Weekly Roundup: Bracing for the March-Quarter Earnings Deluge

With a likely resetting of market expecations ahead, here's our approach for this 'rudderless' market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For the holiday-shortened week, stocks ended in the red, as tariff and trade developments continued to dominate headlines, Fed Chair Powell dashed market hopes by telegraphing a rate cut is not imminent, and the list of companies delivering underwhelming guidance grew. In short, the market continued to deal with issues we raised several weeks back and that led the S&P 500 to close 1.5% lower this week, while the Nasdaq Composite shed 2.6%.

Looking ahead, barring meaningful progress on trade talks or the rollback of tariffs, items that would help remove the current cloud of uncertainty plaguing the market, economy, and corporate earnings, the probability is high the stock market will remain rudderless. For us, this means remaining vigilant as we use incoming data and company comments to refresh our expectations even as the market resets its hopium-infused ones.

Our view has been that 2025 consensus EPS expectations for the S&P 500 would have to be reset lower, but despite what has transpired so far, the consensus figure still calls for 10% growth compared to 2024. Those same expectations also still call for ~7% growth in EPS for the June 2025 quarter for that market basket, compared to the March 2025 quarter. While down from 9% earlier this year, that revised 7% figure is only in line with the 20-year average for that sequential EPS comparison. That level of expectation suggests to us that the market has not fully baked in the impact of tariffs or slower consumer and business spending prospects.

We continue to see risk that consensus EPS expectations for S&P 500 companies for the June quarter and H2 2025 are poised to move lower as the velocity of companies updating their outlooks to reflect tariffs and consumer and business uncertainty accelerates over the next few weeks. We had a taste of that late this week with quarterly results from UnitedHealth UNH, D.R. Horton DHI, and others. Those reports reaffirm our view the market will need to reset 2025 EPS expectations for the S&P 500 in the coming weeks. In turn, those EPS growth rate revisions are likely to spur renewed questions about proper P/E multiples for that market basket.

For us, it’s simply another reason to keep our inverse ETF positions in play and carefully consider deploying the TheStreet Pro Portfolio’s cash. As we navigate the hurdles ahead and the market comes around to our line of reasoning, based on what we learn in the process and what upcoming data tells us, we’ll continue to evaluate the our inverse ETFs and other opportunities. All the more reason for members to pay attention to our alerts in the coming weeks.

Before we move on with this week’s Roundup, here are some programming notes for the next two weeks:

- Because Chris will be guest co-hosting Yahoo! Finance’s Catalyst program on Wednesday morning, Office Hours for next week will be held on Monday, April 21, between 4 PM – 5 PM ET in the Forum.

- Ahead of our next Stocks & Markets podcast conversation with Jay Woods, Global Macro Strategist at Freedom Capital, we’re asking you for questions you’d like us to ask Jay. Please either deposit them in the Forum or in the comments section beneath this week’s podcast conversation with Peter Tchir.

- With the end of April landing in the middle of the following week, the next Monthly Roundup will be published on Friday, May 2, followed by one on May 30.

Catching Up on the Portfolio This Week

On Monday, we picked up shares of six portfolio holdings — Apple AAPL, Elastic ESTC, Marvell MRVL, Meta META, Universal Display OLED, and Qualcomm QCOM — following President Trump’s rollback of his so-called reciprocal tariffs on smartphones, laptop computers, memory, chips, and other electronics.

As we made those trades, we noted that while we did not buy more shares of Nvidia NVDA or ServiceNow NOW given their existing position sizes, their current prices skewed very favorably for members whose position size is below the portfolio’s. Keeping us bullish on Nvidia and Marvell, both Alphabet GOOGL and Amazon AMZN reaffirmed their capital spending plans. Also, Taiwan Semiconductor’s TSM March-quarter results showcased a 73.5% year-over-year revenue jump in its High-Performance Computing segment, management reaffirmed its AI business should double this year and laid out longer-term guidance that calls for its top line to grow at a mid-20% compound annual growth rate over the 2024-2029 period.

Following the trades outlined above, the portfolio’s cash levels remain at elevated levels, and given our near-term outlook we expect to remain owners of our inverse ETF positions. We will continue to evaluate their role in the portfolio as new information arrives, even as we continue to hunt for more than favorable risk-to-reward opportunities for our cash holdings.

We also made several price-target adjustments this week. We reduced our price target to $45 for Bank of America BAC, lowered our target to $310 for American Express AXP, and adjusted our Nvidia target to to $150 from $175 following news the company will need a special license to export its H20 chip to China. On Thursday, we trimmed our Morgan Stanley MS price target to $125 from $145 amid slower expectations for investment banking fees, and also upped our Palantir PLTR target to $105 from $95 given a thesis-confirming development and the potential for another one.

Also this week, Costco COST announced a nice boost to its quarterly dividend to $1.30 per share, up from $1.16. The quarterly dividend is payable on May 16 to shareholders of record at the close of business on May 2.

Now let’s see what Wall Street had to say about the ortfolio’s holdings during this abbreviated trading week:

Truist trimmed its Alphabet target back to $200 from $220.

Philips Securities upped its rating on Bank of America to Buy from Accumulate, slapping a fresh $45 target on the stock. Argus trimmed its BAC target to $47 from $53, sharing our view that a rebound in investment banking fees is likely to be pushed out as tariff-related market turmoil delays deal activity. RBC Capital shared that sentiment but took its price target to $45.

Argus lowered its Nvidia price target to $150 from $175 but maintained its Buy rating. Wolfe Research made a similar move to $150 from $180, also reiterating its Outperform rating.

Morgan Stanley lowered its Meta price target to $615 from $660 as part of a larger set of target cuts that included reducing its Alphabet target to $185. Morgan Stanley also lowered its target on Elastic to $120, ServiceNow's to $881, and Amazon's to $245.

Citi raised estimates and opened a "30-day positive catalyst watch" on Qualcomm citing better-than-expected handset demand, particularly from China. The firm expects a "beat and raise" during earnings and says low sentiment provides a "reasonable valuation" on Qualcomm shares.

Morgan Stanley upgraded shares of United Rentals URI to Overweight from Equal Weight with a $702 target. The firm noted URI’s relatively limited direct exposure to tariff headwinds, which, combined with the company's strong pricing power over suppliers, is seen positioning it to better mitigate the risk of inflation.

Raymond James upped its Waste Management WM target to $258 from $237, noting an uneventful March-quarter earnings report. We look forward to an update on its Stericycle business when it reports on April 28 and an even deeper dive at its June 24 Investor Day.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, April 9: Why We Scooped Up Shares of Multiple Holdings

Tuesday, April 10: Apple's Foldable iPhone Reports Are Positive for This Holding

Wednesday, April 11: Get Ready for TheStreet’s Stocks and Markets Podcast

April 11: TheStreet Stocks & Markets Podcast #1: Buy the Dips, Sell the Rips With Peter Tchir

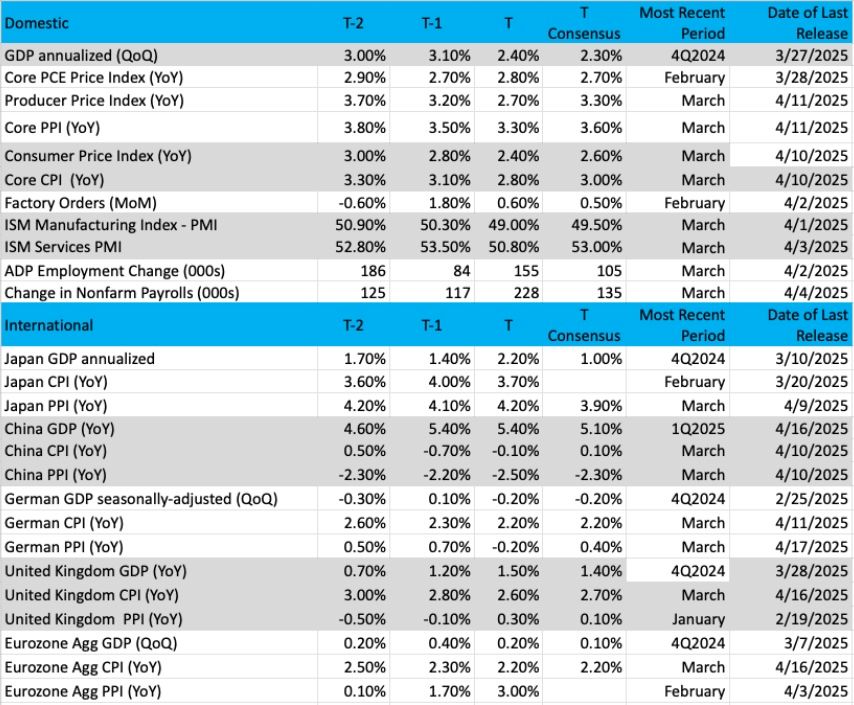

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week Will Return Next Week

With Bob Lang on vacation, we’ll return to our regular technical look at the S&P 500 and portfolio holdings next week. Stay tuned!

The Week Ahead

The recent trifecta of fresh economic data, March-quarter earnings reports and Fed speakers will continue next week. While we will get a few more pieces of March economic data, we will be much more interested in the findings for S&P Global’s Flash April PMI data.

What we’ll be looking for are clear indications of how President Trump's tariffs and announced retaliatory efforts are impacting the economy. As we parse the data, we’ll also be reflecting on Fed Chair Powell’s comments this past week, which unsettled the market and drew the ire of the president, and whether it could alter the outlook for monetary policy.

The same goes for the latest Fed Beige Book findings next week. As we digest those comments, we’ll also be closely tracking the language used by Fed officials making the rounds in the latter part of the week.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, April 21

· Leading Indicators – March (10:00 AM ET)

Tuesday, April 22

· Richmond Fed Manufacturing and Services Index – April (10:00 AM ET)

Wednesday, April 23

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· S&P Global Flash PMI – April (9:45 AM ET)

· New Home Sales – March (10:00 AM ET)· EIA

Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Beige Book (2 PM ET)

Thursday, April 24

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Durable Orders – March (8:30 AM ET)

· Existing Home Sales – March (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, April 25

· University of Michigan Consumer Sentiment Index (Final) – April (10:00 AM ET)

International

Tuesday, April 22

· Eurozone: Consumer Confidence (Flash) - April

Wednesday, April 23

· Japan: Jibun Bank Flash PMI – April· Eurozone: HCOB Flash PMI – April

· UK: S&P Global Flash PMI - April

Thursday, April 24

· Eurozone: New Car Registrations - March

Friday, April 25

· Japan: Leading Economic Index – February

· UK: Retail Sales - March

Although there are no market-moving earnings slated for Monday, it would be a mistake to think that means it will be a quiet week for corporate earnings. In fact, it will be the busiest week thus far for March-quarter reporting — and as we saw late this past week there are reasons to expect not all will be hunky dory. We’re referring, of course, to the downside guidance issued by UnitedHealth UNH and D.R. Horton DHI Thursday morning.

Because UNH shares comprise 9% of the Dow Jones Industrial Average, the drop in that stock weighed on the Dow late last week. By comparison, UNH shares account for just 1.2% of the S&P 500. The lesson here is understanding how what's contained in an index and how it’s weighted can make a big difference.

We point that out because the coming week sees 122 S&P 500 constituents reporting. The largest will be TheStreet Pro Portfolio holding Alphabet GOOGL, but given its size in the basket, folks will also be closely following Tesla’s TSLA results next week as well. Recent Tesla shipment data have been less than favorable, but on the earnings call we’ll be listening to see if Elon Musk aims to reduce his DOGE role to re-focus on the company.

Two other portfolio holdings reporting next week are ServiceNow NOW and United Rentals URI, but in our bid to connect the dots, we’ll also be digging into results and comments from Quest Diagnostics (DGX), Synchrony Financial (SYF), Check Point Software (CHKP), NextEra Energy (NEE), IBM (IBM), SAP (SAP), Lazard (LAZ), and Digital Realty Trust (DLR). We’ll also be interested in comments from auto-related companies, such as Genuine Parts (GPC) and Visteon (VC), regarding Trump tariffs.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, April 22

· Open: 3M (MMM), GE Aerospace (GE), Genuine Parts (GPC), Herc Holdings (HRI), Kimberly-Clark (KMB), Lockheed Martin (LMT), Northrop Grumman (NOC), PulteGroup (PLTE), Quest Diagnostics (DGX), Synchrony Financial (SYF), Verizon (VZ)

· Close: Packaging Corp. (PKG), SAP SE (SAP), Tesla (TSLA)

Wednesday, April 23

· Open: AT&T (T), Boeing (BA), Check Point Software (CHKP), General Dynamics (GD), M/I Homes (MHO), Masco (MAS), NextEra Energy (NEE), Norfolk Southern (NSC)

· Close: Chipotle (CMG), Discover Financial Services (DFS), IBM (IBM), Lam Research (LRCX), Meritage (MTH), ServiceNow (NOW), United Rentals (URI).

Thursday, April 24

· Open: American Airlines (AAL), Ameriprise Financial (AMP), Bristol-Myers (BMY), Dow (DOW), Keurig Dr Pepper (KDP), Merk (MRK), Mobileye (MBLY), PepsiCo (PEP), STMicroelectronics (STM), Textron (TXT), Union Pacific (UNP), Visteon (VC)

· Close: Alphabet (GOOGL), Boston Beer (SAM), Digital Realty Trust (DLR), Gilead Sciences (GILD), Intel (INTC), T-Mobile USA (TMUS).

Friday, April 25

· Open: AbbVie (ABBV), Colgate Palmolive (CL), HCA (HCA), Lazard (LAZ).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.