VIDEO: Market Is Ignoring a Key From CPI, But We’re Not

The market might be out over its rate cut expectation skis once again.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In today’s Portfolio video, Chris Versace breaks down the July Consumer Price Index (CPI) report and why the market is reacting to the headline figures, but missing the uptick in the core CPI data.

With the Federal Reserve more likely to focus on the core CPI print, he explains why the market could be once again out over its rate cut expectation skis.

Chris also explains what we’ll be listening for today during the Oppenheimer 28th Annual Technology, Internet & Communications Conference, and quarterly results from both CoreWeave CRWV and Lumentum Holdings LITE.

Transcript

CHRIS VERSACE: Hey, everyone, Chris Versace here, Tuesday, August 12. And you've probably seen that futures, well, they turned up this morning, following the July CPI report that some would say was in line with expectations, but as we'll discuss, there are reasons to be concerned that core CPI was hotter than expected.

So let's break it down. Headline CPI came in at 2.7%, unchanged compared to the month of June, and less than the market's 2.8% expectation. Now, the market is reading that as tariffs potentially not having quite as big of a bite as many had feared.

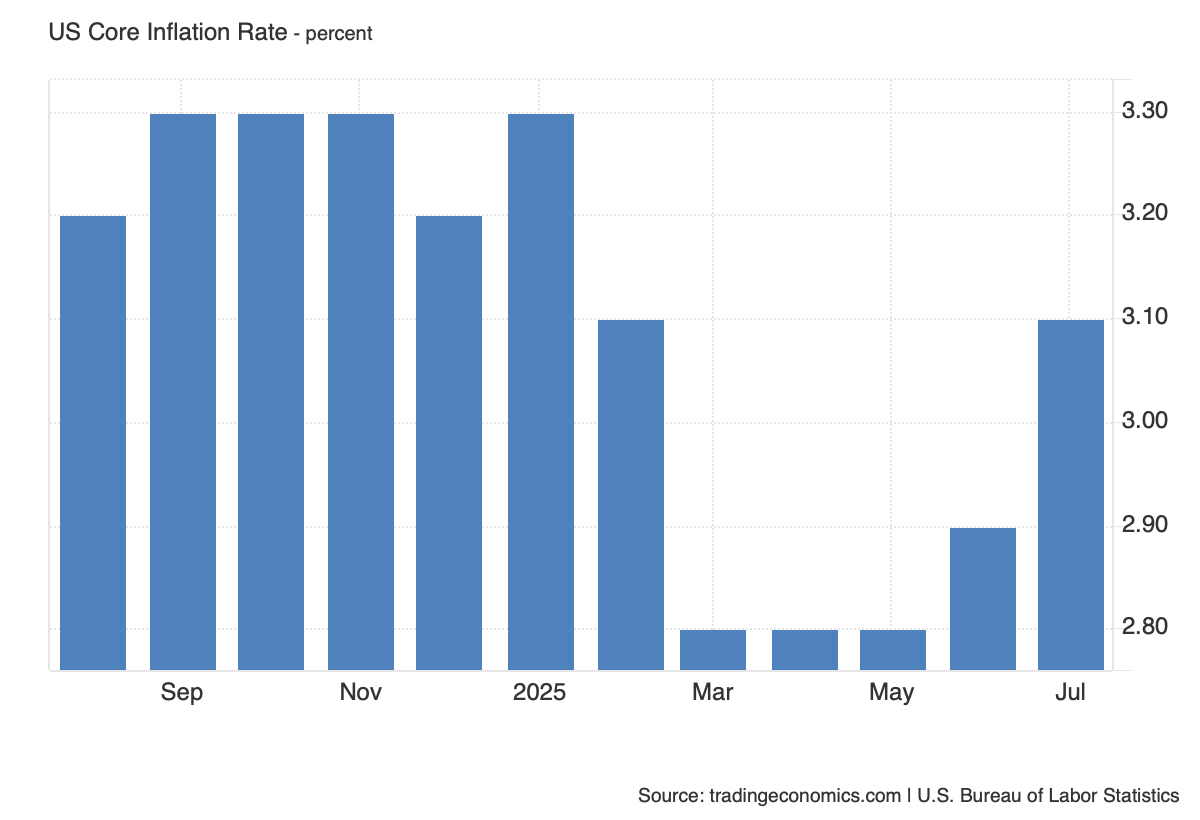

But as I just mentioned, if we look at the core CPI figures, candidly, the one the Fed is more likely to look at, it rose to 3.1% in July on a year-over-year basis. And that's up from 2.9% in June. Not only was that 3.1% figure ahead of what the market was looking for, at 3%, it was also the highest reading on a year-over-year basis since February.

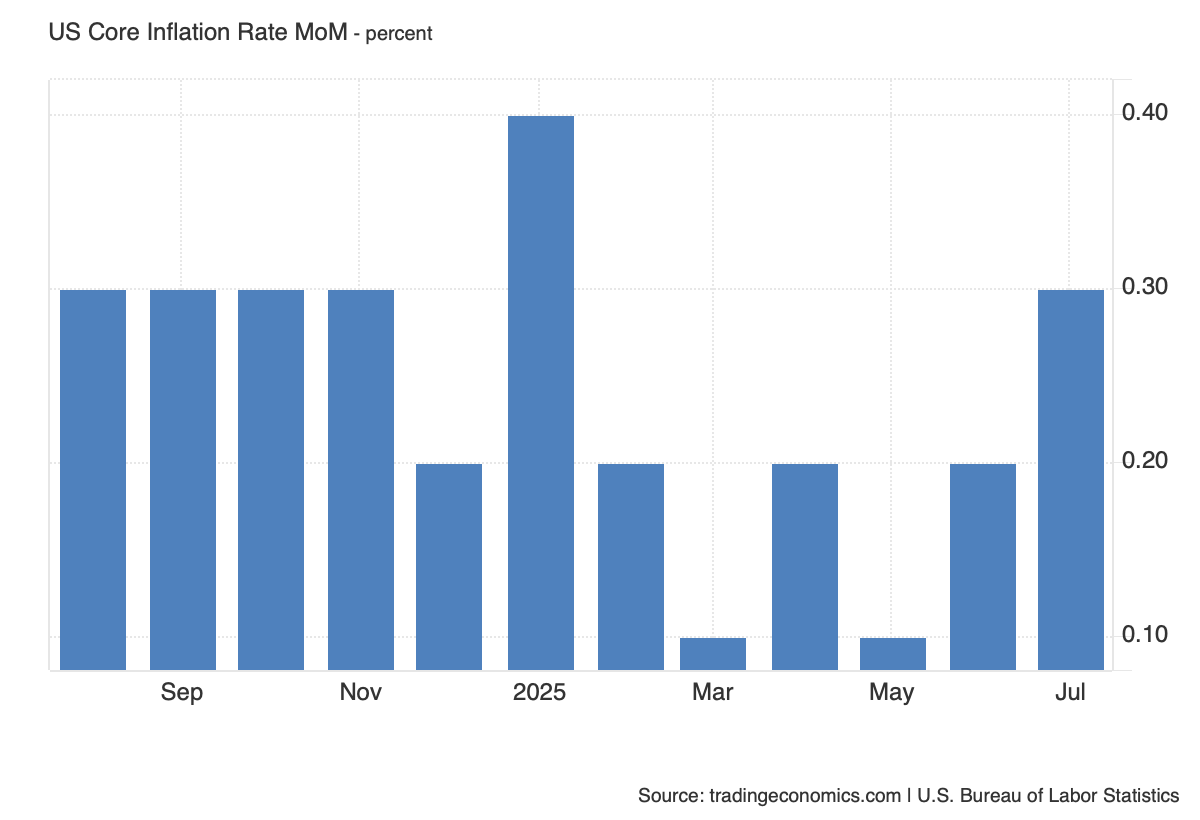

Now, if we turn to the month-over-month comparisons, I know some folks like to look at that. core CPI in July, sorry, came up at 0.3%, also the highest level in the last several months. And for context for everybody, in the alert below, you'll see the two charts. So you can see the movement in the data for yourself.

So my thinking is that while the market is enjoying the headline print, which, as we suspected it might, is benefiting from lower energy prices, odds are the Fed is going to focus on what it sees in the core readings. Now, we'll want to pay attention to what we hear today and tomorrow. We've got something like six or seven Fed speakers coming out. Some may be incrementally dovish.

But when we look at this data, especially the core CPI data, odds are they're going to be incrementally hawkish when it comes to talking about the future of monetary policy. Remember, the market is really keyed in on a September rate cut. And I realize that we have a lot more data to go before we get to the conclusion of that September policy meeting, whether it's on the data about the overall speed of the economy, job creation, which we know is going to be closely watched, and other inflation data.

Now, we also have the PPI report for July coming out later this week. And remember, the market is really starting to focus in on what may or may not be said when Fed Chair Powell speaks at Jackson Hole a week from this Friday. But here's the thing, the day before, we are going to get the August flash PMI report.

Now, that comes from S&P Global. And it's going to tell us a lot more about the pace of the economy, not only in the month of August, but really, for the current quarter. So far, when we take a look at GDP expectation models, including the one from the Atlanta Fed, still north of 2%. So our thinking continues to be that with the market moving higher this morning, looking at past that 6,400 level that we talked about on last week's podcast with Jay Woods, with the VIX falling below 16, we could be potentially setting up for the market having to revisit that expectation for a September rate cut.

It could slip to October. It could slip to later in the year. From our perspective, we're going to continue to let the data tell us what we think is likely to not happen, avoiding that mistake of superimposing what we want the data to say. That's been how we've managed the portfolio. We're going to stick to that.

It tells us when the market might be potentially out over its skis with its expectations. And candidly, that could be where we are once again with a September rate cut. But again, upcoming data will really determine that.

Now, as we watch the market move higher, we will continue to take a, as I say, careful footing. We have a lot more stuff going on this week. We also have several things that we're going to want to pay attention to today. Remember we discussed in Alert with you yesterday that we have the Oppenheimer 28th Annual Technology, Internet, and Communications Conference going on today.

And our own Qualcomm and Universal Display will be presenting among a host of other companies. We expect a lot of data points to come out of this. We're just about at that halfway mark. So an update on the current quarter, any other comments about the second half of the year, where is demand continuing to remain strong?

What are we hearing on inflation component side? All of these things, we'll be paying attention to those comments today and tomorrow. We also have after today's market close, CoreWeave is reporting. Now, directly, we have no exposure in CoreWeave. But you know indirectly, we do have one through our position in SuRo Capital.

My expectation is that CoreWeave should put up a good report. Remember that key customers, really Microsoft. But they have a growing relationship with Alphabet. They have signaled rising capital spending levels in the back half of the year and most likely into 2026. They continue to need additional AI and data center capacity. That is where CoreWeave comes in.

We also have quarterly results after the close from Lumentum Holdings. Now, this is a data center component company. The thing we'll be paying attention to is what they have to say. Because in June, they upped their guidance for the June quarter, saying that they now expected $465 to $475 million in revenue. That was up from $440 to $470 million previously.

But here's the thing, in the year ago quarter, June 2024, they posted $308 million in revenue. So no matter how you slice it, whether it was the existing guidance or the upsized guidance, strong growth on a year-over-year basis, very positive for the AI data center trade.

So what will we be watching in both the CoreWeave and Lumentum quarterly results? Well, do we get a beat and raise set of guidance reports from these companies? If we do, and then we layer in what we heard from Taiwan Semiconductor last week about their July revenue, Foxconn about their July revenue, and yesterday from Micron that upsized its outlook, it's going to be another set of data points that confirms the AI data center trade is on.

As we digest those comments from today and after today's market close, we are also going to be mindful of what we hear tomorrow at the JPMorgan Hardware Semi and Management Access Forum. When you put it all together, I suspect by the end of this week, possibly early next week, we will be revisiting several price targets in the portfolio.

Likely suspects, NVIDIA, Marvell, potentially Eaton, and a few others. So that is what we'll be paying attention to today, and again, tomorrow. We'll also keep our minds on the portfolio. If you saw yesterday, we downgraded the shares of Vulcan Materials because the continued strength in the shares has them approaching our price target.

We continue to like Vulcan Materials. We do see further upside. But remember, in keeping with the 2 rating, to commit fresh capital, whether it's for the portfolio or for members, we would want to see either positive data points that force us to revisit that Vulcan Materials price target or a pullback to an acceptable level where the risk/reward is a lot more favorable to put fresh capital to work.

So as you can see, my friends, we have a lot more coming at you today. Please be sure to check your emails, your alerts. We want to make sure you're getting all our thoughts. And if we make any moves with the portfolio, we want to make sure that you are right there with us. Thanks for watching.