VIDEO: Hot CPI Knocks Back Rate Cut Hopium

Plus, Trump squawks for lower interest rates, Super Micro’s forecast and earnings we’re watching.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In today’s Daily Rundown video, Chris Versace reviews the hotter-than-expected January CPI report, calling out how it is not constructive for rate cuts and its timing also precedes recent tariff announcements.

We continue to see a potential showdown between President Trump and Fed Chair Powell on the horizon, especially as Trump continues to call for lower interest rates, something the inflation data doesn’t support.

Chris explains what we’ll be watching for when Powell gives testimony again on Wednesday.

Turning to stocks, he recaps quarterly results from Super Micro Computer SMCI and how they set the table for Nvidia’s NVDA upcoming earnings report. Chris also shares his thoughts on Dutch Bros BROS ahead of Wednesday night's earnings report and explains why we’ll be focusing on Cisco’s CSCO earnings report after the day's market close.

Transcript

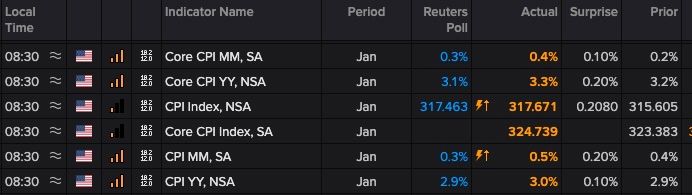

CHRIS VERSACE: Hey, everyone. Chris Versace here, Wednesday, February 12. And we've been waiting for the January CPI report, and boy did it come in not only hotter than expected, but hot across the board. We're focusing primarily on core CPI, and it did not dip as the market expected on a year-over-year basis. Rather, it rose to 3.3% on that basis, up from a figure of 3.2% in December.

So clearly disappointing. But when we take a look at the figures for September, October, November, all in the 3.3% range, and we see that again in January, it tells us that there has been very little progress on inflation. From our perspective, does it reaffirm our view that the Fed is likely to deliver any next rate cut in the second half of the year?

Yeah, that's increasingly likely, in our view. Clearly, today's data is not constructive, but we knew this was likely. Remember, we've been talking with you about the data that we saw earlier this month, whether it was the PMI data from ISM and the prices, or it was the wage data that we saw in either the ADP employment report or the January employment report, but other indicators as well. So remember, we're not surprised, and it's part of the reason why we opted to take out the inverse ETF positions in the portfolio, along, of course, with the unknowns regarding Trump-related tariffs.

So what we're going to do next? Well, we're going to listen to what Fed Chair Powell has to say at 10:00. This is his second day of testimony. But as we argued with you yesterday, we think today will be far more important because of this morning's data.

Could Powell tip the Fed's hand? Not likely. Do I think they're likely to say, or do I think Powell is likely to stick with the notion that the Fed is going to be cautious, need to see more good data? Could he reiterate that inflation remains elevated, as he did yesterday? I think those are all possibilities.

But I think we'll have to be very careful dissecting his tone, his choice of language. Those are the tea leaves that we have to read when it comes to the Fed Chair. But we will have other Fed speakers making the rounds today, so their comments might be a little more incrementally helpful, shall we say. So we'll be paying close attention to them as well.

Again, this data and the Fed's stated need to see sustained improvement, we're likely to see the market's expectation for a June, July rate cut just get pushed into the back half of the year. Again, that's what we've been expecting. Now, we also are going to be on guard today from any word on reciprocal tariffs from President Trump. And once we have the details, we'll be able to kind of puzzle through the different scenarios.

But remember, today's January CPI data does not include any impact of recently announced tariffs and reciprocal tariffs. So the odds of us seeing a dip in inflation in February, mm, questionable at best. And again, I think this plays into the scenario that any Fed rate cuts are likely to be in the second half of the year.

But no surprise, we are seeing Trump kind of come out today and saying that interest rates should be lowered to go hand-in-hand with his tariffs. Now you're probably sitting back going, a few weeks ago, Chris, you said that we could have a potential standoff between President Trump and Fed Chair Powell. I think that's increasingly likely. It's something that's going to keep the market very volatile, especially if both stick to their guns.

And for us, it's just more of a reason to stick with our inverse ETF positions. Now we're going to have a lot more coming today on Powell's testimony, breaking down his language. But we will also be discussing any incremental news on those potential reciprocal tariffs from President Trump should he choose to announce anything today. But with that, let's turn to SuperMicro Computer. This company isn't in the portfolio, but it is one that we watch very closely given its relationship with NVIDIA.

Last night, the company reported preliminary revenue for its latest quarter between $5.6 and $5.7 billion, up 54% year-over-year. Here's the key, AI-related platforms contributed over 70% of revenue in the quarter. So we look at the size of that revenue composition and the year-over-year figure, that's another data point that tells us that the AI arms race is proceeding.

SuperMirco also shared that they see 2025 revenue between $23.5 and $25 billion this year. That, when you parse the numbers, suggests a stronger second half of the year, roughly up 9% at the midpoint of their guidance. That also kind of ties with the expected ramp in spending that we're hearing from big tech, but also the maturing of NVIDIA's Blackwell production.

Now, I will say this. We know that SuperMicro has had some auditor issues over the last year. So are we going to take their actual forecast figures lightly? Yeah, we will. But directionally speaking, it matches the spending and the expectations that we've been kind of formulating based on what we've been hearing and learning, either from company earnings calls or third party data about the continued growth in AI and data center.

I also think that when we step back, we can say that SuperMicro's outlook also sets the table for NVIDIA's quarterly earnings call that's going to happen on February 26. And again, that call, the big focus is going to be on Blackwell and expectations for the coming year.

Coming up this afternoon, we do have quarterly results from Dutch Bros and Trade Desk. And we'll have some preview comments out later today. But I just wanted to say that with Dutch Bros, we continue to like the West to East expansion and the prospects for further ticket growth as they expand their food portfolio. I will say, however, that Dutch Bros, they do have an Investor Day on March 27.

So when it comes to management discussing the outlook on tonight's earnings call, I wouldn't be surprised if they're not as forthcoming as usual, perhaps deferring to that event on March 27. We've seen other companies do this, most recently Qualcomm. And remember, Qualcomm's Investor Day really broke down their diversification strategy to a very granular level. That was very helpful, very reaffirming for us. I wouldn't be surprised if we see something very similar for Dutch Bros.

What I can say is that coming out of tonight's earnings, odds are we'll be revisiting our price target. And based on that, we'll be revisiting our rating on the shares as necessary. But we'll be sharing those thoughts with you early tomorrow morning.

Also, after today's close, we do have Cisco reporting. We are going to be very interested in its comments about digital networks, capital spending as it relates to Marvell, but also as it kind of reaffirms our thesis that AI adoption across the enterprise and with consumers is going to drive network capacity bottlenecks, fostering incremental capital spending. I'd also say, folks, remember, today is Wednesday.

That means after the close-- boy, it's going to be busy after the close-- we are going to have office hours in the forum before 4:00 PM and 5:00 PM. And just a little preview, tomorrow, "The Streets" Conway Gittens will be putting me through the paces as we review the market, the economy, and yes, the portfolio in our latest quarterly call. We will have details on that out later today, but rest assured you will be able to watch that from the Portfolio page.

So going to be a busy day. A lot of exciting stuff. Please be sure to read your emails and your Alerts. We want to make sure you're getting our latest thoughts. And if we make any moves with the portfolio, we want you right there with us. Thank you for watching.

At the time of publication, TheStreet Pro Portfolio was long NVDA and BROS.