Trump's Iran Update Has Ripple Effect on Gold Share Prices

Geopolitical tensions are lifting multiple holdings in our EPS Diplomats Model.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following Tuesday's conversation with Bob Lang on the "Stocks & Markets" podcast (and it’s sweeping one you won’t want to miss), let’s take a look at the developments that are affecting the market on Tuesday morning.

As you’ve likely noticed, after opening higher, the S&P 500 has since turned and traded off. Not oh so much, but a tad in the red as the market had more time to review the December CPI report as well as quarterly results from Delta Air Lines (DAL) and JPMorgan Chase (JPM) .

Unlike most of the constituents of our EPS Diplomats model on Tuesday morning, both of those stocks are a bit deeper into the red than the S&P 500 despite reporting in-line to better-than-expected results, especially in the case of JPMorgan. We’ll dig a bit deeper into those in a follow-up alert.

Outside of those earnings reports, which we’ll discuss in a few minutes, we are seeing geopolitical tensions ramp up as central bank chiefs across the globe declare their support for Federal Reserve Chair Jerome Powell and reports Iran is “ready” should the U.S want to “test military action.”

The latter led President Trump to cancel all meetings with Iranian officials and comment that “help is on the way.” That helps explains why the shares of Equinox Gold (EQX) , IAMGOLD (IAG) , Kinross Gold (KGC) and Pan American Silver (PAAS) are moving higher on Tuesday.

We will continue to track developments on the U.S.-Iran front, gauging tensions along the way as well as the market’s reaction to earnings reports coming over the next few days. Should we need to get a bit more defensive, we will, but we also recognize that when we play the long game, short-term geopolitical drama can bring about some nice buying opportunities.

The December CPI Report

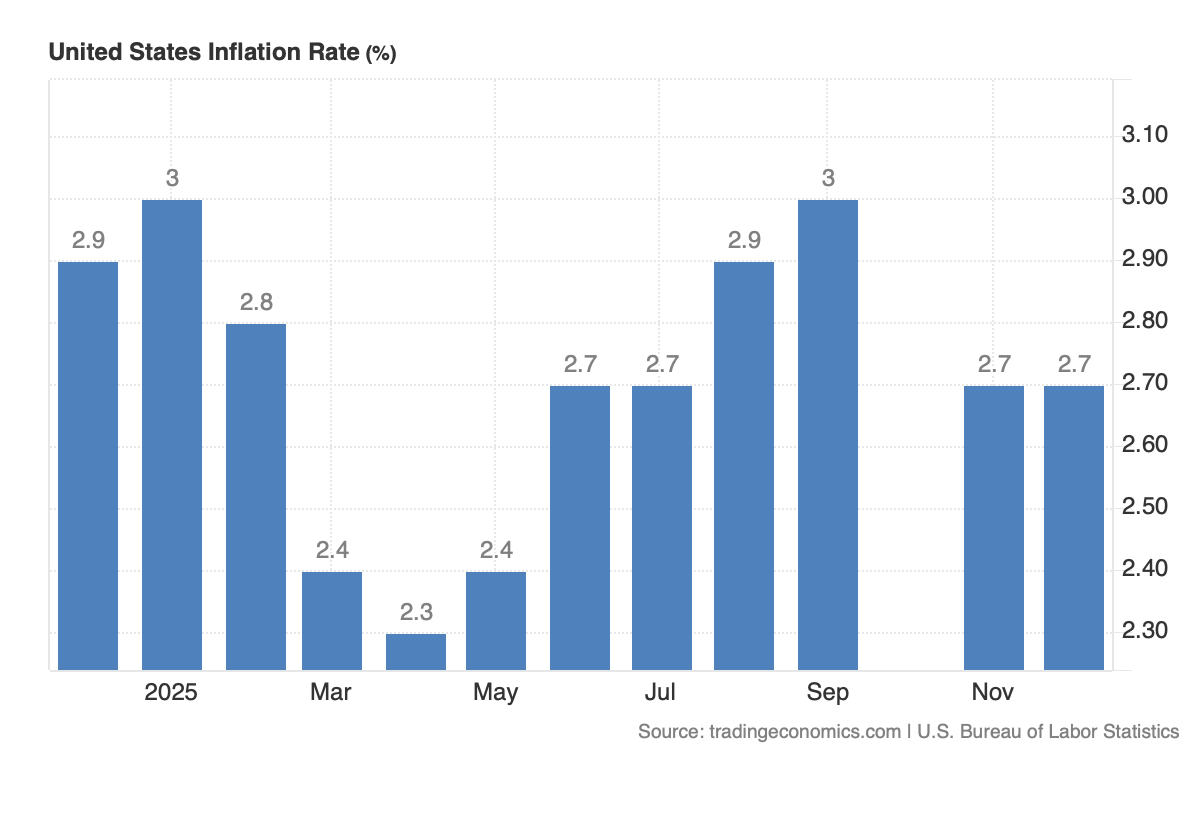

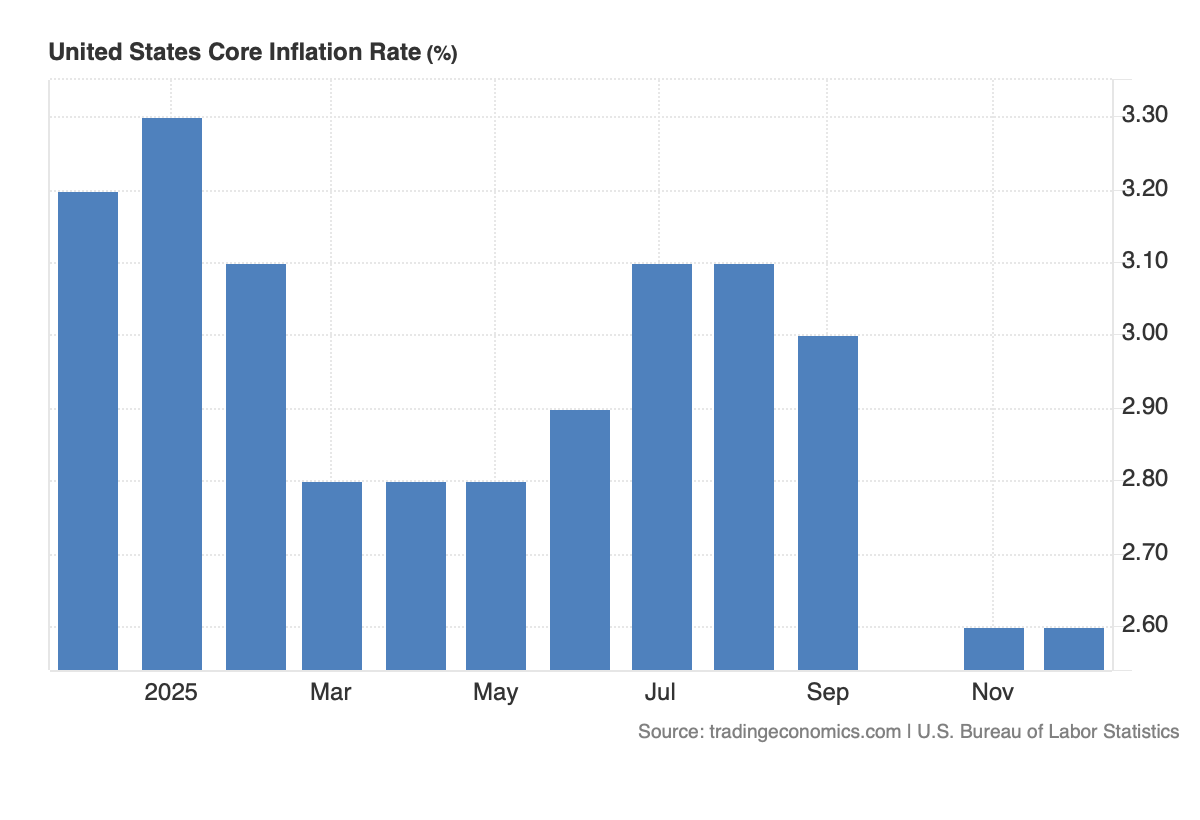

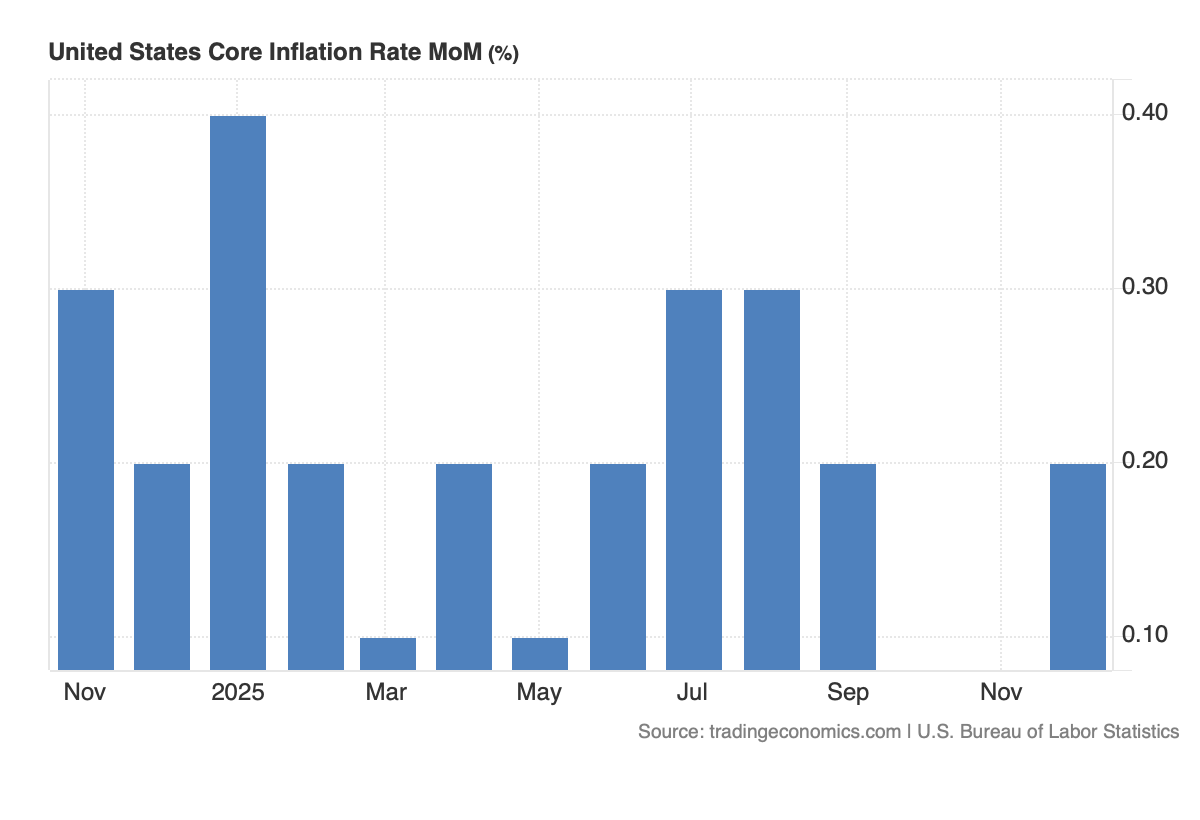

The headline figure for the Consumer Price Index rose 2.7% on a year-over-year basis, in line with expectations and unchanged compared to the November figure. The core CPI figure was also unchanged at 2.6% but it was a tick lower than the 2.7% figure the market had penciled in for December. Both metrics are still some distance from the Fed's 2% target.

In the case of both data sets, the November and December figures are below those for August and September, but as you can see in the charts below, we have some gaps in the data. Thank you, government shutdown.

Those gaps throw off the trailing three-month analysis that the Fed and we prefer.

Paired with the positive job creation for November and December depicted in the December Employment Report, the unchanged year-over-year CPI figures isn’t going to spur the Fed to do more in the near-term, especially after having delivered three-consecutive 25-basis point rate cuts. And for those wondering, the PPI reports we get for Wednesday will be for October and November, not December. More puzzle pieces to sift through but not enough to get a full picture, at least not yet.

The December PPI figure is scheduled to be published on January 30, which is past the Fed’s January 28 policy announcement.

The bottom line is that there wasn’t anything inside the December CPI report that is going to shift the market’s expectation for the Fed’s next rate cut to come in June. Remember, Powell steps down in May, and a new, and more likely dovish, Fed Chair will be in the saddle.