKE shares are still down quite a bit from their September high, despite the rebound seen in the last several weeks. Comments about consumer spending patterns, tariffs, and currency will be top of mind when we read through the results and updated guidance.

We’ll also be following comments about the use of incentives and discounts when homebuilders Lennar (LEN) and KB Home (KBH) report. We’ll be interested to see what they say about the cumulative rate cuts delivered by the Fed since September, as well as if they admit the weakening jobs market could be a headwind. And with the final throes of the holiday shopping season just a few weeks away, we’ll be curious to see how FedEx (FDX) sees digital shopping closing out the year. We’ll also be interested in its comments about the larger economy and what it sees for 2026.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, December 11

Close: Lennar (LEN)

Wednesday, December 12

Open: General Mills (GIS)

Close: Micron (MU)

Thursday, December 13

Open: CarMax (KMX), Cintas (CTAS), Darden Restaurants (DRI)

Close: Blackberry (BB), FedEx (FDX), KB Home (KBH), Nike (NKE)

Friday, December 14

· Open: ConAgra (CAG), Lamb Weston (LW)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.