VIDEO: Here's What September Services PMI Tells Us

Let's breaks down the report from ISM and connect the dots.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In today’s Pro Portfolio video, Chris Versace follows up on our opening comments and breaks down the September Services PMI report from ISM. Chris explains why the continued softening in the employment market is likely to be held in check from an additional rate-cut perspective due to services price pressures ticking higher in September.

What we saw in the two September Services PMI reports on the pricing front reaffirms our view that margins will be a focal point of the upcoming September-quarter earnings season. Chris discusses how we’ll be tracking that concern next week, and why the S&P 500, having moved into an overbought condition, will keep us on the sidelines while we wait to see if President Trump’s “massive layoffs” threat becomes reality.

Transcript

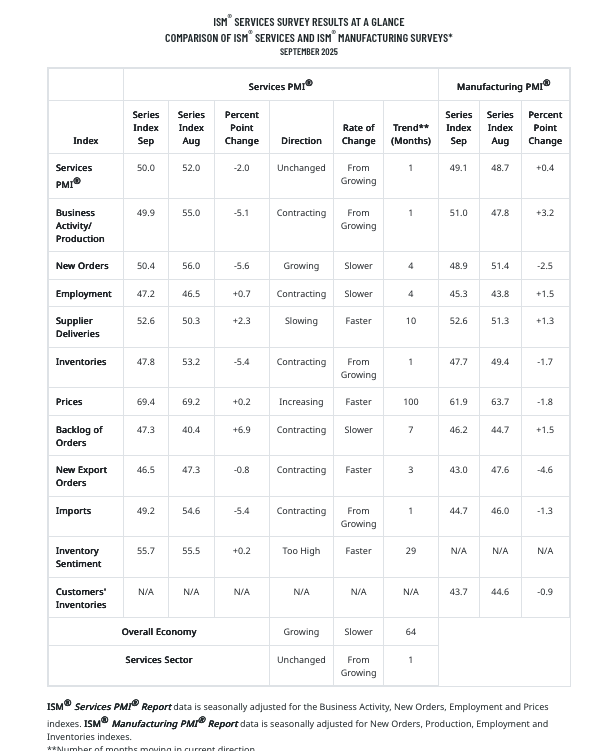

CHRIS VERSACE: Hey, everyone. Chris Versace. It is Friday, October 3. We are closing out the week. And I wanted to spend a few minutes with you just going over the September Services PMI Report from ISM. As I discussed in our opening comments today, this is really going to be the big economic data point, arguably, as we close out the week. The why on that-- services accounts for 85.9% of GDP. And absent the September employment report because of the government shutdown, we are going to, as I said, lean more so into this report than we have in the past. I suspect that others are doing that as well.

So let's just take a quick look at it. Headline-- services PMI fell to 50, which is even with the expansion-contraction line. That's down from 52 in August. Breaking it down, we did see some declines also in the new order activity, a harbinger of economic activity to come for this particular part of the economy. That fell to 50.4% from 56%.

Now, what I said to you about new orders in the past is that this is going to give us an indication of how we're likely to start off the current quarter. Remember that we have seen, of late, rolling GDP forecasts move higher. That was the Atlanta Fed GDPNow model. It was at 3.9%, likely to tick a little lower after today's number.

The New York Fed cast up to 2.5% GDP for the September quarter. The December quarter, we could see this number take it a little lower. But I would argue that the new order data is going to impact expectations for how we start the current quarter from a GDP perspective. So just something to be mindful of. There was a lot more data coming. We don't want to read into any one data point, but this is a pretty important one nonetheless.

On the topic of employment and inflation, the two things that the Fed and we, therefore, continue to focus on, when we look at employment, that actually ticked a little higher to 47.2 in September, up from 46.5 in August. Now, Chris, this is below the expansion-contraction line of 50. Yes, it is. And it says that employment is just contracting slightly slower than it did the prior month. This is going to be our proxy, because remember, no September employment report.

This is going to signal that the employment market continues to remain very weak. If you think about some of the other numbers that we got-- the Challenger Job Cuts Report for September, the ADP Employment Report for September-- it all kind of triangulates around telling us that the employment market continues to be challenging.

Our thought on this is that it could get more challenging if we see the White House move forward with these mass layoffs. As I talked about the last couple of days and again this morning, this is going to be something that we are watching very closely, especially over the weekend. Maybe there's some deal to help end the shutdown, but if not, does the White House go forward with these mass layoffs? What are the impacts for the economy, consumer spending, and, of course, the all-important holiday shopping season? These will be the things that we are watching.

The question, though, is, did we see the jobs data roll over so much that we're likely to see the Fed do a little more, potentially, at its October monetary policy meeting? And yes, the employment numbers have continued to point to a contracting market for that. That's some of the pain that Fed Chair Powell said we might have to feel. But the issue is inflation.

When we look at the price component in the September, services PMI, it ticked higher to 69.4% from 69.2%. If you saw the alert this morning, you saw the chart that we shared. And this tells us that when we add in that September figure, that inflation pressures remain at elevated levels.

But here's the thing. When we talk about the difference between input prices and output prices, the S&P September services PMI said that it saw output prices continue to soften a little bit. This is what we saw in the Manufacturing PMI Report for September a couple of days ago as well from S&P. This reaffirms our view that margins are going to be a big, big talking point in the September quarter earnings season.

This means that as we start to see companies report ahead of the pack, like the ones that we'll see next week, we are going to be very mindful of what they say not only about their margins for the September quarter, but the margin guidance for the final quarter of the year. Now, as we think about all of that, the yin and the yang between the employment and the pricing data, they're likely to cancel each other out to some extent, which likely means that the Fed is still on track to deliver two incremental rate cuts that were penciled in in the latest set of economic projections. However, again, we have to be mindful that if we do get these mass layoffs, that could be a change in expectations for what the Fed is likely to do, all the more reason for why we will be really focusing in on that over the weekend and over the next couple of days, again, to see if they really happen.

I will share, too, that the continued strength in the market that we're seeing this morning now has the S&P 500 once again back in an overbought condition. The comments that we made this morning about the NASDAQ being in that overbought condition and now the S&P 500, that is going to keep us on the sidelines in the near term. I know that there are some stocks that we've been talking about-- Costco, Dutch Bros-- that we are closely following. But with the overbought condition and the potential for those mass layoffs, things could get a little bumpy next week, hence our decision to ring the register in a very profitable way yesterday with the shares of Marvell.

Now, we've built up our cash a little bit. We will have some opportunities to pick things up. We have our shopping list. Yes, Costco, Dutch Bros are on there. We know we would like to pick up some additional shares of Welltower. If we see the market pull back, that could bring some other opportunities as well. We will be examining some of them and hopefully discussing them with you in the coming days.

If the opportunity presents itself, we might need to move a little quickly on one or two of them, maybe. So don't be surprised what happens, should it happen, in the coming days, again, if we see those layoffs and we see the market respond. If we don't get the layoffs, the market could embrace that. It could be a sign that we're closer to the government shutdown being averted, and that could help us move higher. But then we've got to pay very close attention to margins and what that means for the September quarter earnings season.

So a lot going on as we come back with you next week. So please, folks, be sure to check your emails, your alerts. We want to make sure that you are getting all our latest thoughts. And, of course, if we make any moves with the portfolio, we want you right there with us. Coming up today, we will have some more comments. We'll also have our weekly roundup. And over the weekend, we will see the return of our Signals Alert on Saturday and a little more light-headed fare on Sunday. Yes, the Sunday Soup makes a return as well.

Enjoy the weekend. We'll see you back here on Monday, primed and ready.