Trump Tariff Decision, New Data Set to Impact These Four Holdings

Following a fluid tariff decision, we'll have our eyes on this coming report as we manage the Portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

With one day to go before President Trump unveils his reciprocal tariffs, futures point to a mixed start for Q2 2025.

While Trump claims to have settled on his tariff plan, reports as to what the president could announce, reportedly at 3 p.m. ET in the White House Rose Garden, continue to vacillate between 20% global tariffs on virtually all imports to more targeted tariffs.

Our take is that the situation is fluid, and the outcome will likely hinge on last-minute deal-making attempts that would allow Trump to claim some victory on the trade front. How all of this comes together and what it means for the market is very much to be determined, but in our minds, what is just as important will be the response from those getting slapped with these tariffs. Then it becomes a question of whether Trump opts to escalate tariffs further.

If you’re a public company that has just closed its books and is getting ready to issue June quarter guidance and possibly update your outlook for 2025, what’s to come has the potential to determine if your guidance meets, beats or falls short of market expectations. As we’ve discussed, we will be keeping our eyes and ears open for any such reports, connecting the dots back to the Portfolio’s holdings as well as potential candidates.

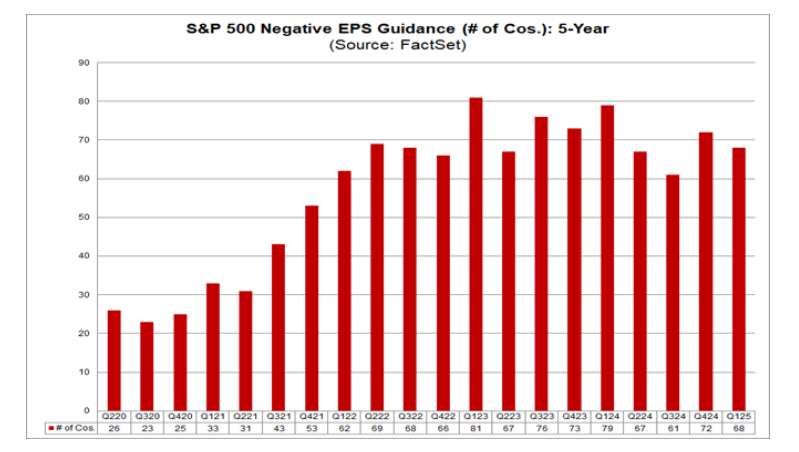

Data from FactSet shows that, overall, 107 S&P 500 companies have issued quarterly EPS guidance for the first quarter. Of those companies, 68 have issued negative EPS guidance and 39 have issued positive EPS guidance. While a tad higher compared to the five-year average, what is announced in the next few days could lead to even more negative earnings pre-announcements and fuel more questions about S&P 500 EPS growth prospects.

Typically, when that happens, folks also question the market multiple, and for reference, the S&P 500 closed last night at 20.8x expected 2025 EPS of $269.92. For inquiring minds, that’s a 7% premium to the average peak P/E multiple for the S&P 500 over the 2000 to 2024 period sans the pandemic and matches the average peak P/E multiple for the 2015 to 2024 period also sans 2020.

Because we are in the often-cited “quiet period” ahead of the March quarter earnings deluge, only one Fed official is poised to speak on Tuesday, and any earnings pre-announcement will come once we have a clearer picture of tariffs, it’s a good bet all eyes will be on the day’s economic releases. Those include S&P Global’s (SPGI) final U.S. March Manufacturing PMI, the more closely followed ISM March Manufacturing PMI, and the February JOLTs and Construction Spending reports.

We will be interested in the construction data given the Portfolio’s positions in United Rentals URI, Vulcan Materials VMC, Eaton ETN, and to a lesser extent, Waste Management WM. But, for our money, the greater focus will be on the March Manufacturing PMI reports and how they compare to the data found in the February reports. When we and others reviewed the February data, the concern was there could have been a pull forward in demand given the expected Trump tariffs at the time on Canada, Mexico and China. With Trump touting April 2 as “Liberation Day” during March, it’s quite possible the March data doesn’t fall as much as some might expect and it could surprise to the upside, likely due to more sales pulling forward ahead of unknown tariffs.

The big reveal to us will be in the new order dynamics as well as those for employment and inflation. On the one hand, because the U.S. manufacturing economy is responsible for about 15% of GDP, what we see in the March Services PMI reports for those figures will be even more revealing. However, what we see in the data will influence GDP expectations for the March quarter. Given the Atlanta Fed’s GDPNow model at -2.8% for Q1 2025 and the New York Fed’s Nowcast model at 2.86%, it’s safe to say expectations are currently all over the map.

It will start the process of refining expectations for what we could see in ADP’s March Employment Report on Wednesday, Friday’s March Employment Report and what Fed Chair Powell could say late Friday morning.

Now to see what the data says…

More Pro Portfolio

- We're Exiting This Semi-Cap Holding on Excess Capacity Concerns

- Monthly Roundup: March Lives Up to Its Reputation. Now for April...

- Energy Addiction, Walmart and Mom & Pop Cos. in AI, Luxury M&A and More Investing Headlines

At the time of publication, TheStreet Pro Portfolio was long URI, VMC, ETN and WM.