Weekly Roundup: Bracing for a 'Buy the Rumor, Sell the News' Fed Event

It was another postive week for the Pro Portfolio, as we upgraded one holding, rang the register on another, and picked up more of a third. We also laid out our plans for a Bullpen resident.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If we were to sum up the market and its movement this week, we would do it by paraphrasing a quote from Gil Penchina: “Momentum begets momentum.” That’s what we saw this week as the S&P 500 hit new highs multiple times over the last five trading days. We've certainly enjoyed the pull-through at the Pro Portfolio and what it’s done for its year-to-date performance.

What’s been driving this recent momentum? It’s the growing excitement over what the market expects the Fed to say next week. Per the CME FedWatch Tool, the market sees not only a 25-basis point rate cut exiting next week’s meeting, but it also shows similar rate cuts at the Fed’s subsequent three policy meetings in October, December, and January. Going out a big further, the tool shows the market is thinking the Fed will deliver a total of six 25-basis point rate cuts between next week and its final meeting in 2026.

Remember, the Fed already telegraphed two 25-basis point rate cuts and one of that magnitude with its June 2025 updated set of economic projections. While the jobs market has softened since then, consumer inflation pressures have stepped up and, as we saw with the August CPI report, remain at elevated levels.

At the same time, rolling GDP forecasts for the current quarter and even for the final quarter of the year show the domestic economy still growing at a healthy pace. Granted, that can change based on upcoming data, but against that data backdrop, the question we’re contemplating is why would the Fed telegraph six potential rate cuts between now and year-end 2026?

That questioning led to this week’s Stocks & Markets Podcast discussion about the outcome of next week’s Fed meeting likely being a “buy the rumor, sell the news” event for the market.

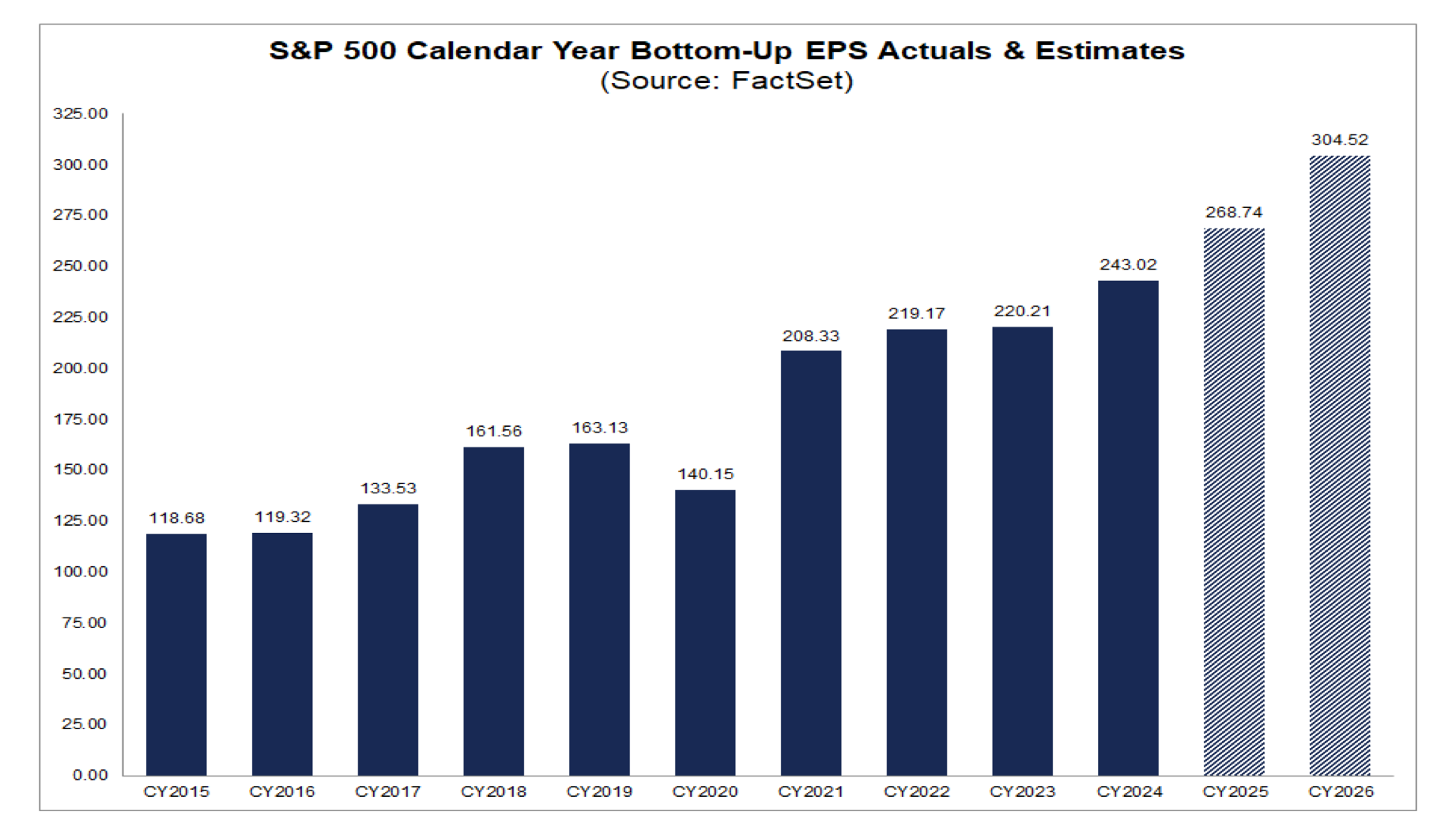

As we think about that potential, let’s consider what’s been driving the market higher. We’ve discussed ample times about softening H2 2025 EPS expectations for the S&P 500 compared to H1 2025. When we look at the latest consensus EPS figures for the S&P 500 vs. those at the end of March 2025, it’s clear they have moved lower.

Yet, the S&P 500 has not only recovered from its late March-April selloff, it’s also easily surpassed levels seen earlier this year, powering ahead to those record highs mentioned above. This tells us that what’s been powering the S&P 500’s move has been multiple expansion, in part predicated upon the market’s expectation for the Fed to go “big” next week.

Here's the thing as we close out the week, the S&P 500’s P/E valuation on the latest consensus EPS figure of $268.74 is 24.6x. The S&P 500 peaked at 25.1x last year, which, outside of the 2001 recession and the global pandemic, was the peak P/E ratio for the basket.

We’re also seeing the Volatility Index (VIX) back below 15, which signals market complacency.

And while not flashing overbought, the S&P 500’s RSI figure of 67.40 isn’t that far away either.

Looking at all above, there is room for the market to be disappointed by what the total package the Fed may deliver next week. Odds are we will get a 25-basis-point rate cut, but the Fed matching the market’s expectation for five more rate cuts over the next 15 months seems like a big stretch.

Think of it this way, what does the Fed have to gain by going out on a limb and telegraphing such expectations, given the totality of the data?

That will keep us on the sidelines early next week, and if the Fed meeting winds up being a “buy the rumor, sell the news” event, we have our shopping list and potential new addition from the Bullpen that we’ll be watching very closely. Of course, we’ll be with you every step of the way.

Enjoy your weekend, Saturday’s signals Alert, and Sunday’s bowl of more light-hearted fare. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio continued to advance this week, pushing past 11% on a year-to-date basis. A double-digit move in Palantir PLTR led the way, which makes us thankful we added to the Portfolio’s PLTR position in August at $154.61 and again earlier this month at $160.63. Other notable performers this week included Nvidia NVDA, Marvell MRVL, Morgan Stanley MS, Eaton ETN, and Axon AXON.

While we can celebrate those wins, the reality is the Portfolio’s returns of late have been weighed down by shares of Dutch Bros BROS and Universal Display OLED. With the east-to-west expansion story still intact, Dutch Bros shares are flirting with support at the 50-day and 200-day moving averages. Let’s see if that holds — if not, should the stock fill the gap in the chart near $57.50, that would be a compelling pick-up point. With OLED, we see a triple bottom potentially forming in the chart near $135, and if that level holds, we’re inclined to make a move to round out our position size.

On Monday, we discussed the factors that we’ll be following and what it could take for us to get more interested in the homebuilding sector. Tuesday, we shared the upcoming dividend payments we can expect from our holdings and those that will benefit the Portfolio’s cash position in the final quarter of the year. On Wednesday, we upgraded Axon shares to a One rating following a thesis-confirming presentation by the company at this week’s Goldman Sachs investor conference.

Thursday, we discussed our plans for Bullpen resident Welltower WELL, including key support levels we’ll be closely watching. Following the string of new record closings for the S&P 500, on Friday, we opted to take some very profitable Alphabet GOOGL chips off the table, funneling the proceeds into Waste Management WM shares. That relatively even swap we are making should keep the Pro Portfolio’s cash position size above 10%, maintaining our firepower so we have the option to be opportunistic if next week’s Fed meeting is indeed a “buy the rumor, sell the news” event.

And as we clear next week’s set of IPOs, we fully intend on revisiting our price targets for Bank of America BAC and Morgan Stanley MS.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during this week:

Phillip Securities downgraded Alphabet to Accumulate from Buy with a price target of $265, up from $235. Like many others, the firm viewed the U.S. district judge's ruling positively and believes restrictions on exclusivity will have limited impacts on Google's product strength and partner incentives. It cited valuation for the downgrade following the stock's recent rally.

DA Davidson downgraded Apple AAPL shares to Neutral from Buy, given what it saw as “uninspired” new products from the company this week. The firm’s AAPL target remains $250. BofA upped its AAPL target to $270 from $260 following Apple’s iPhone launch event this week, while Melius Research increased its to $290 from $260. JPMorgan saw the event as more of a “mixed bag” and was less excited about potential iPhone Air adoption given its premium price point.

Daiwa Securities initiated coverage of Eaton with an Outperform rating and a $390 target.

Morgan Stanley named Amazon AMZN shares as a Top Pick as the company’s push into the fresh grocery market will unlock “durably faster growth.”

Also, this week, DA Davidson upped its rating on Nvidia to Buy with a target of $210, up from $195. The catalyst for the move was “the belief that the growth in AI compute demand will drive enough demand to sustain growth into next year and likely beyond.” We won’t spoil it here, but in Saturday’s signals Alert, you‘ll find an interesting comment between folks at Meta META and Nvidia that jives with what DA Davidson was thinking.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, September 8: OpenAI's Spending Message Boosts These Portfolio Plays

Tuesday, September 9: Apple Underwhelms With iPhone 17 Event

Wednesday, September 10: Stocks & Markets Podcast: Rate Cut Reaction, Healthcare Stocks, and Jaguar's Reboot

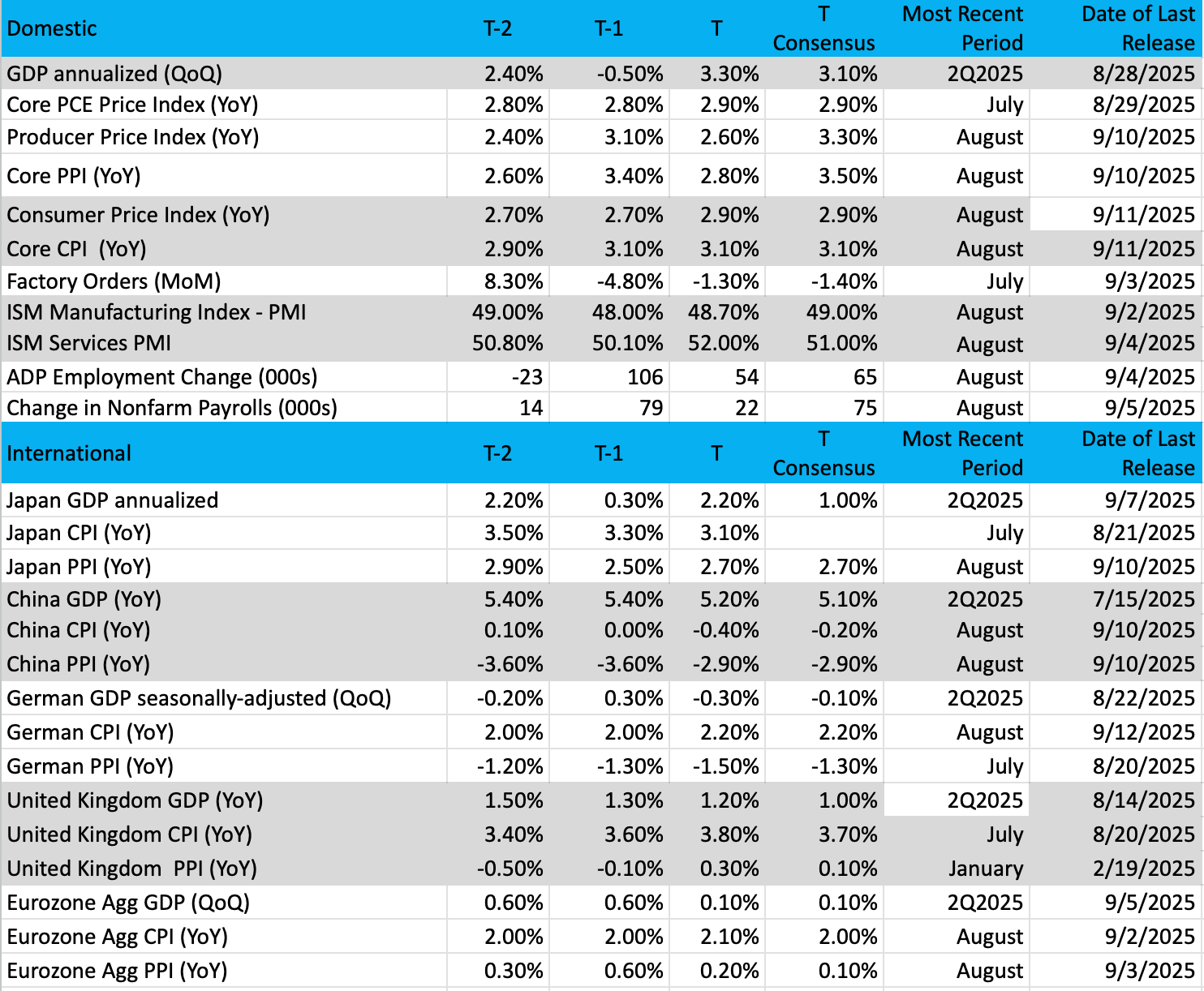

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

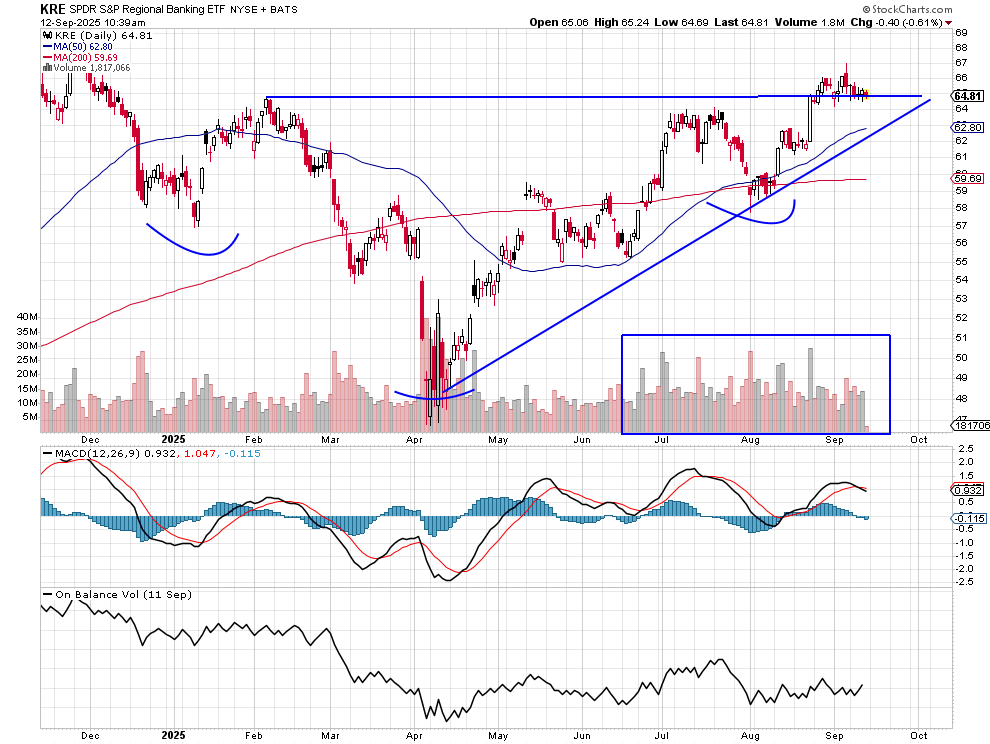

Chart of the Week: SPDR S&P Regional Banking ETF (KRE)

Don’t look now, but the Fed has a meeting next week, the most important one since….the last one! Naturally, there will be discussion over monetary policy and where it goes in the future, but at the moment, it seems policy is pivoting towards a more dovish posture. The data followed by the Fed is more "money-friendly," and with some comments by Fed speakers and even Chair Powell, there is the notion that the current policy is too tight for an aging economy.

Growth is okay here, perhaps GDP may be growing at 2% this quarter, but there are downside risks to growth. Further, monetary policy changes need to occur quickly, or else there are significant penalties to be paid. One of those is in housing, but banking could also be challenged.

If the committee gets it right, we could see the banks/financials really perform well. If that is the case, we know the big names such as JPMorgan Chase JPM, Bank of America BAC, Morgan Stanley MS, and Goldman Sachs GS will likely rise up, but we should also see the regional banks thrive in a friendlier interest rate environment. The KRE is an ETF that houses many of the best regional banks in the country. The ETF is strong and looks to continue its winning ways.

The KRE chart is very bullish, with a series of higher highs, higher lows, and a bullish inverse head/shoulders on the chart. Volume trends have been very bullish, with the biggest volume days occurring while the stock has been rising. Resistance at $64 was exceeded this month and is being tested now. If that holds, we see the KRE making a run to $70 before too long.

Other charts we shared with you this week were:

Monday, September 8: S&P 500 – Why Recent Action May Not Inspire the Bulls or Bears

Monday, September 8: Vulcan Materials (VMC) - Vulcan Materials Is Building Something

Tuesday, September 9: Morgan Stanley (MS) - Morgan's Movin' Up

Wednesday, September 10: TJX Companies (TJX) - Why This Overbought Holding Shouldn't Scare You Away

Thursday, September 11: Axon Enterprise (AXON) - With Axon, It Pays to Follow the 'Big Money'

The Week Ahead

With another leg down in the pace of quarterly earnings reports, next week’s focus will primarily be on additional August economic data and the outcome of the Fed’s policy meeting. When we say outcome, it’s more than just the Fed delivering on the market’s expectation for a September rate cut. The central bank will update its set of economic projections, revising its outlook for the economy’s rate of growth, the Unemployment Rate, and the Fed Funds rate.

As we get ready for the Fed meeting, we are keeping a close watch on developments in DC regarding central bank's makeup. It looks like Senate Republicans are aiming to confirm President Trump’s temporary Federal Reserve pick as soon as Monday. On Thursday of this week, the Trump administration asked an appeals court to remove Lisa Cook from the Federal Reserve’s board of governors by Monday, before the central bank’s next vote on interest rates. The request comes after U.S. District Court Judge Jia Cobb ruled that the administration had not satisfied a legal requirement that Fed governors can only be fired “for cause,” which she said was limited to misconduct while in office.

While the market has come around to widely expect a 25-basis point rate cut next week, the larger question is whether the updated Fed outlook will match the six 25-basis point rate cuts the market expects per the CME FedWatch Tool. Remember, the Fed’s June 2025 set of economic projections showed only three rate cuts from the second half of 2025 and all of 2026. While the job market has softened, as we saw with this week’s August CPI report, inflation pressures remain rather sticky.

To that, we can add the Atlanta Fed’s GDPNow model, pegging current quarter GDP at 3.1%. Granted, the New York Fed’s Nowcasting model has a 2.1% figure for the current quarter, but it also sees the following one at 2.2%. Those figures would suggest the economy isn’t at risk of falling off a cliff, something Fed Chair Powell is likely to echo.

We will want to revisit those GDP forecasts after the August reports for Retail Sales, Industrial Production, and Housing Starts, which we’ll get on Tuesday and Wednesday. Just in time for the Fed to conclude its policy meeting.

Barring any dramatic change in those regional Fed forecasts, we think the central bank will not “go big” with its Fed Funds forecast update if only for the simple reason that it can adjust the pace of rate cuts down the road should the data warrant it. The market will, as it usually does, hang on Fed Chair Powell’s comments, but given the run-up in stocks and the Volatility Index once again flashing market complacency, we believe there is reason to think the market will be underwhelmed by the Fed’s aggregate actions, comments, and forecasts next week.

If that is the outcome we get, we have our shopping list in hand, which includes levels at which we would be inclined to call shares of Welltower WELL up from the Bullpen.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, September 15

· Empire Manufacturing Index – September (8:30 AM ET)

Tuesday, September 16

· Retail Sales – August (8:30 AM ET)

· Import/Export Prices – August (8:30 AM ET)

· Industrial Production & Capacity Utilization – August (9:15 AM ET)

· Business Inventories – July (10:00 AM ET)

· NAHB Housing Market Index – September (10:00 AM ET)

Wednesday, September 17

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Housing Starts & Building Permits – August (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Rate Decision, Updated Fed Economic Projections (2 PM ET)

Thursday, September 18

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Philadelphia Fed Index – September (8:30 AM ET)

· Leading Indicators – August (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

International

Monday, September 15

· China: Retail Sales, Industrial Production, Fixed Asset Investment – August

· Eurozone: ECB Survey of Monetary Analysts

Tuesday, September 16

· UK: Employment Change – July

· Eurozone: Industrial Production – July

· Eurozone: ZEW Economic Sentiment Index - September

Wednesday, September 17

· Japan: Imports/Exports – August

· UK: Inflation Rate 0- August

· Eurozone: Inflation Rate, Consumer Price Index (Final) - August

Thursday, September 18

· Japan: Machinery Orders – July

· UK: Bank of England Interest Rate Decision

Friday, September 19

· Japan: Inflation Rate – August

· UK: Retail Sales - August

The pace of corporate earnings reports slows dramatically next week. Still, we will lean into comments on consumer spending from Dave & Buster’s PLAY and assess the sequential findings for Lennar’s LEN booking and backlog levels.

With Darden Restaurants DRI, how is the average ticket and traffic holding up, and how are input costs trending? Is Darden being impacted by folks eating more at home or trading down, or fast casual or fast food?

With FedEx FDX, what does it say about the holiday shopping season and the overall tone of the economy?

The answer to those questions and others that will crop up along the way will help us prepare for the upcoming September-quarter earnings season. That’s right, after this week, there are just 12 trading days left in the quarter.

Here's a closer look at the earnings reports coming at us next week:

Monday, September 15

· Open: Hain Celestial (HAIN),

· Close: Dave & Buster’s (PLAY)

Tuesday, September 16

· Open: Ferguson plc (FERG)

Wednesday, September 17

· Open: Cracker Barrel (CBRL), General Mills (GIS)

· Close: Steelcase (SCS)

Thursday, September 18

· Open: Darden Restaurants (DRI), FactSet (FDS),

· Close: FedEx (FDX), Lennar (LEN)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.