Trump Brings Renewed Tariff Uncertainty to an Overbought Stock Market

Let's discuss the implications of the latest tariff news, passage of the 'Big Beautiful Bill' and Foxconn’s Q2 & Q3 comments.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Futures indicate we will likely start post-July 4th trading with stocks giving back some of their pre-holiday gains. Markets are responding to reports that U.S. tariffs will return to April 2 levels on August 1 if there is no progress on trade deals with the U.S. President Trump also threatened an additional 10% tariff on countries that align with the “Anti-American policies of BRICS,” which refers to emerging market countries including Brazil, Russia, India and China.

Reports also indicate there are letters going out to 12 countries today outlining the various tariff levels they would face on goods they export to the U.S., with what is being called a "take it or leave it" offer. So far, the names of those 12 countries have yet to be released, but their identities are expected to be made public later today.

In addition, shares of Tesla TSLA, which account for 1.69% of the S&P 500 and 3.25% of the Nasdaq 100, are under renewed pressure this morning after Elon Musk announced the formation of the “America Party,” a move that prompted Trump to comment that Musk has gone “off the rails.”

Should we be all that surprised by the White House’s move on tariffs, as expectations for some trade deals have moved past the self-imposed July 9 deadline? We view this as Trump looking to regain control of the narrative, but like we saw back in late March and early April, it’s going to drag the markets along.

The fact the relative strength index (RSI) levels for the S&P 500 and Nasdaq Composite are sitting at 75.57 and 72.22, respectively, means the combination of developments we outlined above will, at a minimum, inject a fresh round of uncertainty into the market just as we get ready for companies to update their expectations for H2 2025.

Our view is that the potential movement on the tariff front is likely to lead management teams to skew their outlooks more to the conservative side. We’ve talked before about the decline in H2 2025 EPS growth for the S&P 500 compared to the first half, from its high near 14% exiting March to the current 8.4%. Should the initial wave of corporate guidance for the current quarter and or H2 2025 suggest that 8.4% figure needs to come down further, odds are high we’ll see at least some question the current market multiple of 23.8x.

On Thursday, we updated our shopping list for the Pro Portfolio, should we see a pullback in the market, and that list still stands. However, depending on the depth of a market pullback, we could see it grow by a name or two.

While we wait, ~12% of the Pro Portfolio’s assets in cash is a welcome buffer. We may also elect to do some prudent register ringing with a position or two whose RSI levels are deep in overbought territory, like we see with American Express AXP.

Trump’s Big Beautiful Bill and Foxconn’s Q2 and Q3 Comments

Before we close out this morning’s opening comments, there are some bright spots to share. The passage of Trump’s fiscal stimulus bill does bring some clarity on tax rates as well as increasing spending for border security, defense, and energy production. Those increases are likely tailwinds for our positions in Axon Enterprise AXON, Palantir PLTR, and, to a lesser extent, the First Trust Nasdaq Cybersecurity ETF CIBR. On the energy front, OPEC+ has agreed to larger than larger-than-expected hike in oil production, which could bring some additional relief at the pump.

We also have the latest positive data point for AI demand, courtesy of Foxconn. Over the weekend, the company said that it saw record second-quarter revenue driven by strong demand for AI products for the current quarter, AI demand contining to drive strong growth at its Cloud and Networking Products segment and improving demand for its Information and Communication Technology segment, which houses smartphones and other connected devices. Given Foxconn’s relationship with Nvidia NVDA and Apple AAPL, its comments are positive for those two Portfolio holdings, but also for Marvell MRVL, Universal Display OLED, Qualcomm QCOM, and, to a lesser extent, Eaton ETN.

Coming Up This Week

We have a modicum of earnings reports this week. We’ll be interested in what ConAgra CAG has to say about demand for its packaged food business as well as pricing. When it comes to Delta Air Lines DAL, our interest will be on domestic vs. international travel demand, ticket pricing, and travel expectations for the holiday-filled second half of the year.

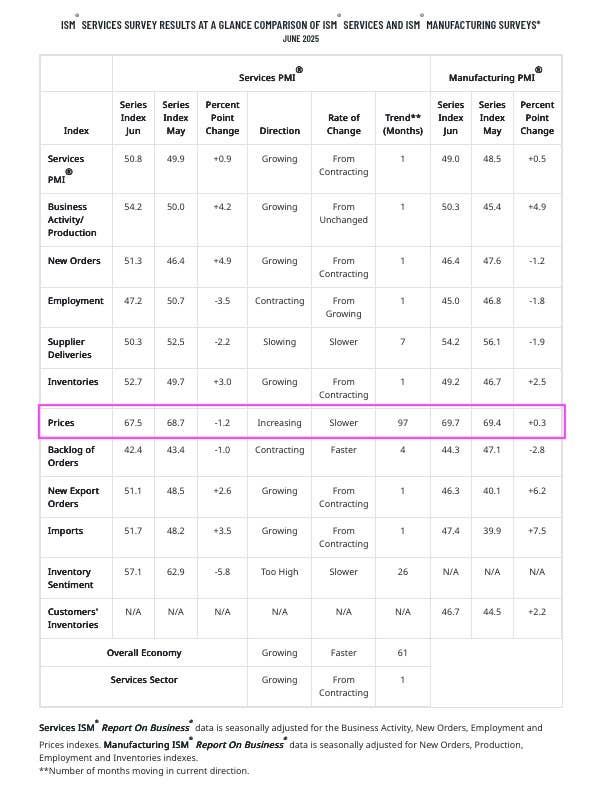

On the economic data front, the June NFIB Small Business Optimism Index is due tomorrow (June 8) as well as the May Consumer Credit report. Wednesday (June 9) brings the latest Fed FOMC meeting minutes, and while we’ll want to review them, what we saw in last week’s June Employment Report and June ISM Services PMI data, in our view, means a July rate cut is off the table.

We will continue to follow the June, July, and August data as we get ready for the Fed’s next policy meeting in mid-September, but given our comments above on trade deal uncertainty and tariffs, depending on what happens, the market may need to rethink the potential for a September rate cut.

At the time of publication, TheStreet Pro Portfolio was long AXP, AXON, PLTR, CIBR, MRVL, AAPL, NVDA, OLED, QCOM and ETN.