Sharp Fall in Housing Starts Confirms Our View on Homebuilding Stocks

Digging into the latest data around the housing market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There’s nothing like starting your day at the auto-body shop to get a late start on things, but with that said, let’s tackle Tuesday’s May Housing Starts report and discuss some of its implications as we get ready for the culmination of the latest Fed policy meeting and the debut of Fed Chair Kevin Warsh.

Total housing starts fell 15.4% month on month in May, reaching a seasonally adjusted annual rate of 1.177 million, the lowest since May 2020, and well below the market forecast of 1.43.

And it gets a little worse… April starts were downwardly revised to 1.392 million in April. May housing starts were also down 8.7% on a year-over-year basis with single-family down 6.7% to 0.882 million and multi-family dropping more than 12% to 0.284 million.

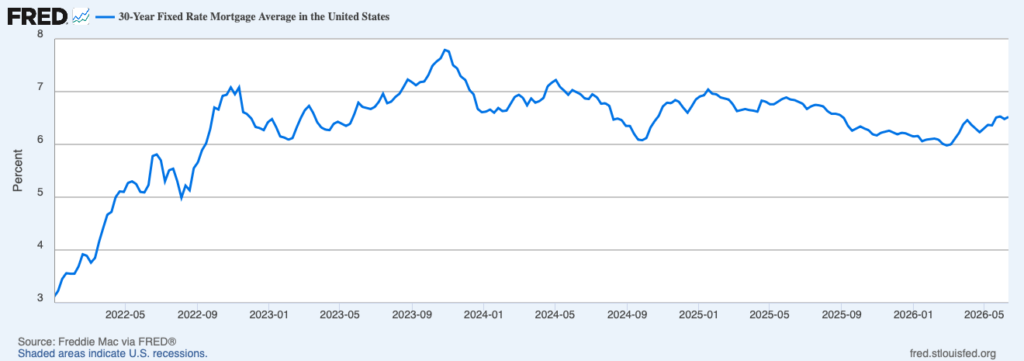

Reading through the data, we find that high mortgage rates are curbing builder activity, with contractors adopting a cautious approach as they reduce the inventory of new homes for sale due to sluggish demand. We can see this in the number of new starts mentioned above compared to the number of new housing units completed — 0.872 million for single-family and 0.426 million for multi-family— compared to the number under construction— 0.587 million for single-family and 0.662 for multifamily.

What homebuilders are aiming to do is avoid excess inventory at a time when they are already using lower prices, incentives, mortgage rate subsidies and other items that weigh on margins to attract buyers. In other words, avoid having to escalate the very things that have weighed on their margins so far this year and kept us away from being involved in that part of the stock market.

So far, that has been the right call, but at some point, the time to become involved in the housing market could arrive. Given what we’re seeing on inflation pressures and mortgage rates, that timing isn’t likely to be with us in the short term, but we’ll continue to monitor developments. Some items that fall under that include a stabilization in homebuilder backlogs and backlog pricing.

From a Q2 2026 GDP perspective, the May Housing Starts miss will being a negative factor for the current Q2 2026 GDP figure of 3.3% served up by the Atlanta Fed’s GDP Now Model. Remember, Wednesday brings the May Retail Sales report and once we have that report, we’ll have a better view on current quarter GDP ahead of the Fed’s policy decision, updated Set of Economic Projections, and policy presser on Wednesday afternoon.

We’ll be sure to check the Atlanta Fed’s GDPNow model for its next scheduled update.