Stagflation Worries Grow on New Personal Consumption, GDP Data

Let's dig into the numbers to see what could be ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Behavioral Change and the Economic Recovery

Behavioral Change and the Economic Recovery

When we look at the downward revisions for the fourth-quarter 2025 gross domestic product and the continued tick higher found in the year-over-year January Core personal consumption expenditure price index figure, we would not be surprised to see more rumblings of potential stagflation. By the book, stagflation is a condition when we have a combination of three things: high inflation, high unemployment, and stagnant demand or low growth. Let’s examine recent data for each of those.

In the chart above, we can see the recent uptrend in the closely watched core PCE price index over the last few months, but if you look closely, you’ll see the December and January figures of 3.0% and 3.1% are the highest since March 2024. In our opening comments this morning, we explained why, in our view, the upcoming Flash March data will be of even greater interest than this latest January reading of the Fed’s closely watched inflation indicator.

If you’ve looked at the CME Fed Watch Tool of late, the one that tracks the market’s expectation for the Fed Funds rates and rate cut expectations, those inflation figures and recent escalation in energy prices we’ve talked quite a bit about with you have pushed out rate-cut timing expectations. The next cut per the CME’s tool isn’t expected now until December 2026 – a month ago, it was expected at the Fed’s June policy meeting, the first one expected to be chaired by Kevin Warsh.

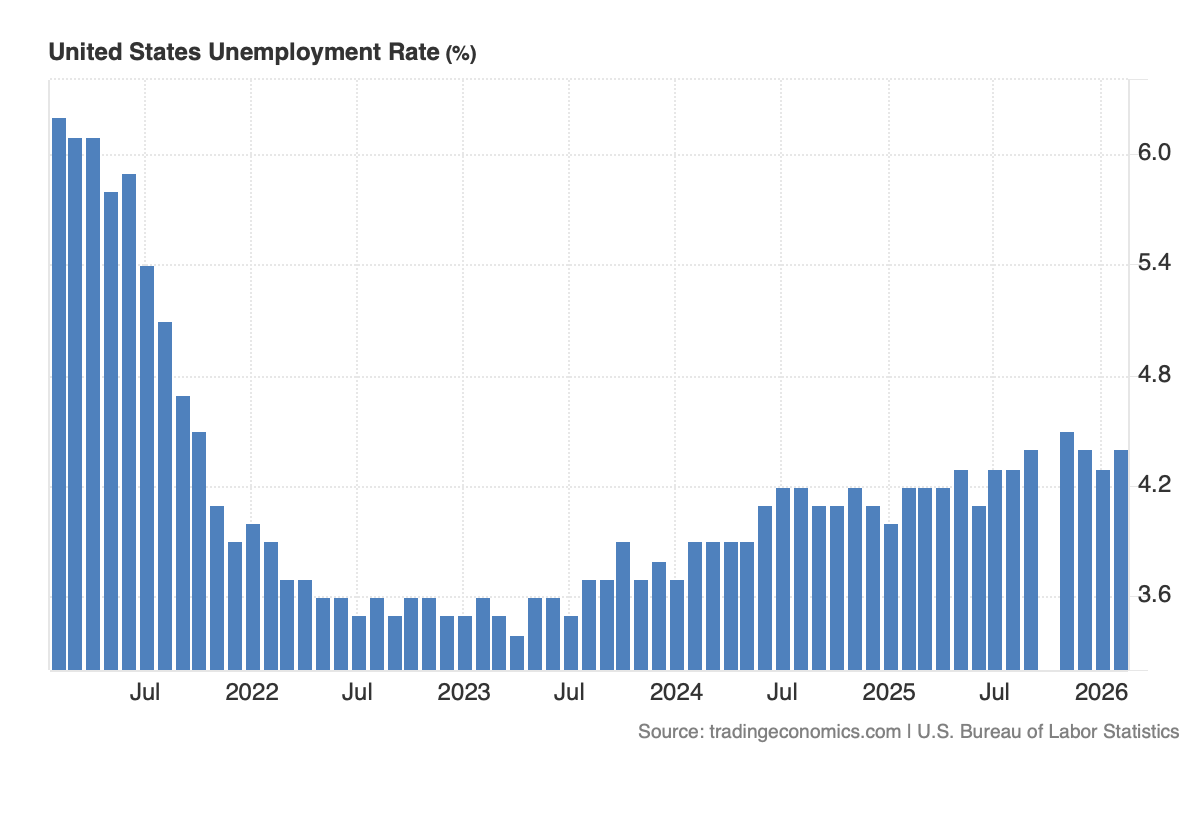

Switching to the above chart on the domestic unemployment rate, while the February reading of 4.4% wasn’t the highest level we’ve seen in some time, it wasn’t far off. Moreover, we’ve seen multiple months at that 4.4%, which also happens to be the level the Fed penciled in for 2026 in its December 2025 Set of Economic Projections. Those same projections pegged core PCE Inflation at 2.5% for 2026, down from 3.0% in 2025. Safe to say that when we get the Fed’s March 2026 Set of Economic Projections, we’re likely to see that line revised higher.

Related: Markets Face Realities of War, Both in Cost and Defense Stocks

Getting back to the unemployment rate, if we see further employment reports like the February one or the trailing three-month moving average of the data, we could see the unemployment rate tick higher.

That would put the Fed in a tight box, especially if energy prices remain elevated for longer and the potential fallout on other prices becomes another tailwind for inflation.

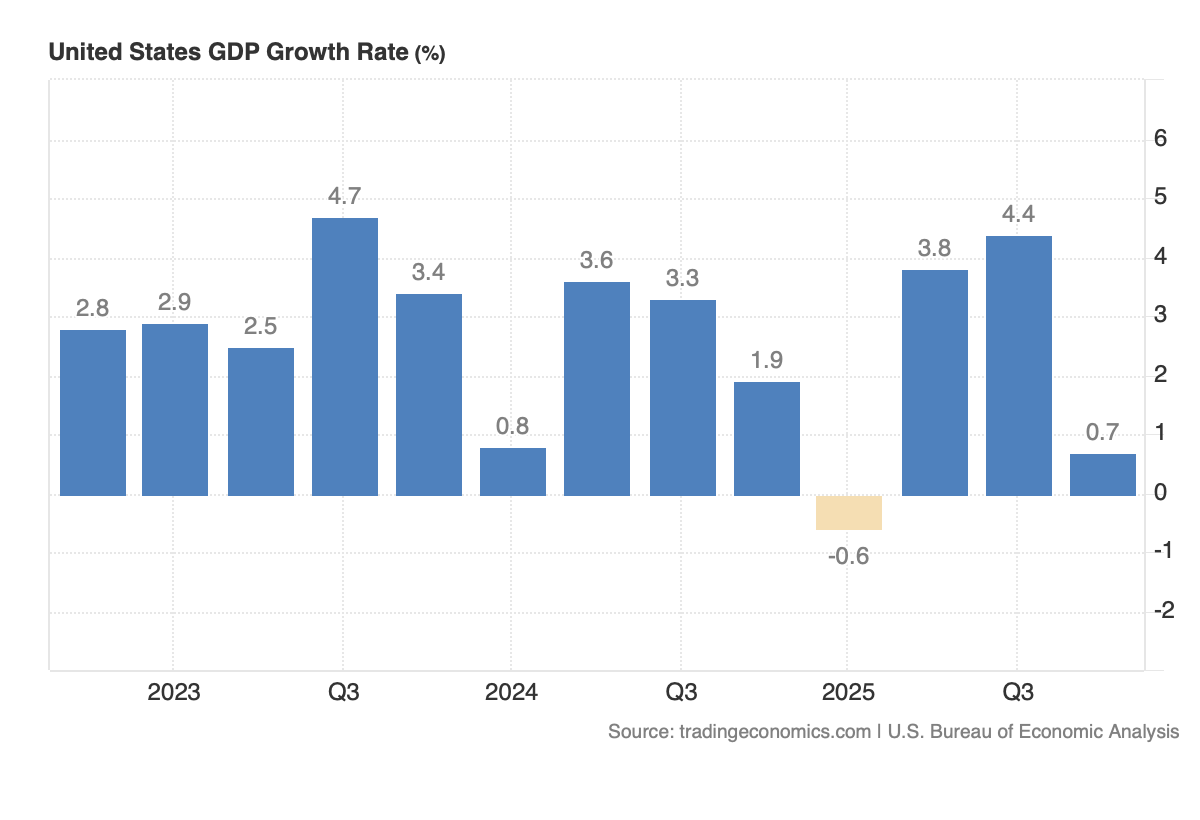

In a scenario like that, the market and the Fed will focus on that third leg of any potential stagflation stool – the pace of the economy. Today’s second look at GDP for Q4 2024 was cut in half to 0.7%, one of the weaker readings we’ve seen over the last few years. But in analyzing that figure, we need to factor in the quarter also included the longest government shutdown.

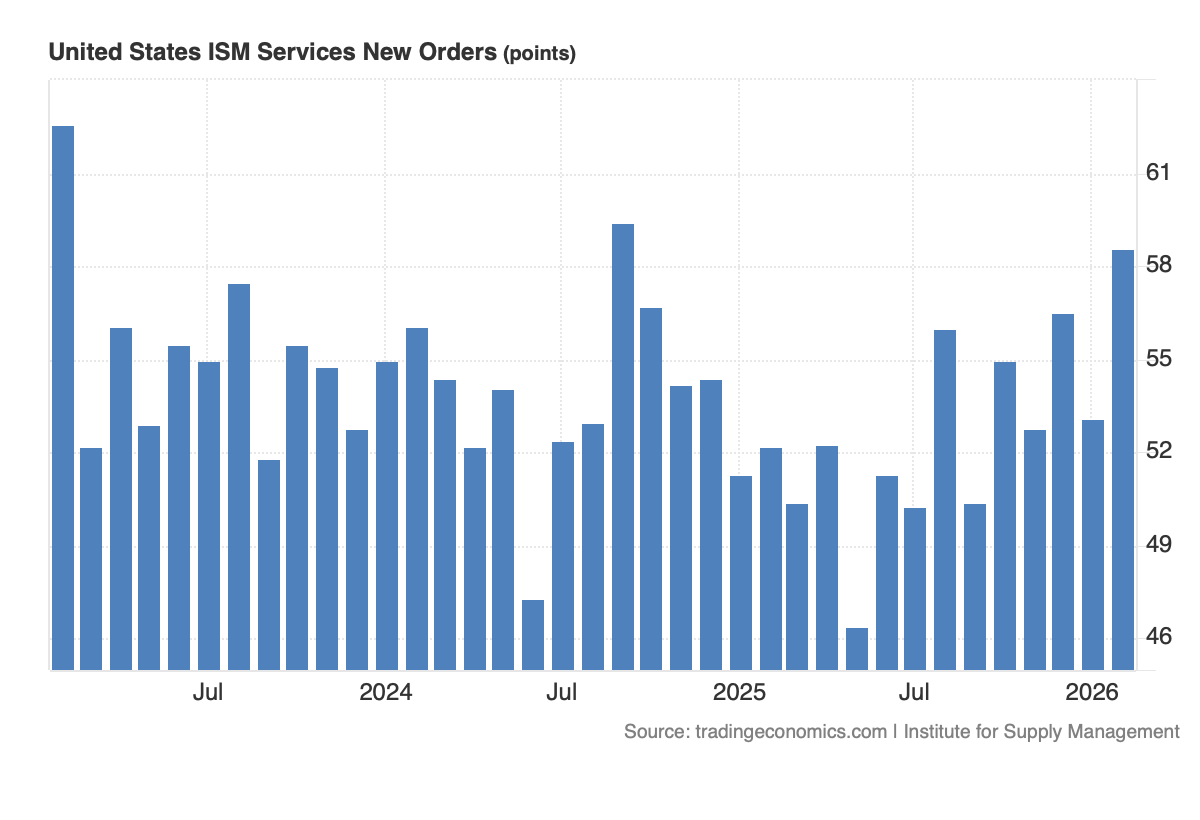

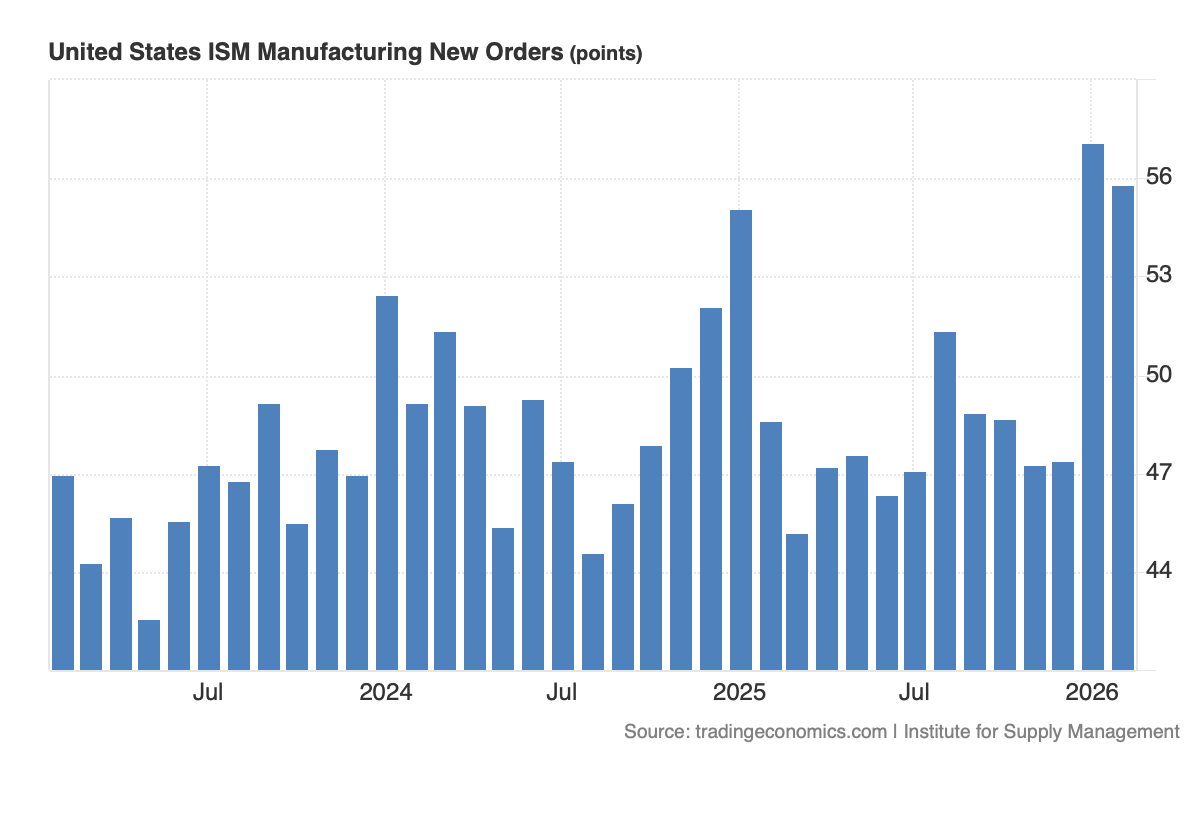

On this week’s Stocks & Markets podcast, Bob Lang shared his view that the economy in the current quarter would perk up due in part to the re-opening of the government. That makes sense, and it’s supported by the upturn we’ve seen in recent New Order data captured by ISM’s monthly Purchasing Managers' Index reports. Bob also voiced his concern over the speed of the economy as we get into the middle of 2026.

We’ll want to revisit the probability of that as we collect upcoming new order data from ISM, and it’s another reason we’ll want to tune into the S&P Global Flash March PMI report on the March 24. The question we'll be pondering is how much of that recent order strength was due to the reopening vs. true levels of demand.

As we get that data and analyze it against other reports and signals, we’ll update our thinking and adjust the Portfolio accordingly.

The Pro Portfolio had no position in any security mentioned.