Updating Our Portfolio Game Plan as Auto Tariffs Mean More Uncertainty

Here's our plan for one holding this morning, and how a contract decision could impact another position.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Early this morning, equity futures are mixed following President Trump announcing plans to impose 25% tariffs on “all cars that are not made in the United States” and “absolutely no tariff” for cars that are built in the U.S.

That sure sounds to us like a stick designed to drive car companies to build autos in the U.S. This is a good idea in principle when it comes to jobs but one that if successful, will be measured in years not months. Near-term, though, it’s another headwind for earnings expectations and not just for companies such as Stellantis STLA, Volkswagen VWAGY, and other Asian or European car companies.

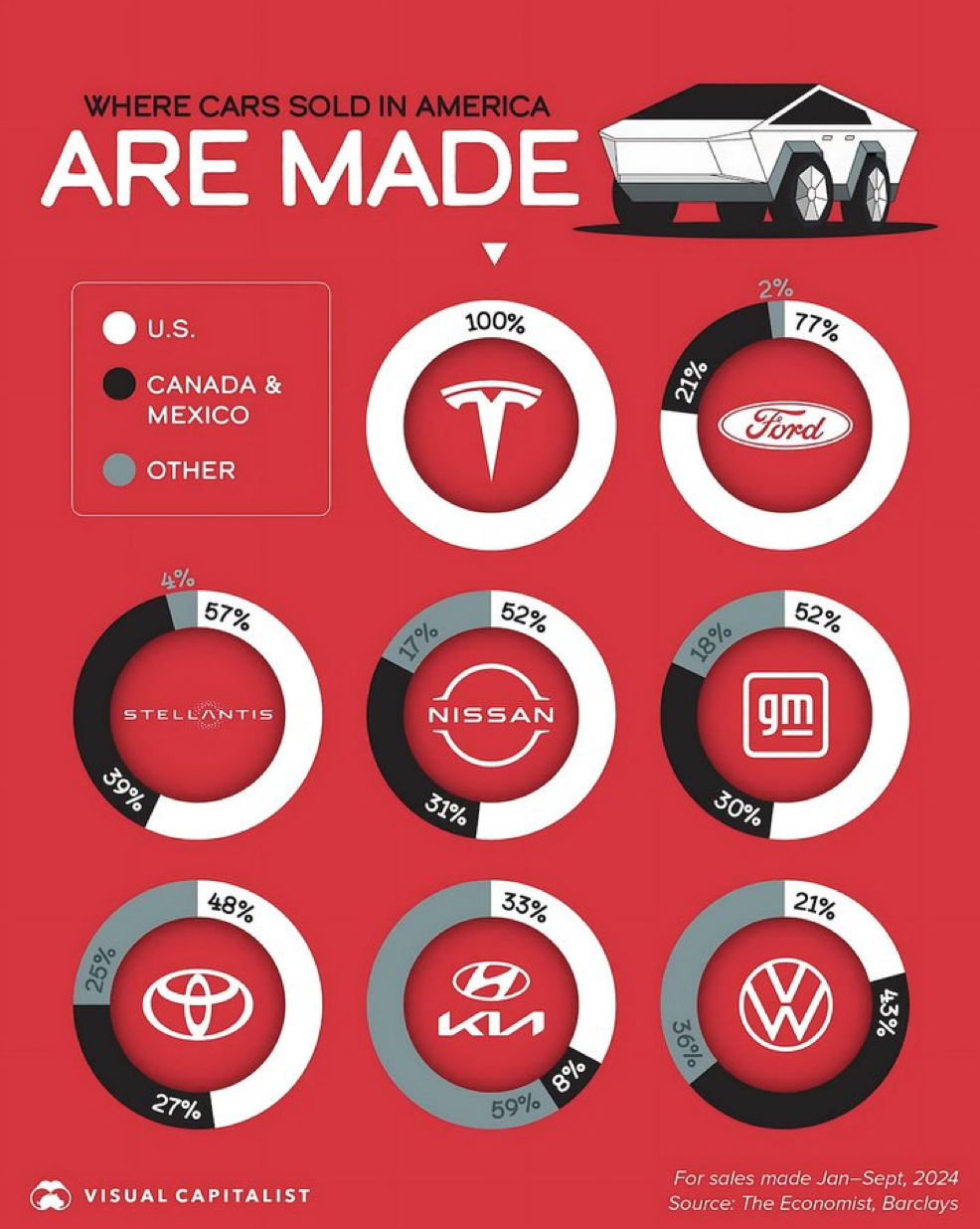

As we can see in the graphic above, General Motors GM and Ford Motor F won’t escape unscathed. And with tariffs expected on both finished automobiles as well as auto parts starting on April 3, it’s a pretty safe bet that margin and EPS expectations will be dialed back in the coming weeks for auto OEMs and their suppliers. As nearly half of all vehicles sold in the U.S. are imported, per findings from S&P Global Mobility, as well as nearly 60% of the parts in vehicles assembled in the U.S., there is a high degree of certainty vehicle prices will get pushed up in response.

Potentially aiming to soften the blow, Trump continued to ssay that while his expected reciprocal tariffs slated for April 2 will be on all countries, they will be “very lenient.” Exactly what that means will be laid out next week, but the other outcome to all of this we’ll be watching for is the response from Canada, Mexico, the European Union, and others.

This is where things will get tricky because Trump has already suggested further tariffs would be imposed on the EU and Canada if they worked together “to do economic harm” to the U.S. That sure sounds like the potential for tariff escalation to us, and that would only bring more uncertainty about the economy, inflation, and Fed policy — and also for corporate earnings prospects.

Planning to Exit Remaining Mastercard Position

The next few days could bring a few layers of clarity, but that doesn’t mean it’s going to be positive for the market, which is once again back in "Fear" mode on the Fear & Greed Index.

The unwinding of the portfolio’s stake in Four-rated Mastercard MA has lifted our cash levels to ~8%, but when the market opens this morning, we’re planning on closing out the balance of our MA position. That should bring the cash level to around 9% and the portfolio’s total defensive positioning to about 11.3% give or take.

Our Plan for Lockheed Martin

Based on the outcome of the U.S. Navy’s upcoming next-gen fighter jet contract, we’ll revisit the portfolio’s position in Lockheed Martin LMT. Following last week’s contract loss to Boeing BA, we said that if we saw LMT shares snap back to their 100-day moving average, which now sits near $483, we would consider using the shares as a source of funds.

Given the developments of the last several days, another contract loss is going to raise more questions about Lockheed’s competitive position. Such an outcome could lower our pain threshold for the shares.

Two Fed Rate Cuts This Year?

We’ve already shared our concern over June-quarter guidance and implications for S&P 500 EPS expectations. Given the developments with Trump tariffs in the last 24 hours, and the renewed uncertainty they bring, more are likely to join us, and, in our view, it would be surprising if other Wall Street firms don’t revise their S&P 500 price targets. As they do, that's likely to keep a lid on the market but it’s not the only potential headwind.

Some would say we are seeing an earlier-than-expected departure from last week’s updated set of economic projections that included two 25-basis point rate cuts for this year. Sparking that thought, earlier this week, Federal Reserve Bank of Atlanta President Raphael Bostic said he sees just one rate cut this year. Much like we do, Bostic does not see a clear way to the Fed’s 2% inflation target ahead and he made his thinking very clear: “Because that’s being pushed back, I think the appropriate path for policy is also going to have to be pushed back.”

With those comments coming ahead of Trump’s auto tariff announcement, we’ll be curious to see what Fed speakers making the rounds today and tomorrow say. We also think that between the inflation data contained in Monday’s Flash March PMI report and tariff developments, the market is going to look right through Friday’s PCE Price Index data for February.

At the time of publication, TheStreet Pro Portfolio was long MA and LMT.