Weekly Roundup: Following the Data Pays Off for the Portfolio

We locked in big gains on two positions, added to another and are 'soft circling' these two others.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Connecting the dots

Connecting the dots

Following a challenging March, one that led all the major indexes to close the first quarter of 2026 in the red, a two-week ceasefire between the U.S. and Iran has powered a recovery in the market. The S&P 500 rebounded more than 3% this week, while the Nasdaq Composite clawed back around 4%. Meanwhile, the Volatility index plummeted from around 31 in late March to close the week out below 20.

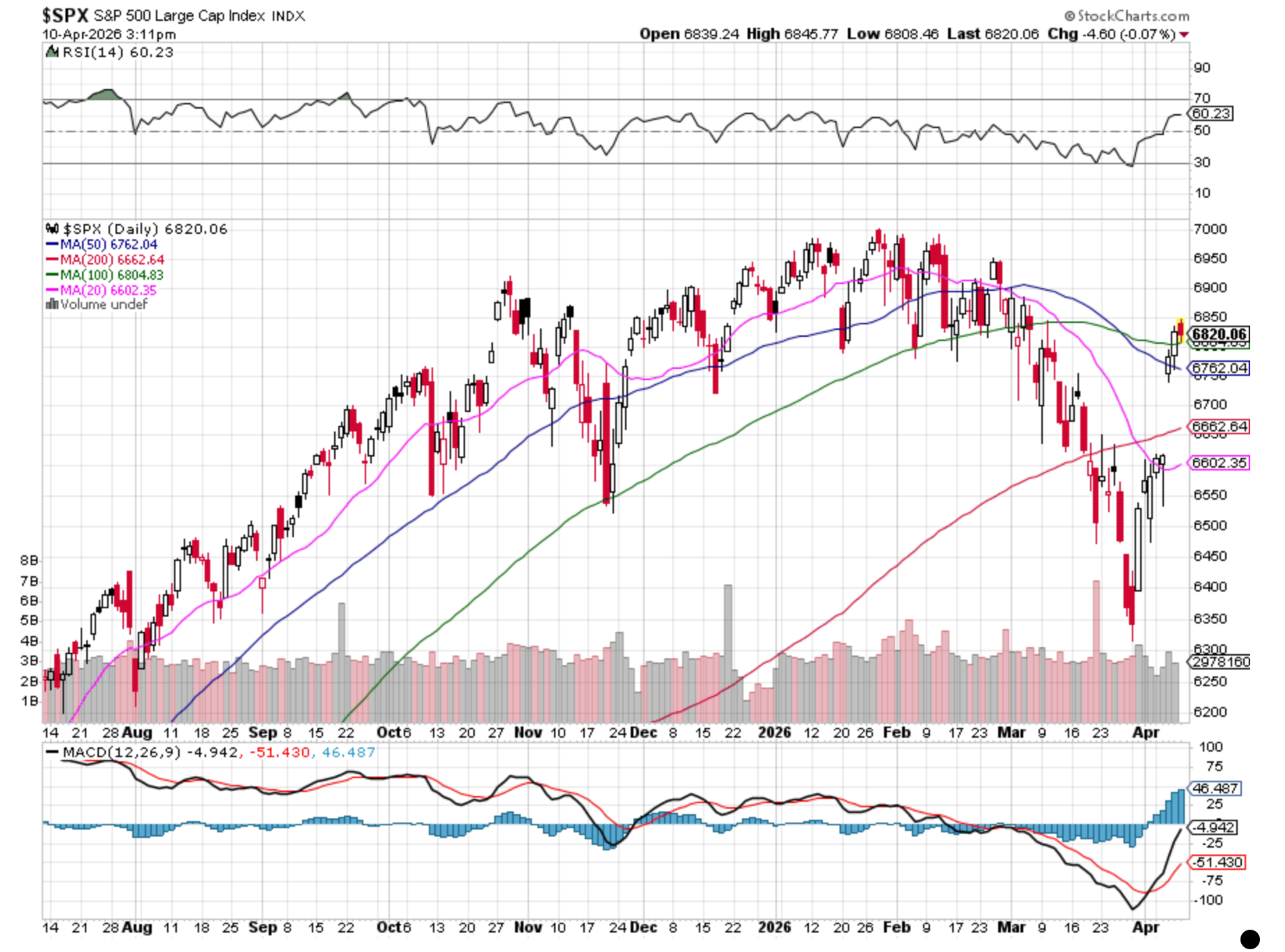

In the chart below, we can see the S&P 500 pushed past key resistance levels, and now we are watching to see where support for the index lands. Some may chalk up the recent market surge to a relief rally, but as the trading week comes to a close, the continued closure of the Strait of Hormuz and fighting between Israel and Hezbollah in Lebanon threaten to complicate U.S.-Iran negotiations over the weekend.

There are other concerns as well. Recent below-consensus guidance from Delta Air Lines (DAL) and Friday’s EPS estimate cuts to Procter & Gamble (PG) from Bank of America, reflecting higher jet fuel, packing and input costs, call into question the continued climb in consensus S&P 500 EPS estimates over the last several weeks. And let’s not forget the reminder from RH (RH) about Q1 2026 winter weather and the impact of tariffs.

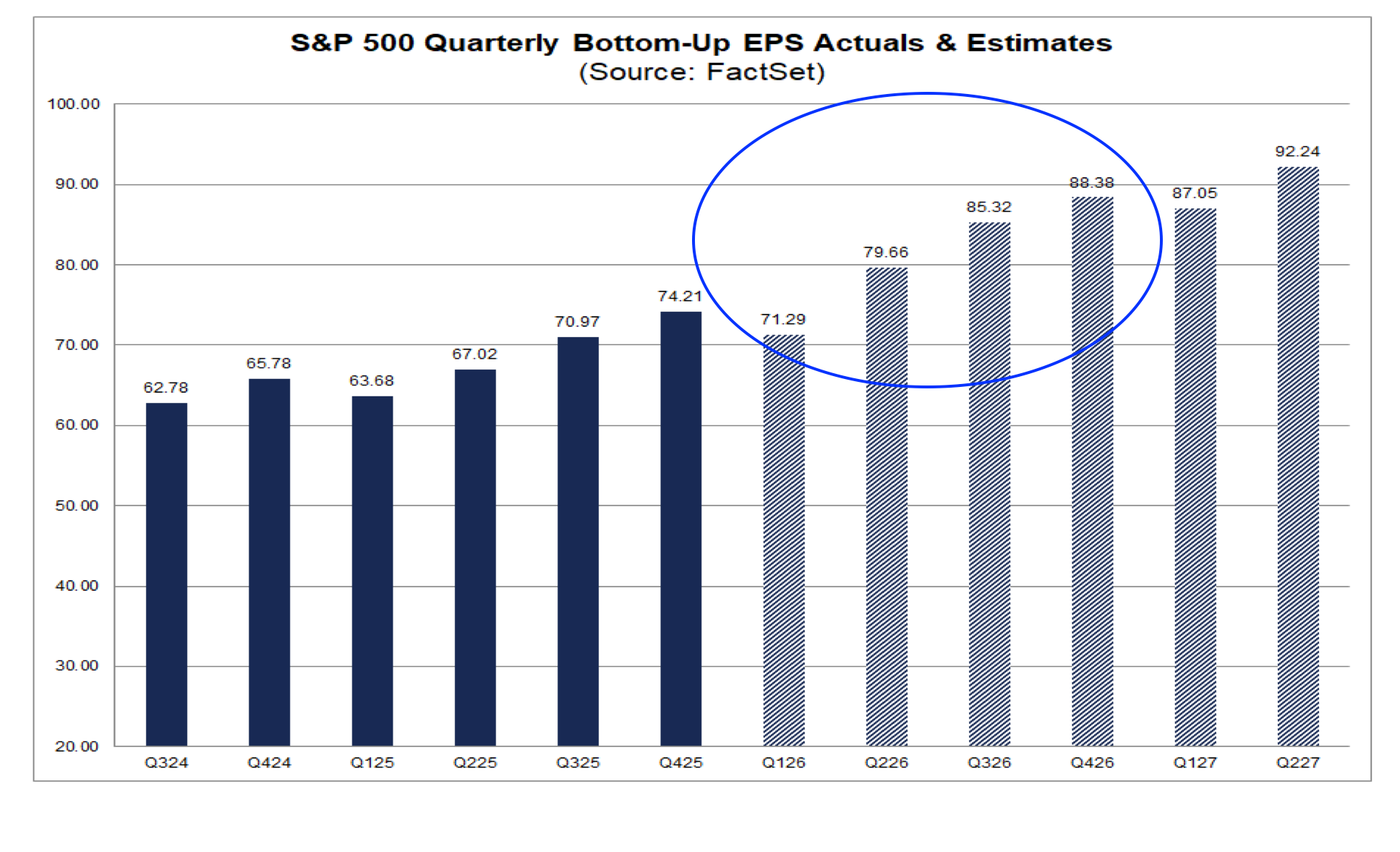

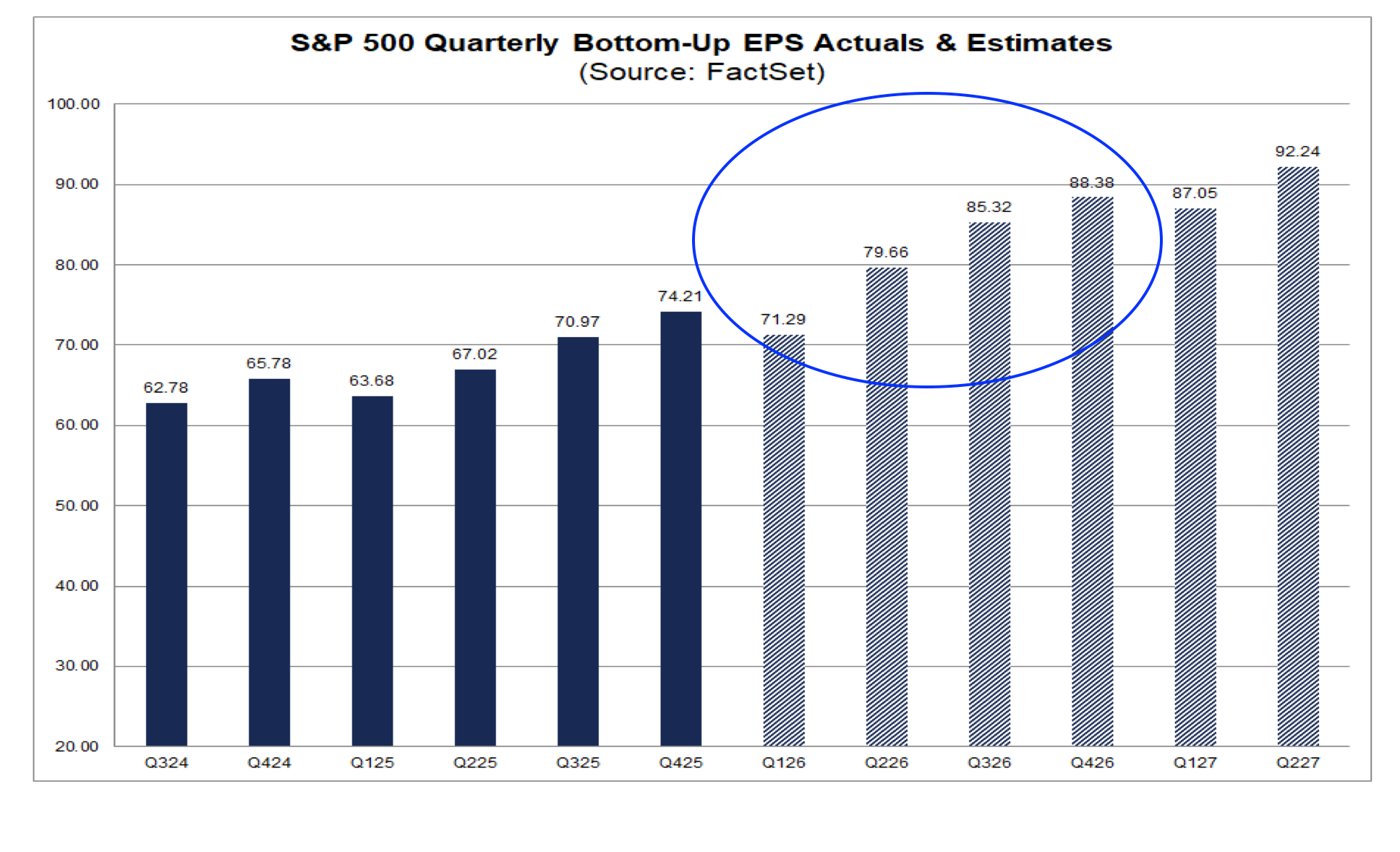

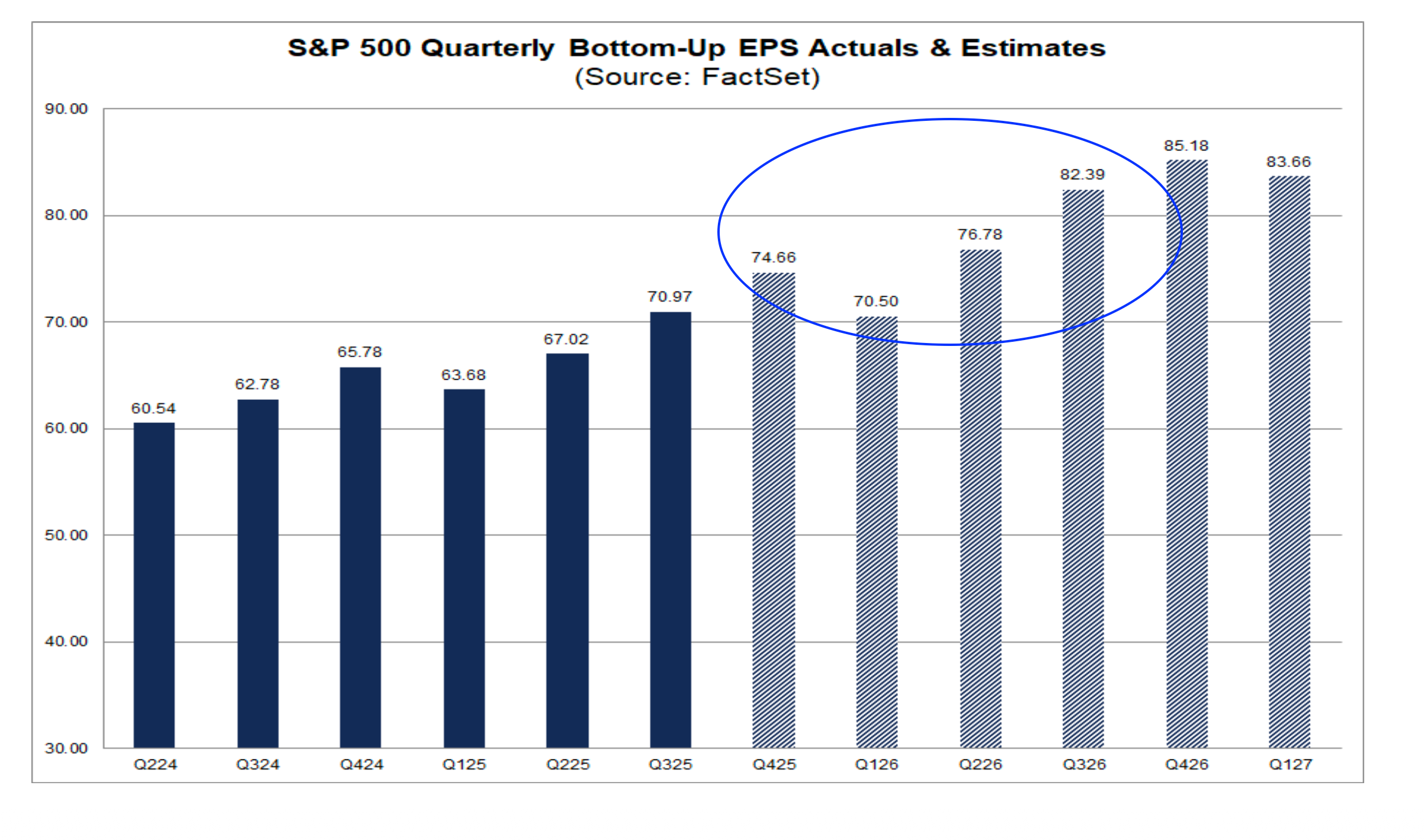

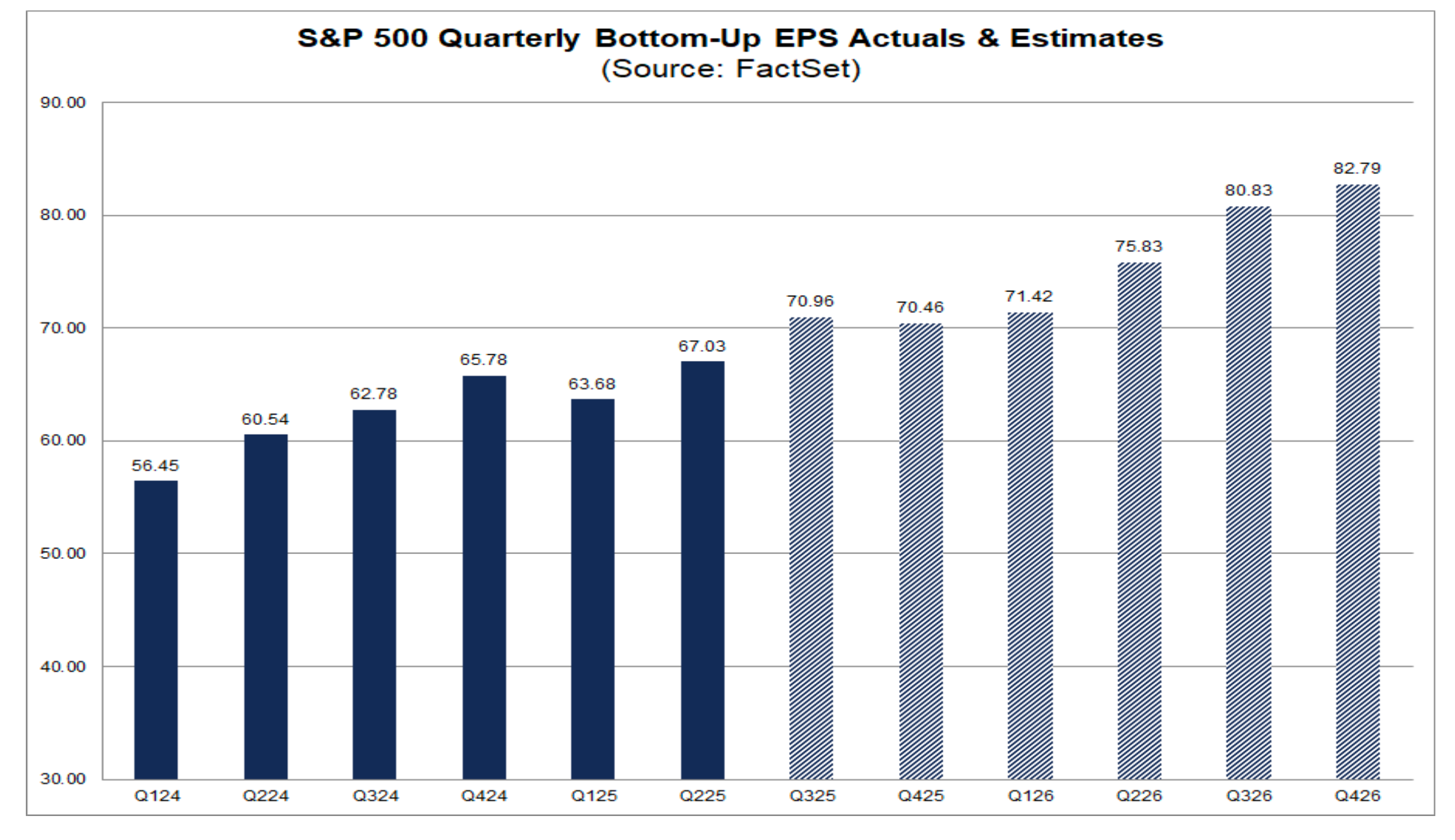

We’ll get into the quarterly nitty gritty or S&P 500 EPS expectations later in this Roundup, but the 2026 consensus EPS forecast for the S&P 500 now calls for… wait for it… nearly 19% growth compared to 2025. Based on reduced GDP expectations for the current quarter, the growing potential for margin pressures, and a Fed that will likely remain in a holding pattern for some time, we could see the market face renewed headwinds as we move through April and those expectations are reset.

As we navigate this and keep our inverse ETF positions in play, we’ll continue to focus on the incoming data and signals as our North Star for the Pro Portfolio. While things were challenging for us in late March, recent news from Taiwan Semiconductor (TSM) , Applied Digital (APLD), Lumentum (LITE), Foxconn, and others validated our investment rationale for multiple holdings, and propelled them higher. We’ll continue to do our best to block out the noise and tamp down emotions to keep laser-focused on what the data are telling us.

And if we need to bow to our portfolio discipline as we did on Friday, we will. We’ll also continue to look for opportunities to adjust the Portfolio’s position when and where it makes sense.

Enjoy your weekend, and Saturday’s Signals alert. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio outpaced the S&P 500 this week, and it is now outperforming that industry benchmark on a year-to-date basis. This week's move up was fueled by double-digit gains in Applied Materials (AMAT) , Amazon (AMZN) , Arista Networks (ANET) , Broadcom (AVGO) , Eaton (ETN) , Marvell (MRVL) , and SuRo Capital (SSSS) . While those were the highlights, other positions, including American Express (AXP) , Bank of America (BAC) , and Alphabet (GOOGL) . to name a few, also bested the S&P 500 rise this week. Those gains were mitigated by declines in Axon (AXON) , Palantir (PLTR) , Labcorp (LH) and the First Trust Cybersecurity ETF (CIBR) .

Our recently reconstituted and upsized exposure to the EPS Diplomats strategy was also a positive force for the Portfolio, as its April-to-date gain pushed into the mid-teens this week. That performance has been fueled by sizable moves higher so far in nearly all of the basket's constituents, save for Eldorado Gold (EGO) and Rocket Companies (RKT) .

One question we’re likely to get is about the Portfolio’s market-hedging positions, which were a drag on performance this week. It’s true, they declined as the U.S.-Iran ceasefire lifted the market. However, as we discuss in "The Week Ahead" below and touched on in Friday’s video, the market remains amiss with the spread of consensus quarterly EPS expectations for the S&P 500. Slowly but surely, though, some on Wall Street are coming around to realizing the impact the war, as well as the step up in inflation pressures ahead of the conflict, will have on margins and bottom-line performance. Recognizing this disconnect, we’ll keep these ETFs in play as we move deeper into the Q1 2026 earnings season.

On Friday, we took advantage of the upswell in Marvell and SuRo Capital shares, as both entered an overbought condition based on their respective RSI levels. The average gain we booked on that tranche of MRVL shares topped 80%, as did our gain on that slug of SSSS shares. Those trades lifted the Portfolio’s cash position, and as we discussed in Friday’s video, the renewed pressure on Palantir (PLTR) and Axon (AXON) has us following both of those names closely even after we accumulated additional AXON shares earlier in the week.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday: CIBC inched up its Waste Management (WM) price target by $2 to $244. Goldman Sachs lifted its Morgan Stanley (MS) target to $186 from $172 and upgraded Netflix (NFLX) shares to Buy with a new $120 target.

Tuesday: Rosenblatt Securities upgraded Arista Networks (ANET) to a Buy and lifted its price target to $180 from $165. BofA added Microsoft (MSFT) shares to its US 1 List.

Wednesday: BofA reiterated its Buy rating and $885 target for Meta (META) . Evercore ISI lifted its Labcorp (LH) target to $300 from $280.

Thursday: William Blair added Amazon (AMZN) to its Conviction List and reiterated its Outperform rating. Telsey Advisory increased its Costco (COST) target by $10 to $1,135. Susquehanna reset its Applied Materials (AMAT) target at $500, up from $435. BTIG raised its SuRo Capital (SSSS) target to $15, as did Citizens. Morgan Stanley re-started coverage of Netflix with an Overweight rating, matching our $115 target.

Friday: BNP Paribas lowered its Microsoft (MSFT) target to $556 from $659. RBC slimmed down its American Express (AXP) target to $415 from $425, but JPMorgan boosted its Waste Management (WM) target to $270.

This Week's Portfolio Videos

We cover a lot of ground during the week in our daily videos. If you happened to miss one or more of them, here are some helpful links:

Monday, April 6: Our Outlook on Big Bank Earnings With Markets in Wait-and-See Mode

Tuesday, April 7: As Iran Deadline Nears, Watch This Key Level for the S&P 500

Wednesday, April 8: Uranium, SMRs, and Eagle Nuclear Energy's Opportunity

Friday, April 10: We're Bullish on These 2 Holdings Despite Pressure

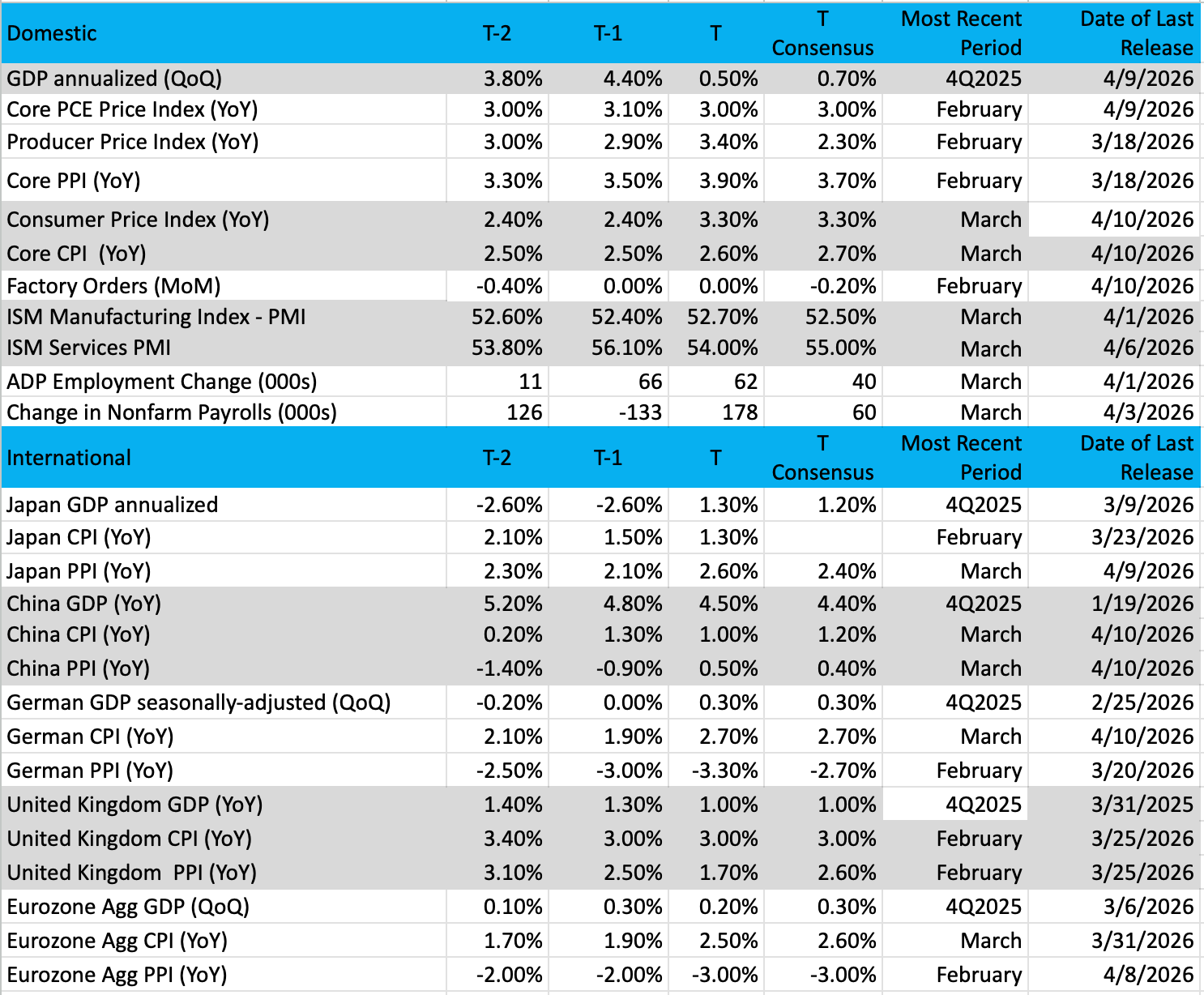

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

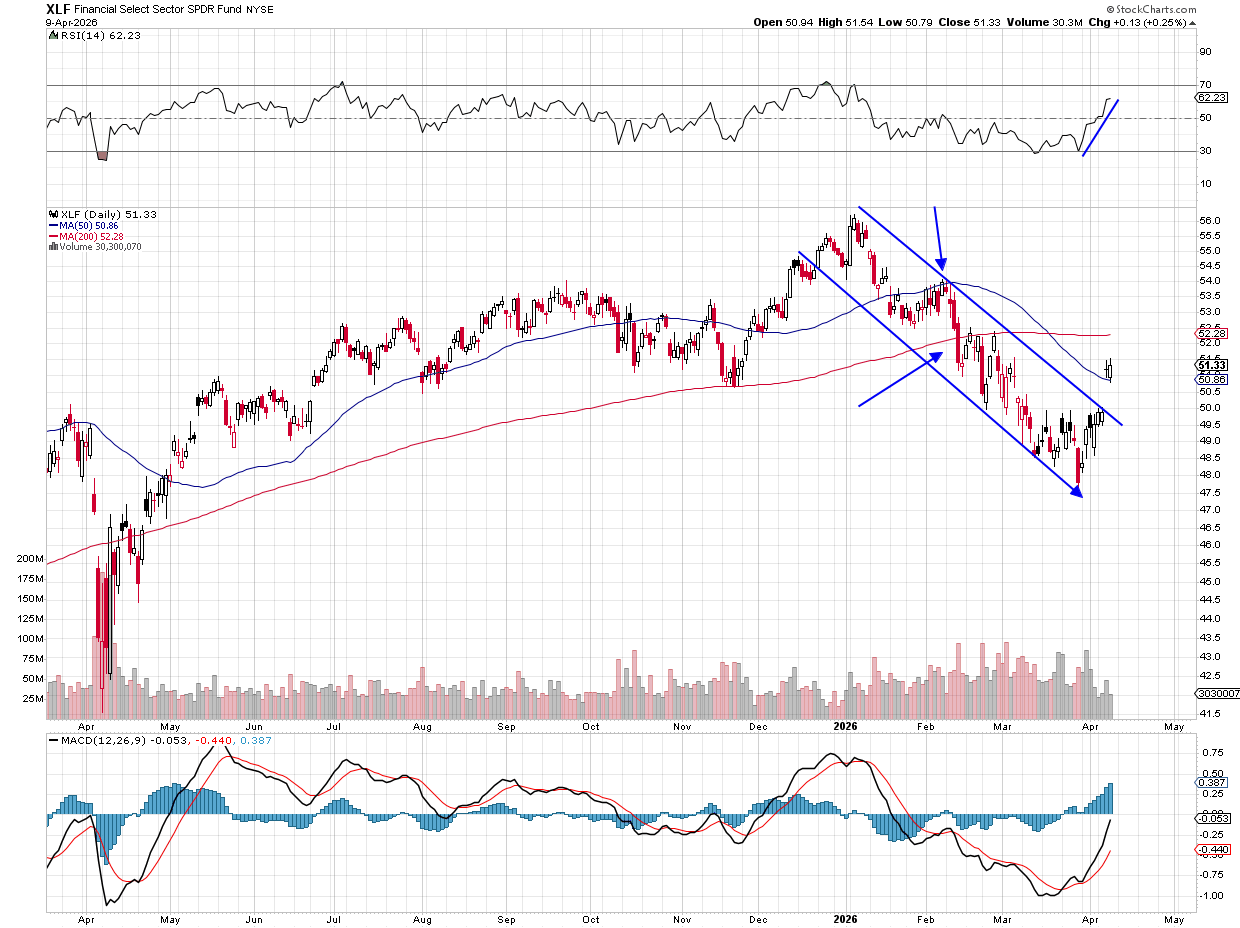

Chart of the Week: State Street Financial Select Sector SPDR ETF (XLF)

Don’t look now but earnings season is about to get underway. As usual, the banks/financials will kick start things, perhaps giving the market a "tell" into how the rest of the season might look. Of course, certain conditions need to be met for the banks to deliver strong earnings, and uncertainty is not one of those. The past several weeks has been filled with worry and doubt over the Iran War, and even with a two-week ceasefire agreed to this week it may not be over.

Uncertainty has a direct negative correlation to bank earnings, one may assume. This is due to the strong relationship between the consumer and the banks as it relates to investing, spending and travel. When the consumer is out spending, the banks are often a secondary beneficiary (more money through the system, transactions, loans, credit cards).

Recent action in the banks has been mediocre until this week when the State Street Financial Select Sector SPDR ETF (XLF) gapped higher and held firm. Notice, in the chart below, how in early February the XLF struggled with resistance at the 50-day moving average, failing miserably and then quickly through the 200-day moving average, where that resistance was even more formidable.

A recent "death cross" (50-day moves under the 200-day) was enough to lose more bulls as the selling continued, but this past week saw heavy buying starting on Wednesday and now the XLF finds itself trying to make a move to the 200-day moving average. Resistance is at $54; a quick move up there would set the ETF as overbought.

Indicators have now flipped from bearish to bullish, and just in time. The only concern I can see here is the weak volume on the rally this past week, clearly short-covering but not overwhelming turnover. We’ll see if that matters over the coming days. If the financials roll over then the market may have a problem. Next week we hear from JPMorgan Chase (JPM) , Goldman Sachs (GS) , Bank of America (BAC) , Citigroup (C) and Wells Fargo (WFC) . As they go, so goes the XLF.

Other charts we shared with you this week were:

Monday, April 6: S&P 500 - Did the Bulls Pull Off the 'Great Escape'?

Monday, April 6: Rocket Companies (RKT) - This New Diplomat Could Be Prepping for Takeoff

Tuesday, April 7: Bank of America (BAC) - Getting Ready for Bank of America Earnings

Wednesday, April 8: Nvidia (NVDA) - Nvidia Indicators Begin to Brighten

Thursday, April 9: Apple (AAPL) - Apple's Tumble Could Signal a Fresh Trading Opportunity

The Week Ahead

Developments associated with this weekend's U.S.-Iran ceasefire talks will influence how U.S. equity markets begin next week. We’ll have our eyes open and our ears glued not only to what is said over the weekend, but the language and tone that underpins it.

In Friday’s video, we explained our thinking as to why next week’s March PPI report has the potential to be far more market-moving than the consensus-matching March CPI report. As we explained, and as you can see in the table below, core PPI levels were already moving higher even before the U.S.-Iran conflict, and that was already poised to apply some margin pressure. Given the big step-ups in the Prices sub-indices in ISM’s March PMI reports, we are likely to see a further move higher in the March PPI data.

That has the potential to shake the market and have it come around to what we’ve been saying about consensus 2026 EPS expectations for the S&P 500. As you can see in the following charts, despite that move up in recent PPI figures, the fallout from the U.S.-Iran conflict on energy and petrochemical prices, and the increase in transportation costs and fuel surcharges, consensus EPS expectations for the S&P 500 have only risen compared to the end of February and late December.

Next week also brings multiple Fed speakers, with just under a dozen appearances. The vast majority of those will come after Tuesday’s March PPI report, and that could make their comments worth listening to, but we’ll be more focused on the Fed speaker comments after Wednesday’s Beige Book report.

And as some of the final pieces of March data are published, we’ll revisit GDP expectations for Q1 2026. Exiting this week, the Atlanta Fed GDPNow model pegs Q1 2026 GDP at 1.3%, better than the 0.5% figure for Q4 2025, but down a bit from the model’s 3.1% figure in late February.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, April 13

Existing Home Sales – March (10:00 AM ET)

Tuesday, April 14

NFIB Small Business Optimism Index – March (6:00 AM ET)

ADP Employment Change Report – Weekly (8:15 AM ET)

Producer Price Index – March (8:30 AM ET)

Wednesday, April 15

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Empire State Manufacturing Index – April (8:30 AM ET)

Import/Export – March (8:30 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Fed Beige Book (2 PM ET)

Thursday, April 16

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Philadelphia Fed Index – April (8:30 AM ET)

Industrial Production & Capacity Utilization – March (9:15 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, April 17

Housing Starts & Building Permits – March (8:30 AM ET)

International

Tuesday, April 14

China: Imports/Exports, Balance of Trade – March

Japan: Industrial Production, Capacity Utilization – February

Germany: Wholesale Prices – March

Wednesday, April 15

Eurozone: Industrial Production - February

Thursday, April 16

Japan: Machinery Orders – February

China: GDP – Q1 2026

China: Industrial Production, Retail Sales – March

UK: Industrial Production, GDP – February

Eurozone: CPI – Inflation Rate

Friday, April 17

China: Foreign Direct Investment - March

First-quarter earnings season moves up a gear next week. We have three Portfolio holdings — Bank of America (BAC) , Morgan Stanley (MS) , and Netflix (NFLX) — reporting. Ahead of those updates, we’ll get quarterly results from Goldman Sachs (GS) , JPMorgan Chase (JPM) , Citigroup (C) , and Wells Fargo (WFC) . What those four show and tell about investment banking activity, stock market volatility and trading revenue, the private credit market, and loan activity will set the table for BofA and Morgan Stanley. Our expectation is a favorable picture for investment banking will be delivered, especially with SpaceX’s April analyst day meeting ahead of us.

In late March, Netflix announced its latest forthcoming price increase, and that led us to increase our price target to $115 for the shares. As interested as we’ll be in paid subscriber count figures, we’ll be as focused on the update on advertising revenue, content spending, and the upcoming programming slate, and what management plans to do with that $2.8 billion breakup fee from the aborted effort to acquire Warner Bros Discovery (WBD) .

Applied Materials (AMAT) is not set to report for more than a few weeks out, but we will be sifting through market comments and guidance from ASML Holding (ASML) on Wednesday.

When we review other companies’ results and guidance next week, we'll be on the lookout for comments about the impact of tariffs, energy prices, and other key inputs. We’ll also be listening for any indications that customers are delaying purchases or extending cycle times for corporate deals.

Here's a closer look at the earnings reports coming at us next week:

Monday, April 13

Open: Fastenal (FAST), Goldman Sachs (GS)

Tuesday, April 14

Open: Albertsons (ACI), BlackRock (BLK), CarMax (KMX), Citigroup (C), Johnson & Johnson (JNJ), JPMorgan Chase (JPM), Wells Fargo (WFC)

Wednesday, April 15

Open: ASML (ASML), Bank of America (BAC), Morgan Stanley (MS), PNC (PNC), Progressive (PGR)

Close: JB Hunt Transportation (JBHT)

Thursday, April 16

Open: Abbot Labs (ABT), BNY Mellon (BK), Charles Schwab (SCHW), PepsiCo (PEP)

Close: Netflix (NFLX)

Friday, April 17

Open: Ally Financial (ALLY), Ericsson (ERIC), Fifth Third (FITB), State Street (STT).

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.