Services Economy Perks Up, But Inflation Pressures Persist

Multiple looks at February job creation reduce the odds of any needed Fed intervention.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We’ve got the first part of the day’s swatch of economic data, and by and large it shows a pick-up in activity for the Services sector, job creation perking up some, and inflation pressures still elevated.

Let’s break it all down…

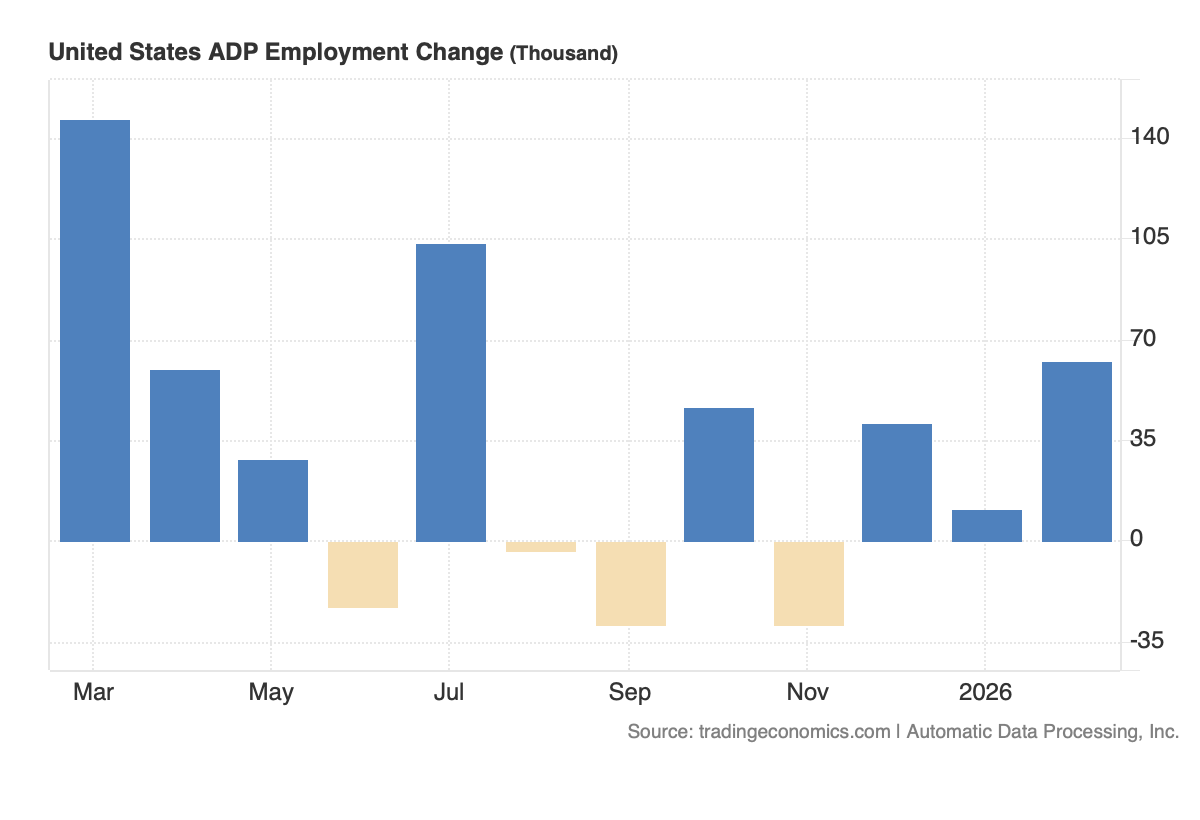

ADP February Employment Change Report

As we can see in the chart below, ADP’s findings for February job creation in the private sector accelerated, hitting the highest level in the last few quarters. The vast majority of the better-than-expected 63,000 jobs came from small businesses, but peering deeper into the figures we see Education and Health Service added the greatest number of jobs in February followed by Construction, while Professional Services and Manufacturing lost jobs.

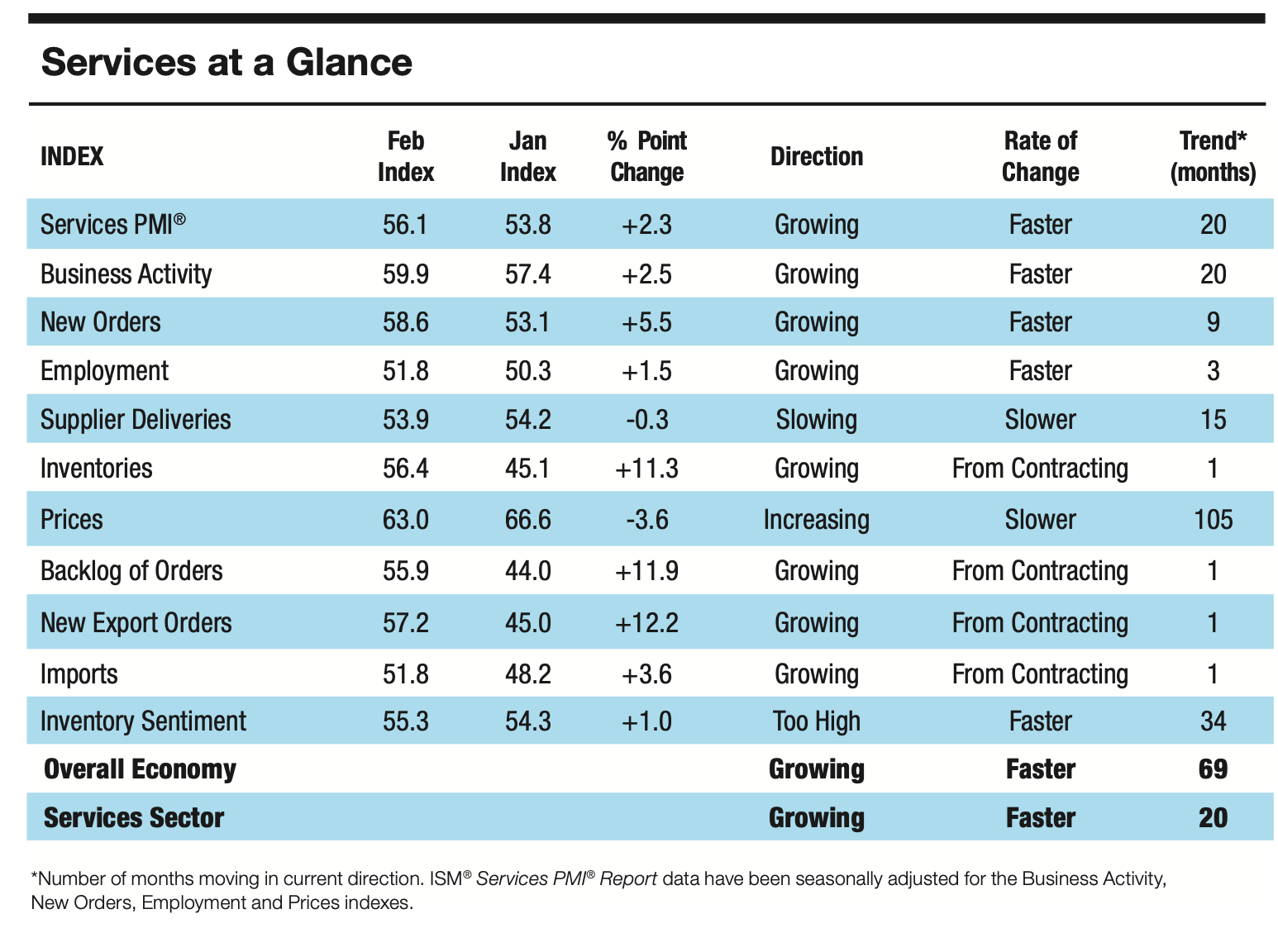

ISM February Services PMI Report

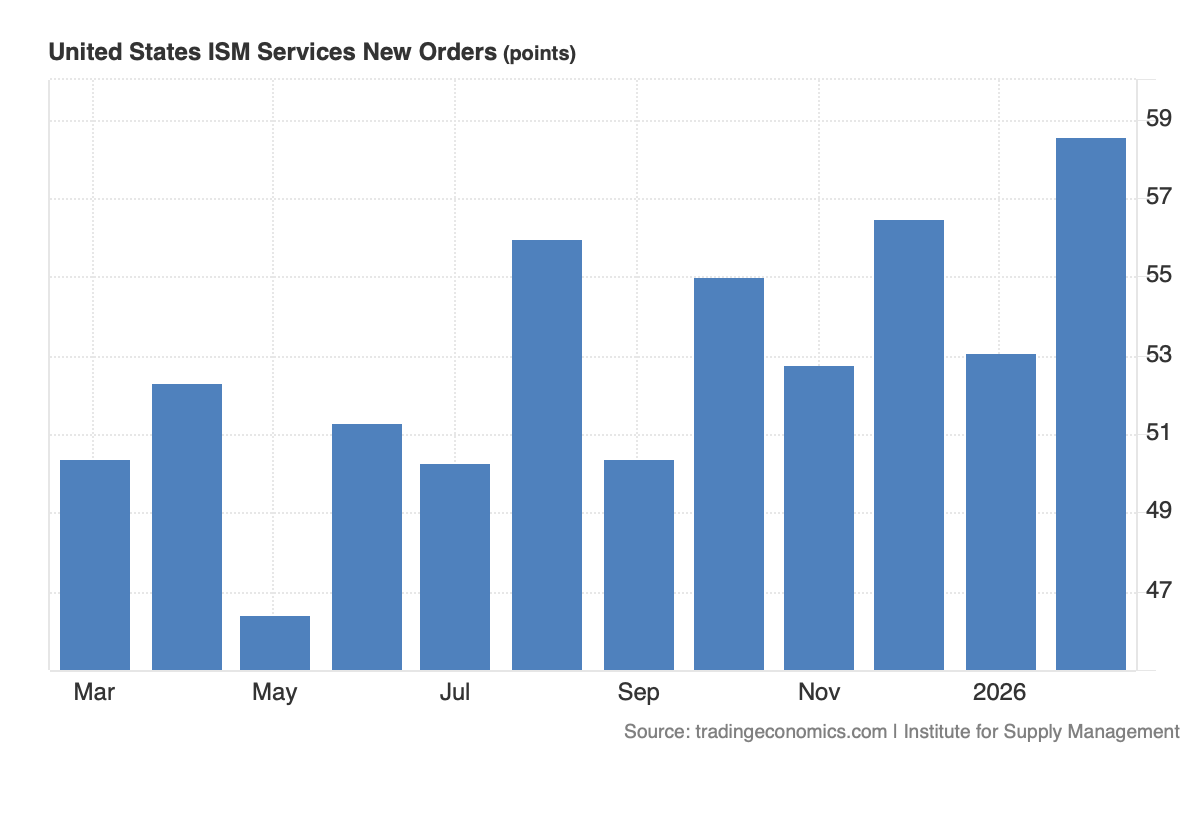

The findings from ISM’s February Services PMI data paints a more favorable picture for the part of the economy that accounts for 85%+ of GDP. Not only did activity in that part of the economy accelerate, but job creation improved compared to January. The standout, however, was new order activity hitting the highest level in over a year, which bodes well for the economy in the months ahead.

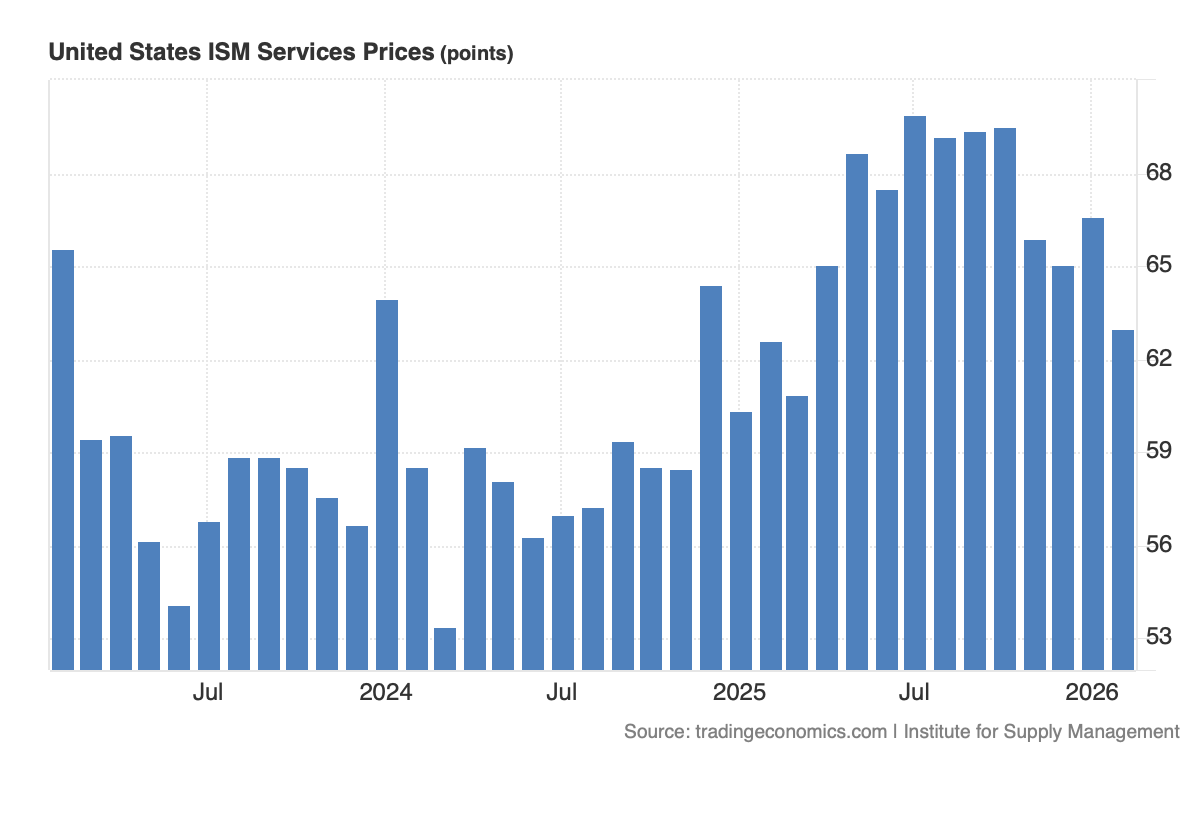

ISM’S findings show inflation pressures decelerating, but at a reading of 63.0, it indicates those pressures remain elevated. Remember, the expansion/contraction line for ISM’s data is at 50.0.

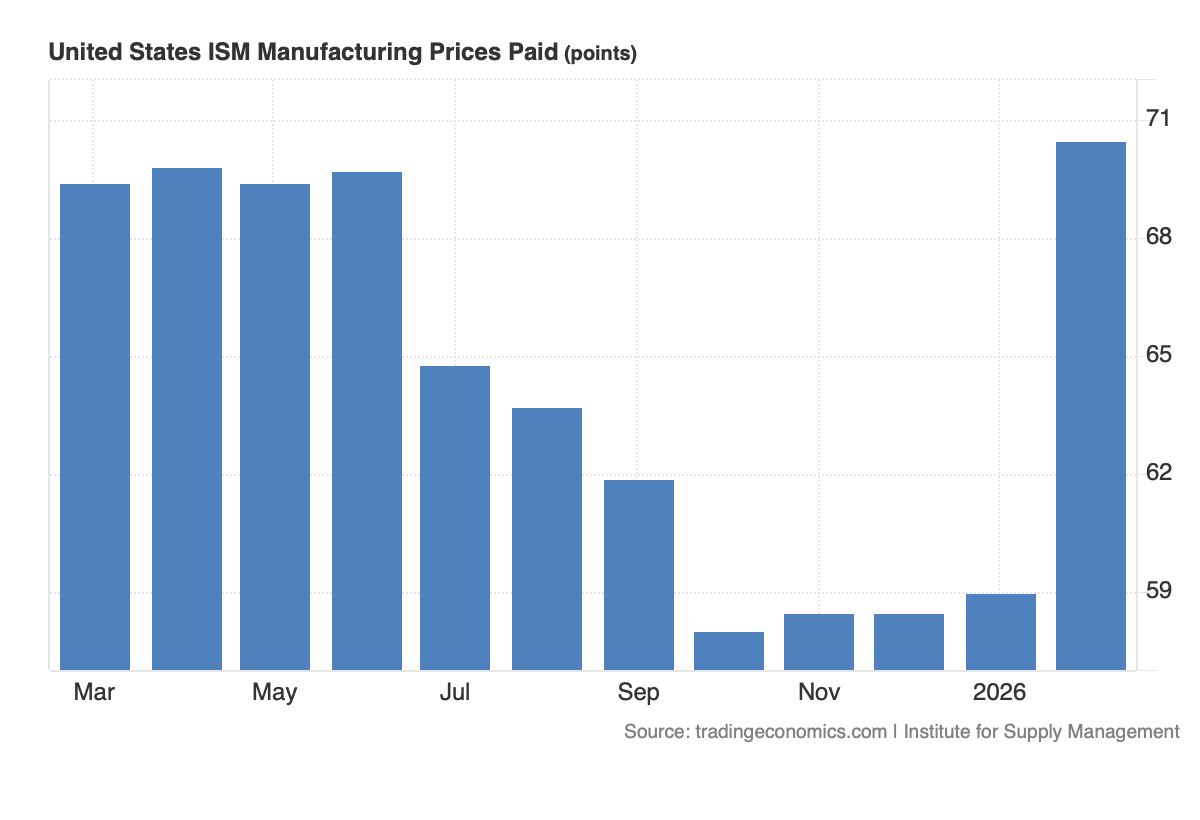

When we look at the February Manufacturing Price Index published by ISM on Monday, the sharp increase ahead of the very recent jump in oil prices is another indicator that inflation pressures persist.

Our Thoughts

Piecing the data sets together, we can surmise the economy remains on a growth vector and job creation continues at a modest pace. That implies the economy isn’t in such dire straits that the Fed would need to swoop in with defibrillator pads to revive it. At the same time, the combined picture captured by the inflation data tells us we should expect more comments like those from Cleveland Fed head Beth Hammack we shared this morning.

The next set of Fed speakers are set for Thursday and Friday, and if they say anything, odds are it will be about how the Fed will want to gauge the impact of the U.S.-Iran conflict on oil prices and how that may run through the economy. Also, as we touched on this morning, President Trump’s 15% universal tariff, up from 10%, is poised to kick in sometime this week. That’s another reason, in our view, for Fed officials to be more hawkish in their comments and combined with other developments it has the potential to keep the market restrained.

The final piece of economic data today will be the latest installment of the Fed Beige Book released at 2 PM ET today, but we’ll want to contrast our above discussion with what is revealed in Friday’s Employment Report.