Weekly Roundup: Another Record High for the S&P 500 and Pro Portfolio

The market’s valuation sets a high bar for next week's Big Tech earnings and the Fed.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The S&P 500 hit a new record high on Friday following a September Consumer Price Index report and other data that suggest the Fed will deliver a rate cut next week. Friday’s across-the-board move higher for the major market indexes capped another positive week for the stock market and TheStreet Pro Portfolio.

With just under a third of the S&P 500’s basket having reported, we saw consensus EPS expectations for this year and 2026 inch up yet again this week. Despite those upward revisions, the S&P 500 closed this week near 25.4x expected 2025 EPS of $268.18. Safe to say that is a rather stretched multiple, especially when the market sees the year-over-year growth rate for H2 2025 EPS slowing to 7.5% compared to nearly 12% in H1 2025. That tells us expectations are running high, but when we look at the below-average trading volume for both the S&P 500 and the Nasdaq Composite, it raises questions about market conviction.

Next week, we see another 175 S&P 500 constituents reporting, including widely held Apple (AAPL) , Microsoft (MSFT) , Amazon (AMZN) , Meta Platforms (META) , and Alphabet (GOOGL) . Those stocks and other basket residents mean we will have more than 30% of the S&P 500’s weighting report next week, and that, as well as the Fed’s policy decision and Fed Chair Powell’s comments, mean it will be a big week for the market. Based on our comments above about the S&P 500 P/E and Friday’s trading volume, there is reason to think there is room for this priced-to-perfection market to be disappointed.

Over the last few weeks, we’ve once again seen the market reward companies that deliver beat-and-raise quarterly reports and punish those that don't. We don’t see that changing next week, especially with capital spending comments from those aforementioned Big Tech companies in focus.

During the week, we discussed rising AI adoption and usage data points as well as other tie-up announcements, including Friday’s between Google and Anthropic, that indicate there is much room yet to run when it comes to AI. Measured alongside comments that Microsoft will be capacity constrained well into 2026, suggests we should see another leg up in those capital spending figures for H2 2025.

As we take stock of those figures, we’ll also be looking for directional clues about capital spending levels in 2026. We suspect they will move higher, and if we get that confirmation, it will be a positive catalyst for our AI chip holdings and others benefiting from the AI and data center buildout.

Laying out all those oncoming reports and developments, Wednesday afternoon will be a big one for the market. We have the outcome of the Fed’s decision and quarterly results from Alphabet, Meta, and Microsoft. We could also see more saber-rattling ahead of the expected Trump-Xi meeting in South Korea on Thursday. To us, that all means if the market continues to race higher on low volume, a prudent move or two before Wednesday afternoon may be called for. After all, no one ever went broke taking a profit.

We’ll take it one step, one day at a time, and based on what lines up, we’ll communicate our thoughts and any moves with you as we make them for the Portfolio.

Enjoy your weekend, and be sure to check out our Saturday signals column. See you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

While we didn’t make any trades with the Pro Portfolio this week, we continued to benefit from the additions we made with Axon Enterprise (AXON) , Arista Networks (ANET) , Dutch Bros (BROS) , and Costco (COST) earlier this month. Other strong players on our bench this week included shares of Apple (AAPL) , Amazon (AMZN) , as well as those for Qualcomm (QCOM) , Alphabet (GOOGL) , and American Express (AXP) .

The one position that restrained the Portfolio’s performance relative to the S&P 500 this week was United Rentals (URI) . Those shares came under pressure following the company’s September-quarter EPS miss, but as we explained in our alert discussing those results, we see brighter days ahead for the stock.

Closing out the week, none of our holdings is near the 4.5% position size level but given what’s to come next week, we will be reviewing each position’s relative strength index (RSI) level over the weekend. Should the market continue to advance and its RSI level approach an overbought condition ahead of the Fed’s policy decision and Fed Chair Powell’s press conference comments, we may elect to make a prudent move or two. With the Portfolio’s cash levels at roughly 6.5% of its assets, we wouldn’t mind having a wee bit more cash on hand as the current earnings season heats up and the potential for Powell to once again underwhelm the market with his comments.

With speculation that Welltower (WELL) could make a play for Barchester Healthcare, one of Britain's biggest nursing home operators, we’ll keep our ears open over the weekend to see if something is announced before Welltower reports its September-quarter results early next week.

Welltower will be one of the 10 Portfolio holdings reporting next week. As we cull through the results, we’ll revisit price targets as well as panic and pick-up points where it makes sense. If we need to amend any of our stock ratings, we’ll make that call as well.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

On Monday, Evercore ISI added Apple (AAPL) shares to its “Tactical Outperform List,” reiterating its Outperform rating and $290 target, while Loop Capital took its target to $315. Wells Fargo upped its American Express target to $400 from $375, BofA reset its Alphabet target to $280 from $252, and Barclays bumped up its target for Vulcan Materials (VMC) to $320 from $305. Late in the day, we learned JPMorgan raised its Morgan Stanley (MS) target to $157 from $122.

Tuesday, Wells Fargo raised its Welltower target to $200 from $185. The firm also lifted its Apple target to $290 from $245. Morgan Stanley nudged its Dutch Bros target higher, going to $86 from $84. JPMorgan made a larger increase to its Vulcan Materials target, taking it to $340 from $330.

Qualcomm saw its price target raised to $200 from $190 at Susquehanna on Wednesday.

Thursday, Bernstein made a sizable change to its Alphabet price target, taking it to $260 from $210. Citi bumped its United Rentals target a tad to $1,140 from $1,130, and Amazon shares caught a fresh Overweight rating at KeyBanc with a $300 target.

Truist raised its Meta (META) target to $900 from $880 on Friday, the same day the firm dialed back its target for United Rentals to $1,169 from $1,194. RBC Capital also lowered its URI target to $1,123 from $1,152. In our URI earnings note, we shared we would likely see such moves, and as expected, those changes restrained Friday’s move in URI shares.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Tuesday, October 21: What We Learned From the Latest Earnings Reports

Wednesday, October 22: Stocks & Markets Podcast: Product Returns and the Economy With ReturnPro's CEO

Friday, October 24: Implications of a Modestly Cooler September Core CPI

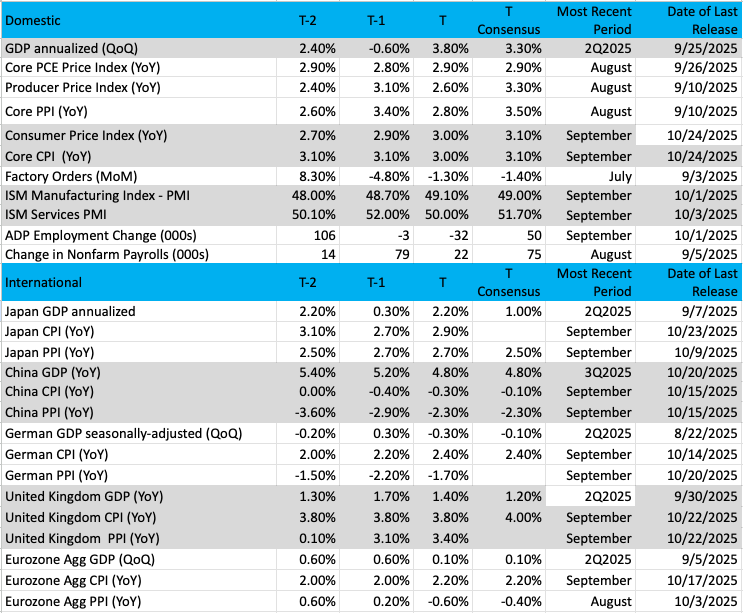

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

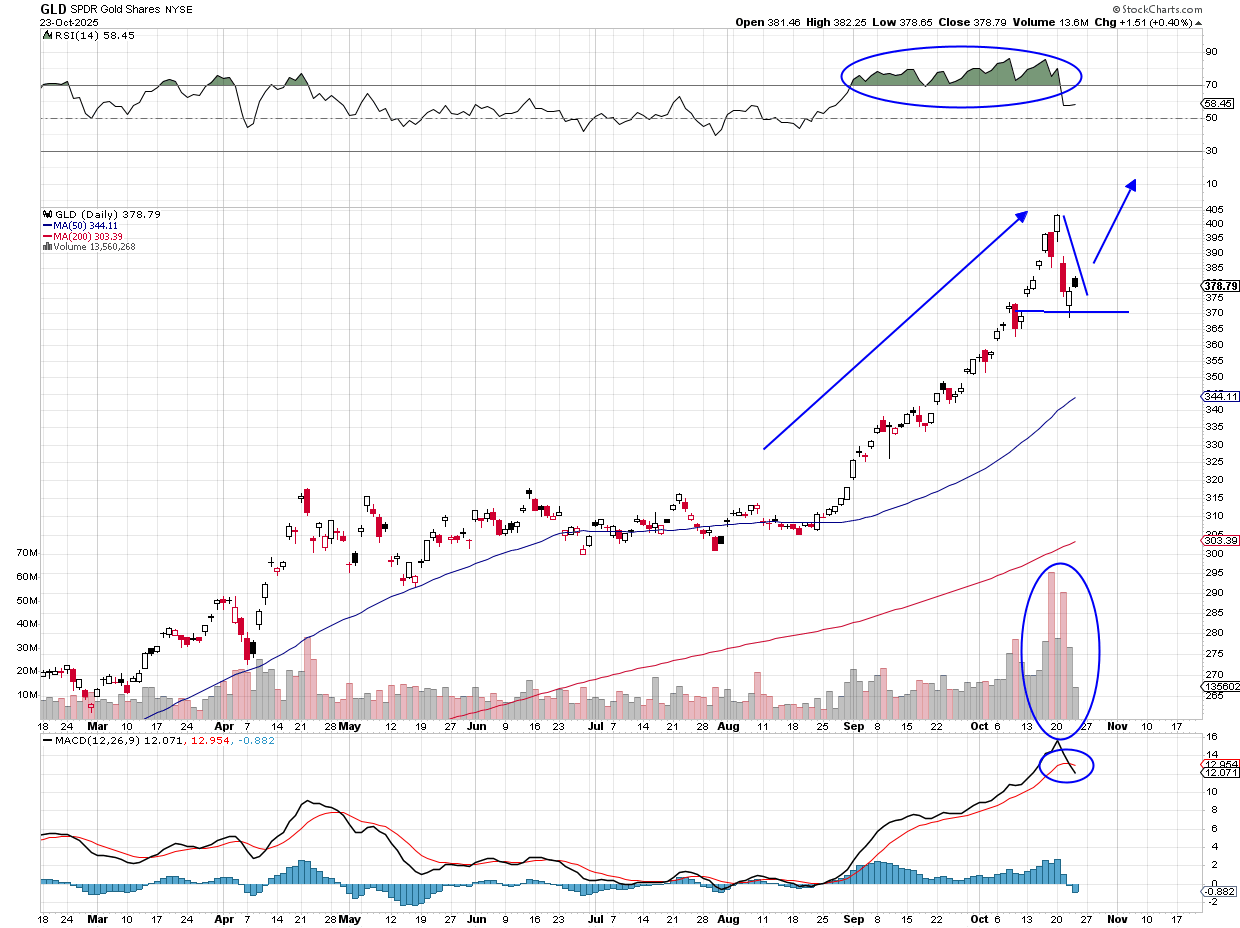

Chart of the Week: SPDR Gold Shares (GLD)

What an amazing run gold has had in 2025, and much of this has happened over the past two months. The SPDR Gold Shares (GLD) ETF has risen more than 20% since the latter part of August, a stunning move over such a short period of time. As a comparison, the U.S. dollar has risen about 2% while bitcoin, an alternative, is down about 2% during that same stretch. New highs for gold, of course, have been a regularity for the metal in 2025, and with this recent parabolic move, you might ask, "Can this continue?" Let’s find out.

Naturally, gold attracts foreign investors like a fly is attracted to a flame. Countries that do business in dollar terms choose to diversify their risk by having alternatives to the U.S. dollar, considered a fiat currency (paper money issued by a government not backed by anything but a promise to repay). The explosion in gold prices, along with silver, has become a phenomenon, but most would say it has been expected. The U.S. dollar has been losing its value for years due to erosion from inflation and printing more dollars, but gold has not been the recipient of that debasement until now. Demand remains strong for metals in a volatile environment and potentially high inflation down the road. Gold will likely remain elevated but with quite a lot of volatility.

What shows us volatility in gold? The $GVZ is a volatility index for gold, and it has been rising steadily for weeks. This simply means the range of gold prices is rising, and we’ll have more large moves than before. Just this week, GLD moved up $166 and then down $220! Those are some big moves, more than 4% each day.

The chart is bullish, and those waiting for a pullback to add a position are getting one right now. Pullbacks have often been the right time to add gold. Notice the recent down move from the highs at $405 to $378, a nearly 5% move straight down, but a gap fill from $370 was accomplished, and now buyers are looking for an entry point. Moving average convergence divergence (MACD) is rolled over, but that just means this indicator has slowed down. The Relative Strength Index (RSI) was overbought for nearly two months and is giving a low-risk entry buy signal.

How far will gold go? $5,000 is not far off from current levels, which might be a target of $470 on the GLD.

Other charts we shared with you this week were:

Monday, October 20: S&P 500 - Bulls Come Back From a Knockout Punch

Monday, October 20: United Rentals (URI) - A Close Look at United Rentals Ahead of This Week's Earnings

Tuesday, October 21: Amazon (AMZN) - Amazon Is Down, But Not Out

Wednesday, October 22: Broadcom (AVGO) - What's Next for This Bullpen 'Juggernaut'?

Thursday, October 23: Marvell (MRVL) - Maybe This Marvell Pullback Is Just What Is Needed

The Week Ahead

It appears the government shutdown will continue, and next week is an absolute barn burner of a conclusion for October. More than 1,000 companies are reporting next week, including 175 S&P 500 constituents and the Big Tech residents contained in that market index that we own in the Pro Portfolio. It’s going to be a brisk week of press releases and conference calls, and potentially a volatile one, but we’ll be with you every step of the way.

Assuming the government remains shut, a likely scenario given the 44-day shutdown forecast depicted by prediction market Kalshi, we won't receive the bulk of the data expected next week. We’ll continue to make do with other data as we aim to triangulate the vector and velocity of the economy.

While we keep watch on the shutdown, we will also continue to pay close attention to the developments on the geopolitical and trade front. President Trump is expected to meet with Chinese President Xi Jinping on Thursday, October 30, in South Korea. We could see some additional gamesmanship leading up to that meeting, another reason to think next week could be a volatile one. We suspect a positive outcome will be had, but let’s remember the devil will once again be in the details.

Before that Trump-Jinping meeting, the Fed will conclude its latest policy meeting on Wednesday, October 29. The market is widely expecting the central bank to deliver a 25-basis point rate cut, but as we discussed in Friday’s video, Fed Chair Powell could once again offer some sobering comments even as he likely reiterates the Fed being data dependent. Should we see the market chug higher from Friday’s record high for the S&P 500, some prudent action may be called for.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, October 27

· Durable Orders – September (8:30 AM ET)

Tuesday, October 28

· FHFA Housing Price Index – August (9:00 AM ET)

· S&P Case-Shiller Home Price Index – August (9:00 AM ET)

· Consumer Confidence – October (10:00 AM ET)

Wednesday, October 29

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Retail & Wholesale Inventories (Advance) – September (8:30 AM ET)

· Pending Home Sales – September (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Fed Policy Decision – 2 PM ET

Thursday, October 30

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· GDP (Advance) – Q3 2025 (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, October 31

· Employment Cost Index – Q3 2025 (8:30 AM ET)

· Personal Income & Spending – September (8:30 AM ET)

· PCE Price Index – September (8:30 AM ET)

International

Monday, October 27

· China: Industrial Profits – September

· Germany: Ifo Business Climate & Current Conditions

Tuesday, October 28

· China: Foreign Direct Investment – September

· Eurozone: New Car Registrations, Consumer Inflation Expectations – September

Wednesday, October 29

· Japan: Consumer Confidence – October

· UK: Bank of England Consumer Credit – September

· Canada: Bank of Canada Interest Rate Decision

Thursday, October 30

· Japan: Bank of Japan Interest Rate Decision

· Eurozone: Flash GDP – Q3 2025

· Eurozone: Economic Sentiment, Consumer Inflation Expectations – October

· Eurozone: European Central Bank Interest Rate Decision

· Germany: Inflation Rate - October

Friday, October 31

· China: NBS Manufacturing & Non-Manufacturing PMI – October

· Germany: Retail Sales, Import/Export Prices – September

· Eurozone: Inflation Rate - October

As we discussed above, we have more than one-third of the Pro Portfolio’s holdings reporting next week, which also means a hefty percentage of the S&P 500’s market cap. But those reports aren’t the only ones we’ll be digging through as we close out October. We’ll continue to connect the dots across the multitude of reports, tying back what we learn to our current holdings and candidates we are putting through their paces. That means paying close attention to the likes of NXP Semiconductors (NXPI) , Corning (GLW) , Check Point Software (CHKP) , Visa (V) , Mastercard (MA) , Dominion Energy (D) , and many others.

Here's a closer look at the earnings reports coming at us next week:

Monday, October 27

· Open: Keurig Dr Pepper (KDP)

· Close: Alexandria Re (ARE), Avis Budget (CAR), Bed Bath & Beyond (BBBY), Celestica (CLS), Crane (CR), F5 Networks (FFIV), Nucor (NUE), NXP Semiconductor (NXPI), Waste Management (WM), Whirlpool (WHR).

Tuesday, October 28

· Open: American Tower (AMT), Applied Industrial (AIT), Check Point Software (CHKP), Corning (GLW), DR Horton (DHI), Herc Holdings (HRI), JetBlue Airways (JBLU), Labcorp Holdings (LH), PayPal (PYPL), Royal Caribbean (RCL), Sherwin-Williams (SHW), SoFi Technologies (SOFI), Sysco (SYY), United Health (UNH), UPS (UPS), VF Corp. (VFC), Welltower (WELL).

· Close: Booking Holdings (BKNG), Caesars Entertainment (CZR), Logitech International (LOGI), Meritage (MTH), Mondelez International (MDLZ), PPG Industries (PPG), Visa (V).

Wednesday, October 29

· Open: Boeing (BA), Caterpillar (CAT), Criteo (CRTO), CVS Health (CVS), Kraft Heinz (KHC), Masco (MAS), Radware (RDWR), Smurfit Westrock (SW), Verizon (VZ).

· Close: Alphabet (GOOGL), Carvana (CVNA), Chipotle (CMG), eBay (EBAY), Ethan Allen (ETD), KLA Corp. (KLAC), Meta Platforms (META), MGM Resorts (MGM), Microsoft (MSFT), Pilgrim’s Pride (PPC), ServiceNow (NOW), Starbucks (SBUX), Teladoc (TDOC).

Thursday, October 30

· Open: Advance Auto (AAP), Anheuser-Busch InBev (BUD), Ameriprise Financial (AMP), Comcast (CMCSA), Crocs (CROX), Eli Lilly (LLY), Estee Lauder (EL), Ferrari (RACE), Hershey Foods (HSY), InterDigital (IDCC), Kimberly Clark (KMB), Mastercard (MA), Restaurant Brands (QSR), Shake Shak (SHAK), Vulcan Materials (VMC).

· Close: Amazon (AMZN), Apple (AAPL), Cloudflare (NET), Coinbase Global (COIN), Lumen Technologies (LUMN), Monolithic Power (MPWR), Motorola Solutions (MSI), Omega Health (OHI), Reddit (RDDT), Zillow (ZG).

Friday, October 31

• Open: AbbVie (ABBV), Cboe Global Markets (CBOE), Charter Communications (CHTR), Chevron (CVX), Colgate Palmolive (CL), Dominion Energy (D), Exxon Mobil (XOM), Linde plc (LIN), Terex (TEX).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.