Revisiting a Bullpen Public Safety Company With AI Upside

Opportunities with AI and rising spending are offset by the technical setup… for now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When we closed out the Portfolio’s position in Axon AXON, we booked a considerable win for the Portfolio and members and placed the shares into the Bullpen.

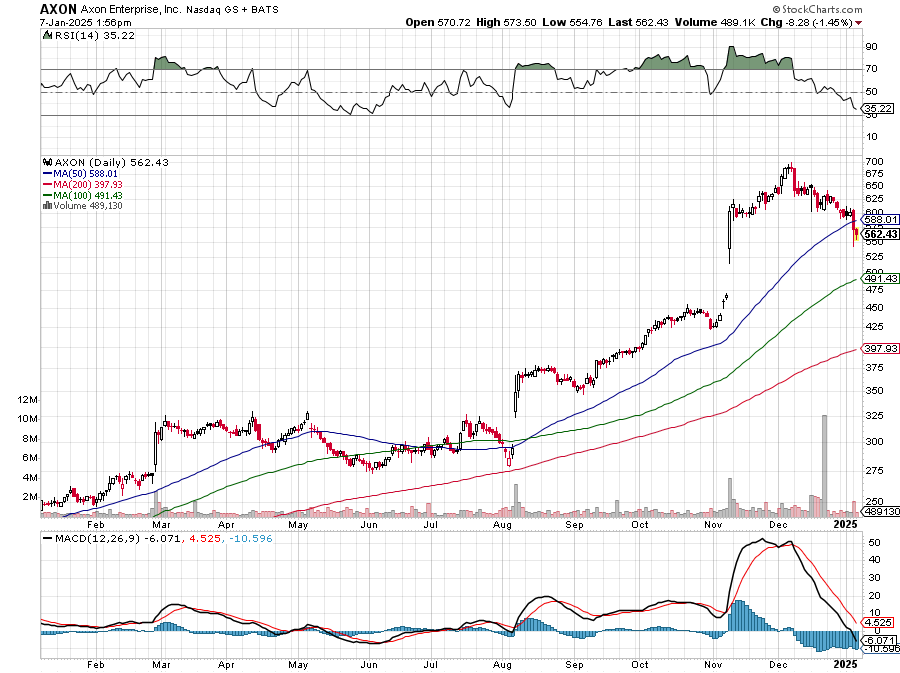

Over the last several weeks after peaking near $690, AXON shares moved steadily lower, bottoming out near $550. That move came even though consensus EPS expectations for 2024 and 2025 increased since early November, currently residing at $5.26 and $6.27, respectively. The underlying assumptions reflect continued growth in the company’s taser and body camera hardware but more importantly the accelerating adoption of the corresponding cloud solutions that turn data collected by those devices into usable and storable information.

By comparison, in early November those figures stood at $4.80 and $5.91, respectively, and those revisions mean Axon is now expected to deliver annual EPS growth of just over 23% between 2023 and 2025, up from 19.5% in early November. That’s what caught our attention as the shares have corrected

While we don’t expect Axon to make an appearance at CES 2025, we do see its business benefitting from the incorporation and adoption of AI into its offerings. We touched on this several times in H2 2024, citing it as a potential growth driver in the coming quarters. That opportunity to drive revenue, pricing and EPS growth was one of the reasons Morgan Stanley upgraded AXON shares to Outperform in early December. When it made that move, Morgan slapped a $700 price target on the shares, which equates to a price-to-earnings growth multiple of 4.84x using consensus 2025 EPS figures.

Pretty steep, but let’s remember that is a target price valuation and it’s not the highest one out there, even though the consensus price target is around $600. That honor belongs to Baird with its $800 target and its thought process doesn’t stray too far from AI, noting back in early December that Axon was seeing early success with its AI Era Plan. The initial product offering in that suite is Draft One, which leverages generative AI and body-worn camera audio to produce high-quality draft report narratives in seconds. The aim is to drive greater productivity initially for law enforcement, but we see applications in other areas, including healthcare, as having long-term potential.

Gaming this out, this likely means we will see a similar shift in public safety spending, which is expected to reach about $828 billion by 2030 from $550 billion this year, toward AI that we’ve seen in IT spending. And when we say “toward AI,” we mean both AI-enabled hardware but also AI software and services. In other words, public safety spending is likely to replicate what we’re seeing unfold in companies — the allocation of greater investment spending to AI solutions.

With ServiceNow NOW and Elastic ESTC, we’ve talked about how that spending mix shift is driving revenue, including subscription revenue, as well as margins and EPS. What Axon has in common with those tech companies is that it also offers its cloud and software solutions as a subscription business. Exiting the September 2024 quarter, Axon had an average annual recurring revenue of $885 million, roughly 45% of its trailing 12-month revenue. AI-enabled services would be another way for Axon to drive its subscription revenue higher, and Axon management has made it clear, Draft One and AI Era will utilize that business model.

All of this has us revisiting AXON shares but as you know we do our best to be disciplined investors. Granted, AXON shares are well off their highs and the fundamental outlook is rather good, but from a technical perspective, the shares are not oversold, nor are they near any real support. As you can see below, there is a rather large gap in the chart from their November jump higher.

We’ll continue to keep a close eye on AXON shares. Should they become oversold or encroach on that 100-day support level near $491, we may be inclined to call them back up to the Portfolio. At the same time, positive catalysts for public safety spending could be a catalyst for us to get involved. For now, however, AXON shares remain in the Bullpen.

More Pro Portfolio

- Increasing AI Spending in 2025 Leads Us to Buy More Shares of This Holding

- Weekly Roundup: Off to a Good Start Despite Santa Arriving Too Late

- Large Language Models Eat Up Big Electricity -- and Other Stories That Speak to Our Portfolio

At the time of publication, TheStreet Pro Portfolio was long NOW and ESTC.