Adding a New Bullpen Name as We Scratch the Surface of Pet Care

Pet care is a large and growing business, but there's one particular aspect that has us interested.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In recent weeks, we’ve seen the market rotate toward sectors outside of technology, and that has favored our holdings in Waste Management (WM) , Labcorp (LH) , Welltower (WELL) , Costco (COST) , and a few others, including United Rentals (URI) .

We’ve discussed with you the linkage between Labcorp’s diagnostics and testing business with Waste Management’s medical waste segment, and now we are looking at additional linkage between that medical waste business and another aspect of the testing and diagnostics business. That aspect centers on pets.

Why pets? A few reasons. First, depending on the source, between 66%-70% of U.S. households own a pet, and more than 90 million have at least one, up double-digits compared to 2024, per the American Pet Products Association.

Second, data published by Capital One reveal consumer spending on pets reached ~$157 billion at the end of 2025, up from $152 billion in 2024. The majority of that, between $70 billion-$80 billion, is tied to health and wellness-related spending.

Third, data from the Pew Research Center find that 97% of pet owners say their pets are “part of the family,” which means certain aspects of pet spending are likely less economically sensitive. You may cut back on the volume of treats, but odds are you’re not going to skimp on caring for your pet, even though veterinary costs, just like other medical bills, have risen considerably over the last several years.

That brings us to diagnostics and testing.

While multiple companies tap into pet demands and related spending, including Freshpet (FRPT) , PetIQ (PETQ) , and Chewy (CHWY) , when it comes to diagnostics and testing, the companies to focus on are Zoetis (ZTS) , Idexx (IDXX) , Elanco Animal Health (ELAN) , and Phibro Animal Health (PAHC) . Each of those latter four companies serves the pet or “companion animal” market as it’s called, but their individual exposure to it varies considerably.

Idexx has the largest exposure, with 90%+ of its revenue derived from its Companion Animal Group (CAG). That segment focuses on veterinary diagnostics, reference labs, imaging, and software used in pet care. The remaining revenue is split between livestock and water testing

Zoetis derives about two-thirds of its revenue from the companion animal market, with the balance from livestock (cattle, swine, poultry, and aquaculture. Good pet exposure, but much more to the livestock market.

Elanco’s business is split roughly 50-50 between companion animal and livestock.

Phibro is predominantly livestock-focused, with minimal companion animal exposure.

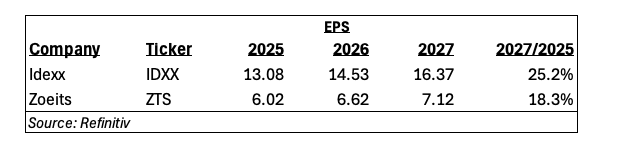

Pivoting and looking at EPS growth prospects from Idexx and Zoetis, we find consensus EPS expectations are the following:

And it becomes clear that Idexx is poised to deliver faster EPS growth.

The two questions we now have to answer are the following:

First, why, even after falling from a high near $760 in late 2025, do IDXX shares trade at a P/E multiple near 44x on expected 2026 EPS?

The answer likely has to do with the mix of business between recurring revenue vs. non-recurring, which clocks in around 85% and 15%, respectively. We’ll suss that out some more on that, but then we have to tackle our next question:

What would be a suitable entry point for the Pro Portfolio to get involved in IDXX shares?

We’ll have more on that once we get comfortable with the reasons for the premium valuation. As we work toward that, we’ll add IDXX shares to the Portfolio Bullpen and look to have some answers in relatively short order.

More Pro Portfolio:

- Buying More Palantir After Enterprise Extending Partnership

- Tracking 24 Portfolio Signals Across 9 of Our Investing Themes

- Weekly Roundup: Market Jumps on Tariff Ruling, But Braces for New Trade Moves

At the time of publication, TheStreet Pro Portfolio was long WM, LH, WELL, COST and URI.