Weekly Roundup: A Strong Finish to September, a Nice Start to October

Here's our plan amid the government shutdown, potential for massive layoffs, and the market’s extended P/E ratio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We closed the books on the first nine months of the year Tuesday night, and as we enter October and the final quarter of the year, the market continues to chug higher. Granted, trading volumes slowed as we moved through the week, as expectations for the duration of the government shutdown that began on October 1 grew. Despite those low volumes on Friday, the S&P 500 briefly re-joined the Nasdaq Composite in an overbought condition and remained near that condition as we closed out the week.

Economic data received this week confirmed the domestic jobs market continued to cool last month despite the lack of the September Employment Report. That same data showed inflation pressures remain elevated and also reinforced our thinking that margins will be a hot topic in the coming weeks as the September earnings season gets underway.

One of our mantras has been to focus the Pro Portfolio on companies benefiting from multi-year tailwinds that are poised to deliver superior EPS growth. That remains a key strategy, but in the current environment, we will need to be extra vigilant about margin pressure for our holdings, and also the basket that is the S&P 500.

We say this because, as we close out the week, the continued climb in the S&P 500 not only set fresh record highs, but it also landed its P/E ratio at 25.1x expected 2025 EPS. That’s the same figure the S&P 500 peaked at in 2024, but the thing is, we saw another leg down in H2 2025 EPS growth expectations for the S&P this week. Per data from FactSet, H2 2025 EPS growth for that basket slumped to 5.26%, down from 8.46% at the end of June and 13.88% at the end of March.

This brings us back to our comment about margin pressure being a hot topic in the September-quarter earnings season. To the extent that more companies in the S&P are having a tougher time passing on higher input costs, the market will need to re-adjust EPS growth expectations.

How widespread that is will be determined as we move into the opening wave of reporting season. We’ll get some initial clues next week as we dig into companies that are reporting. If it becomes clear that margin pressures are going to result in EPS expectations for the S&P 500 moving lower, that could be a catalyst that removes some of the market’s gains over the last few weeks. We upped our cash position this week, and we’re watching our holdings for where some additional trimming could be in order.

Another factor that is likely impacting trading volumes is the question of whether we will see President Trump’s treat of massive layoffs comes to fruition. We’ve discussed how that could be a shutdown bargaining tool, but our focus is more on, if they come to pass, what it means for the economy, consumer spending, and the holiday shopping season. Remember, currently, roughly 2 million federal employees have been furloughed. “Massive layoffs” would only add to the number of folks tightening their belts.

Given the above, we will continue to proceed carefully with the Pro Portfolio, picking our spots in well-positioned companies as we invest for the medium to longer-term.

Enjoy your weekend, Saturday’s Signals, and Sunday’s bowl of more light-hearted fare.

See you back here, bright and early on Monday.

Catching Up on the Pro Portfolio This Week

With the end of the month Tuesday night, we can share that the Pro Portfolio’s performance in September was robust, and rose to 12.6% on a year-to-date basis from 9.5% exiting August. That strength continued to lead the Portfolio higher as we set out in October and the final quarter of the year, but compared to the larger market, our performance was restrained. Gains in SuRo Capital (SSSS) , Marvell (MRVL) , United Rentals (URI) , Apple (AAPL) , Qualcomm (QCOM) , and others were mitigated primarily by the continued weakness in shares of Dutch Bros (BROS) .

During the week, we discussed our plan for BROS shares as well as for Costco (COST) , which includes waiting to see if Trump’s mass layoff threat becomes reality. With no final word one way or the other as the government shutdown continues into the weekend, that plan remains in place.

The only trade we made this week was to take advantage of the pronounced move in Marvell shares of late, as well as the overbought condition that stretched out our position size. The slice of shares we cleaved off our position was sold at $86.47 on October 2 and generated a gain of more than 128%. As we explained in the trade Alert, we remain bullish on Marvell’s prospects given rising AI chip demand, the ramp in its proprietary AI silicon business, and increasing network capacity issues that should drive incremental demand for its Enterprise Networking and Carrier Infrastructure segments. But the size of that gain, as well as the other conditions, meant we had to bow to our Portfolio discipline.

With the proceeds from that trade, as well as dividends received this week from Meta (META) , Universal Display (OLED) , and Nvidia (NVDA) , our cash is back to ~9% of the Portfolio’s assets. While that translates into ample dry powder for us to utilize, we will continue to monitor our holdings for outsized moves higher and overbought conditions that may warrant some prudent profit-taking should the government shutdown look to run longer than expected. For context, since 1980, the average government shutdown lasted a little over eight days. Prediction market Kalshi sees the shutdown lasting between 10 and 15 days, while Polymarket sees the potential for a longer shutdown.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Goldman raised its Amazon (AMZN) target to $275 from $240, highlighting it as a preferred large-cap name, calling out the compounding tailwinds for its Advertising segment and sustained growth prospects for Amazon Web Services.

Seaport Research initiated coverage of Apple (AAPL) with a Buy rating and $310 price target.

Evercore lifted its Bank of America (BAC) target to $55 from $49, and on Friday, Erste Group upgraded BAC to Buy from Hold.

Barclays raised the firm's price target on Labcorp (LH) to $290 from $275.

Stifel raised the firm's price target on Marvell to $95 from $80 and keeps a Buy rating on the shares.

Mizuho started coverage on Meta with an Outperform rating and named it a “Top Pick.” Shares of Alphabet (GOOGL) also picked up an Outperform rating, as did Amazon.

Jefferies raised the firm's price target on Alphabet to $285 from $230 and keeps a Buy rating on the shares after the firm's Internet/Software team ran AI chatbot tests using the same 10 prompts across Google Gemini, OpenAI ChatGPT, and Perplexity.

Evercore ISI boosted its Morgan Stanley (MS) target to $165 from $150, and BMO Capital initiated coverage of Morgan Stanley with an Outperform rating and $180 price target.

KeyBanc lifted its Nvidia price target to $250 from $230, reiterating its Buy rating.

ServiceNow (NOW) shares were added to the Q4 2025 Tactical Ideas List at Wells Fargo.

Baird upgraded United Rentals to Outperform from Neutral with a price target of $1,050, up from $888.

Stifel initiated coverage on Waste Management (WM) shares with a fresh Buy rating and a $252 target.

Cantor Fitzgerald initiated coverage of Welltower (WELL) with an Overweight rating and $195 price target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, September 29: Shutdown Drama, Google, Amazon Events on Our Roadmap for the Week

Wednesday, October 1: We Have a Government Shutdown. Now What?

Wednesday, October 1: Stocks & Markets Podcast: Government Shutdowns and the Market With Louis Llanes

Wednesday, October 1: Government Shutdown Will Impact Consumer Holiday Shopping

Friday, October 3: Here's What September Services PMI Tells Us

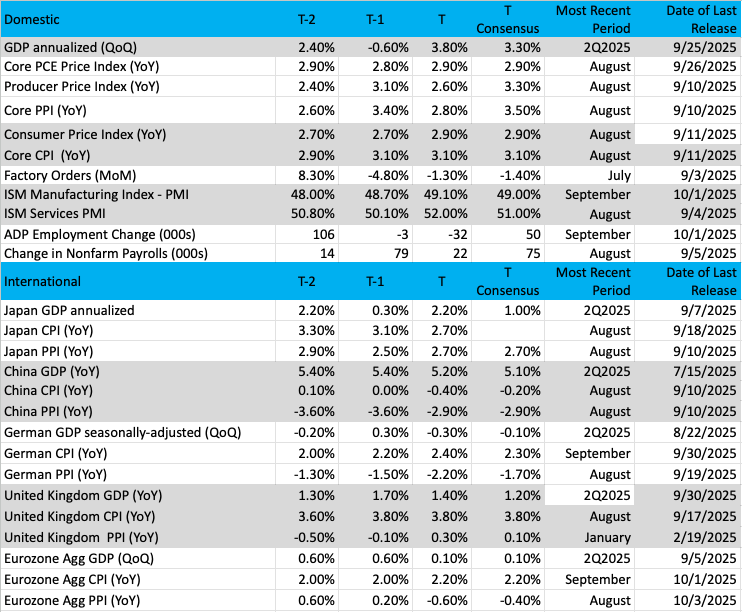

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

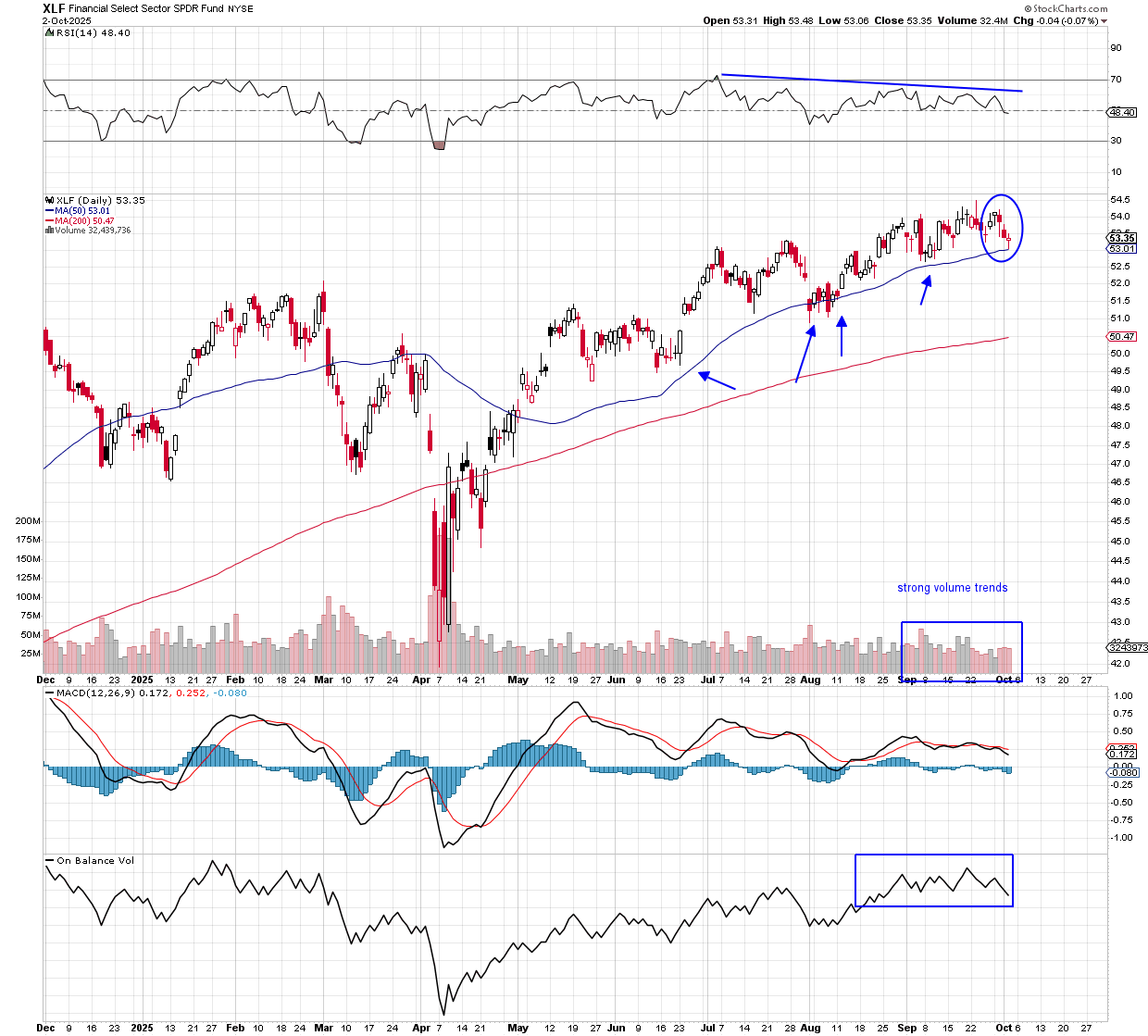

Chart of the Week: Financial Select Sector SPDR Fund (XLF)

Banks and financials will be the first names up as we kick off third-quarter earnings season in about 10 days. If you’re tracking the financials closely, it is more than just watching Bank of America (BAC) , JPMorgan Chase (JPM) , Goldman Sachs (GS) , and Morgan Stanley (MS) . The (XLF) is a great ETF for telling us how well the entire group is performing. We look at this one from time to time as it is an important gauge of economic growth and strength.

The biggest and most powerful banks in the world reside in the XLF. Its performance has been good, not great so far this year, up about 11%, which is slightly below the S&P 500 index in 2025. After a very steep drop in April, the ETF has made its way back but continues to trail the bigger growth names in technology, industrials, crypto, and precious metals.

The chart of the XLF is bullish, with higher highs and higher lows. That is our textbook definition of an uptrend. Notice the on-balance volume at the bottom is strong, with better accumulation in these banks over the past couple of months.

The XLF is right up against an all-time high, and since May, each dip to the 50-day moving average has been a place where dip buyers started buying shares. We had one of those just the other day, so why would this be any different than the prior four times? A dip to buy right before earnings season begins – it doesn’t get much better than that!

Other charts we shared with you this week were:

Monday, September 29: S&P 500 - As Doji Candle Prints, Will Markets 'Follow the Script'?

Monday, September 29: Amazon (AMZN) - A Look at Amazon as Prime Big Deal Days Approaches

Tuesday, September 30: Marvell (MRVL) - Marvell Finds Itself Back in the 'Zone'

Wednesday, October 1: Nvidia (NVDA) - Nvidia Rises to the Occasion

Thursday, October 2: Vulcan Materials (VMC) - Vulcan Makes a Bold Move

The Week Ahead

We will continue to follow government shutdown-related developments and whether the Trump administration moves forward with “massive layoffs.” Barring a resolution late Friday, the next expected vote that could end the shutdown is slated for Monday.

Below is the expected calendar of economic reports, but if the government remains shut, the number of those reports will collapse to just a few. Among them could be the Fed’s recent monetary policy meeting minutes as well as the next update to the Atlanta Fed’s GDPNow model.

We’ll give those Fed policy meeting minutes a solid read through and share any revelations that stand out, but as we discussed in Friday’s video, based on the data collected this week, odds are the Fed is still on track for two more rate cuts later this year. Given the potential lack of data, we’re likely to see the market react a bit more than usual to the aggregate comments made by Fed officials next week. Looking at the calendar, we see a plethora of appearances. Here as well, we’ll note what is said and discuss potential implications with you.

In terms of the Atlanta Fed’s GDPNow model, that rolling forecast was last updated to +3.8% on Wednesday, October 1. That update included the September Manufacturing PMI report from ISM but did not include ADP’s September Employment Change Report, the one that missed job creation expectations by a wide margin with its -32,000 print. The lack of inclusion for any September jobs data and what we saw in the September ISM Services PMI report is another reason why we will want to carefully dissect what all those Fed heads say next week.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, October 7

· Trade Balance – August (8:30 AM ET)

· Consumer Inflation Expectations – September (11:00 AM ET)

· Consumer Credit – August (3 PM ET)

Wednesday, October 8

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Meeting Minutes (2 PM ET)

Thursday, October 9

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Wholesale Inventories – August (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, October 10

· University of Michigan Consumer Sentiment Index (Prelim) – October (10:00 AM ET)

· Treasury Budget – September (2 PM ET)

International

Monday, October 6

· UK: New Car Sales – September

· Eurozone: Retail Sales - August

Tuesday, October 7

· Japan: Household Spending – August

· Japan: Coincident Index, Leading Economic Index – August

· Germany: Factory Orders - August

Wednesday, October 8

· Japan: Eco Watchers Survey Current & Outlook – September

· Germany: Industrial Production - August

Thursday, October 9

· Japan: Machine Tool Orders - September

The pace of quarterly earnings picks up next week. We’ll scour comments from those that are reporting and reflect on implications for our holdings. Given our comments about margins and what’s unfolding between input pressure and the lack of output pricing gains, we will be closely watching margin guidance for the current quarter.

With Delta Air Lines' (DAL) results and guidance, we’ll be collecting what it says about travel, noting the differences between premium vs. economy spending and domestic vs. international travel. Those insights and the ones from United Airlines (UAL) on October 16 will help set expectations for American Express’s results on October 17. We suspect the vast majority of the attention will be on the company’s Platinum card refresh and expected trends in both cards in force and average feed per card.

As it relates to our AI and data center-related holdings and a few others, we are likely to get September revenue reports from Taiwan Semiconductor (TSM) and Foxconn next week. Those reports tend to be “just the facts,” but quarterly results from both and an updated outlook are just around the corner. And with BlackRock’s (BLK) Global Infrastructure Partners reportedly closing in on a $40 billion deal, the company’s earnings call next Friday could be more colorful than usual.

Next week also brings Amazon’s (AMZN) Prime Big Deal Days event that spans October 7-8. Early this week, we discussed Amazon’s updated device offerings, and on Friday, we did the same for Amazon’s increased efforts in the private-label grocery category. Next week’s event could benefit from both of those announcements, but we also suspect it will be the unofficial start of the 2025 holiday shopping season. Should Trump’s mass layoffs come to pass, our thinking is that even pulling forward holiday shopping would only become that much stronger.

As Amazon’s event gets underway, along with competing efforts by other retailers, ICSC is expected to publish its 2025 holiday shopping intentions survey. We’ll examine those insights and blend them with soon-to-be-published holiday shopping forecasts from the National Retail Federation, Adobe (ADBE) , Mastercard (MA) , Bain & Company, and others.

Here's a closer look at the earnings reports coming at us next week:

Monday, October 6

· Close: Constellation Brands (STZ)

Tuesday, October 7

· Open: McCormick & Co. (MKC)

Thursday, October 9

· Open: Delta Air Lines (DAL), Helen of Troy (HELE), PepsiCo (PEP)

· Close: Progressive (PGR), Walgreens (WBA)

Friday, October 10

· Open: BlackRock (BLK)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.