These Reports Should Signal What's Ahead for Jobs, Prices and Rate-Cut Possibilities

Next week will provide more data to determine what the Fed and the market may do next.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

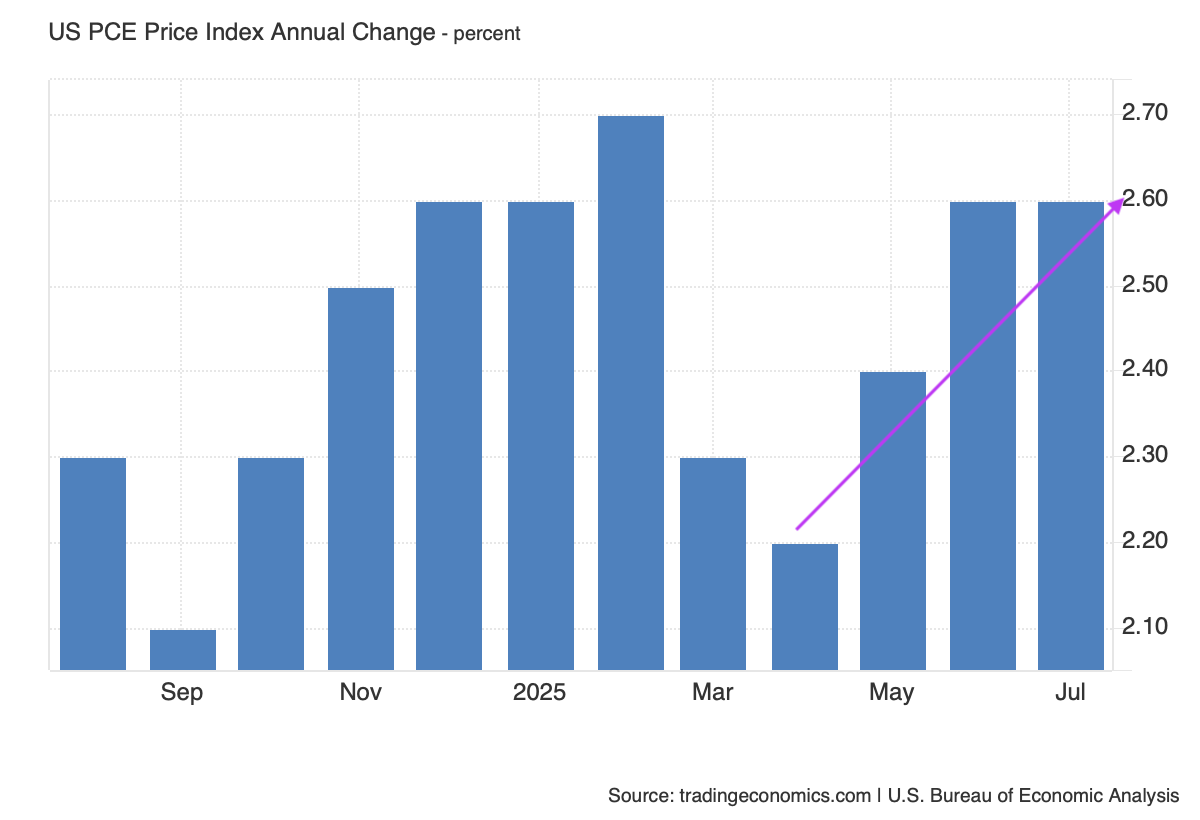

With our plan for Marvell MRVL shares in place, we’re turning our attention to this morning’s eagerly awaited July personal consumption expenditure price index data, which, across the board, matched expectations. The headline PCE price index held steady at 2.6% on a year-over-year basis, matching the June figure, and up compared to May and June.

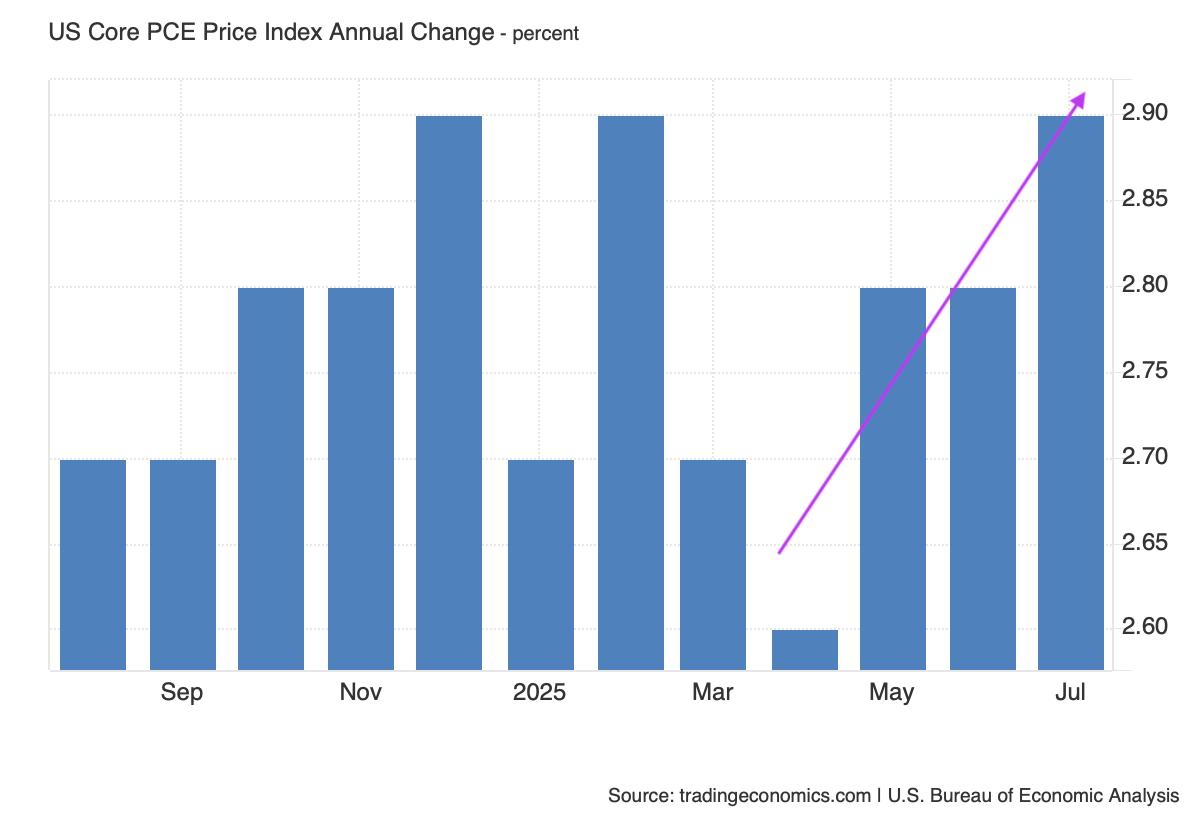

The closely watched core PCE Price Index figure for July ticked higher to 2.9%, again matching expectations. While some may sigh in relief because the July figure did not surprise to the upside like the July core consumer price index and July producer price index figures did, the direction of the core PCE Price Index over the last few months is clearly in a direction the Fed is not going to like.

Earlier this week, we said that the Cleveland Fed’s Inflation Nowcasting model saw August core PCE rising 2.95% and it now shows the cumulative figure for the September quarter at 3.06% compared to yesterday’s revised 2.5% print for the June quarter. With the July core PCE Price Index in hand, the Cleveland Fed’s August forecast, it’s implied that the regional Fed bank’s model sees another leg up in September to around 3.3%.

Helping support that view, this week, companies including Hormel Foods HRL, J.M. Smucker SJM, and Ace Hardware said they would raise prices for reasons ranging from higher meat costs to tariffs. That adds to a list that already includes Walmart WMT, Target TGT, and Best Buy BBY.

On that point, Walmart CEO Doug McMillon commented that, “… as we replenish inventory at post-tariff price levels, we’ve continued to see our costs increase each week, which we expect will continue into the third and fourth quarters.”

As we game that out, we’ll be interested in holiday shopping forecasts that should be published in the coming weeks. Higher prices could be a headwind for consumer spending, but flipping that around means value-conscious shoppers will continue to flock to Costco COST, TJX Companies TJX, and Amazon AMZN.

Big week of data ahead, with potentially big Fed implications

Before we get too far ahead of ourselves, we and the market will be focused on what next week’s August data has to say about the pace of job creation and inflation. If the data found in the ISM Manufacturing and Service PMI reports for August, ADP’s August Employment Report and the Bureau of Labor Statistic’s August Employment Report mimic what we saw in the August Flash PMI data from S&P Global, the market may need to reconsider Fed Chair Powell’s Jackson Hole comment that depending on what happens and what is seen in the data, the Fed’s policy stance “may warrant adjusting.”

While next week is an abbreviated one for the markets, it will be an important one given the market’s high expectation for not only a September rate cut but follow-on ones exiting the Fed’s October and December meetings as well. While the Volatility Index (VIX) has jumped today, its current level and the Fear & Greed Index flashing “Greed” tell us there is room for the market to be rattled by what next week’s data could mean.

We’ll break down the data piece by piece, sharing what it means for the market and the Fed. If needed, we’ll make prudent moves where necessary as we continue to manage the Portfolio for the longer-term.

At the time of publication, the Pro Portfolio was long MRVL, COST, AMZN, TJX.