Restaurant Decline Could Be Boost for These 2 Holdings

We’re also examining some dining-at-home plays for the Portfolio’s Bullpen.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Recently, Fiserv FISV published its Fiserv Small Business Index for June 2025, and while it showed year-over-year sales rose 4.4%, sequentially, sales fell 1.4% following a 1.0% month-over-month drop in May.

What stood out to us was the faster decline in spending at restaurants, which fell 2.6% in June compared to May after dropping 5.6% in May compared to April. Those declines can be traced back to falling foot traffic, which slipped 2.5% in June compared to May, after falling 5.6% in May from April. That data, along with the 0.9% sequential drop we saw for Food Services & Drinking Places in the May Retail Sales report, suggests consumers are cutting back on dining out.

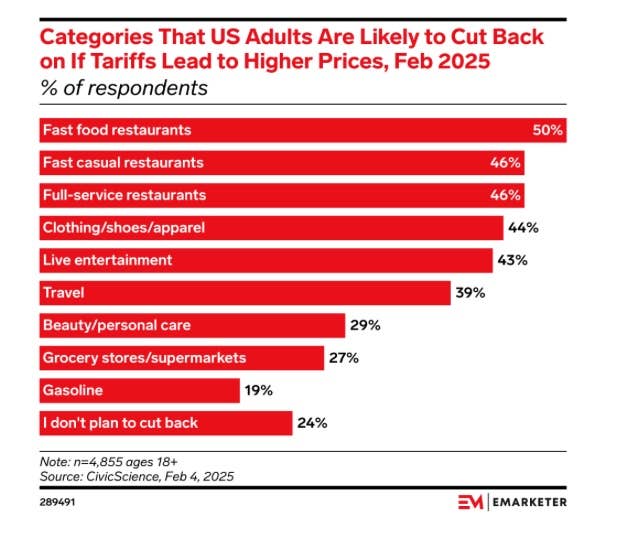

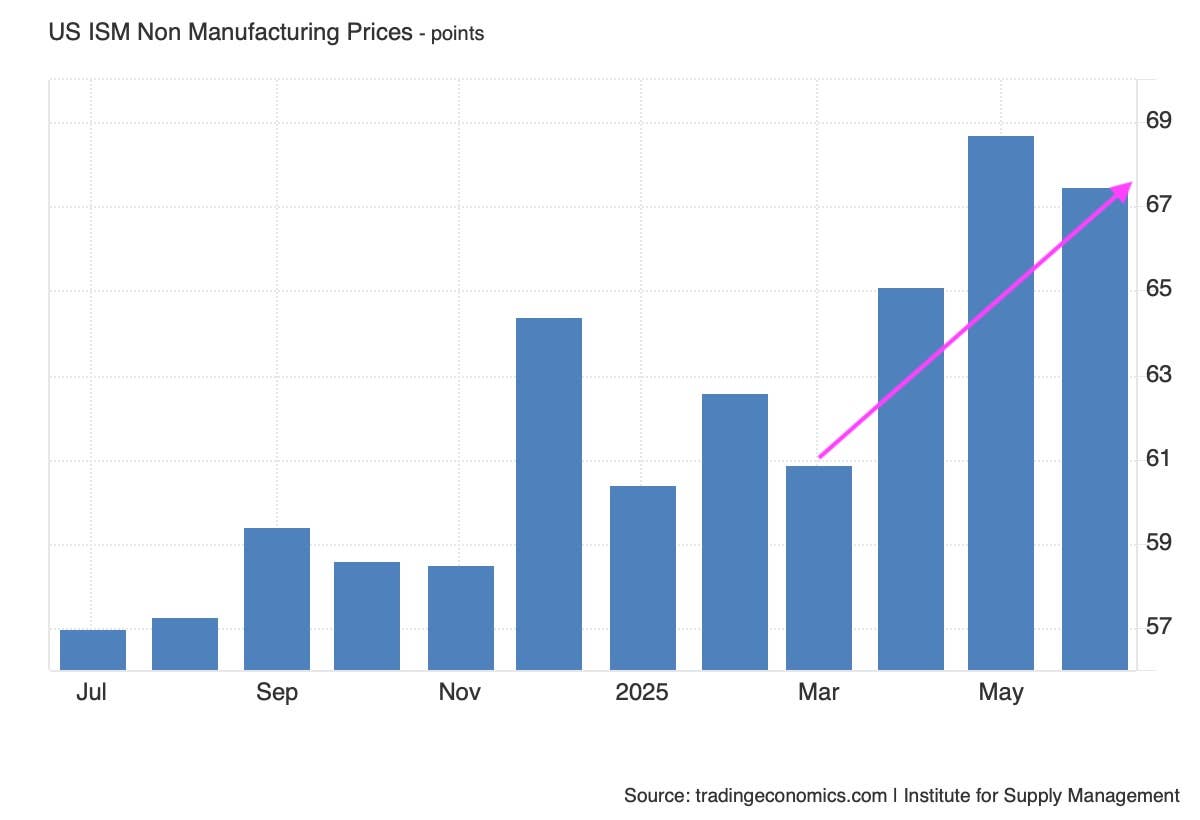

The question to ask is, after mixing the findings from eMarketer that almost 50% of U.S. adults are likely to cut back on dining out if tariffs lead to higher prices and the uptick we saw in the April, May and June Service PMI data from ISM, should we be surprised by that restaurant spending decline?

“No” is our thinking, and it’s one reason why we’ve steered clear of restaurant stocks like Darden DRI, which recently issued downside guidance for this year, or even fast-food ones like McDonald’s MCD. Last week, based on its proprietary data and industry conversations, KeyBanc reduced EPS expectations for McDonald’s, citing slower-than-expected comp sales. On Monday, Guggenheim also mentioned tepid U.S. same-store sales growth as a reason to trim its MCD price target.

While people may dial back dining out, we do know that past a certain point, they need to eat. That helps explain why Kroger KR upped its same-store sales outlook to 2.25% to 3.25% from 2.0% to 3.0%. Not a huge lift, but certainly a directional one that indicates folks are spending more at grocery stores. This will see us pay close attention to quarterly results and guidance from ConAgra CAG later this week and based on what we learn we will be doing some leg work on companies like McCormick & Co. MKC, former Portfolio Bullpen resident Tree House Foods THS and Nomad Foods NOMD.

As we examine these companies, we’ll assess their competitive positions, prospects for EPS growth, and other factors that fit with our discipline. While we could see one of them graduate to the Bullpen, there is no guarantee that will be the case.

In terms of our existing Portfolio holdings, the shift to eating at home certainly bodes well for Costco COST, a position we recently upgraded to a One rating, as well as Amazon AMZN, and its growing food business.

As it relates to the shares of Dutch Bros BROS, while folks may be dialing back larger restaurant spending, let’s remember that, generally speaking, prices at Dutch Bros are lower than those at Starbucks SBUX. There is also the continued west-to-east footprint expansion that is a core part of our BROS investment thesis, as well as the guilty pleasure aspect of grabbing your favorite coffee beverage or energy drink. And let’s not forget the expected food launch in the coming quarters that should bolster average ticket levels. We’re keeping a close eye on BROS shares given the recent pullback and will have a technical look at them later this week.

More Pro Portfolio

- We're Initiating a New Portfolio Position as Retailer Closings Surge

- June Monthly Roundup: Extending Our Lead Over the S&P 500 as First-Half Ends

- TheStreet Stocks & Markets Podcast: Can Markets Head Higher? With Helene Meisler

At the time of publication, TheStreet Pro Portfolio was long COST, AMZN and BROS.