Palantir Could Trigger New Price Target With Nine-Figure Partnership News

The expanded relationship showcases AI adoption in the commercial sector.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday, we discussed the new relationship between ServiceNow (NOW) and OpenAI, but that wasn’t the only corporate relationship that made headlines.

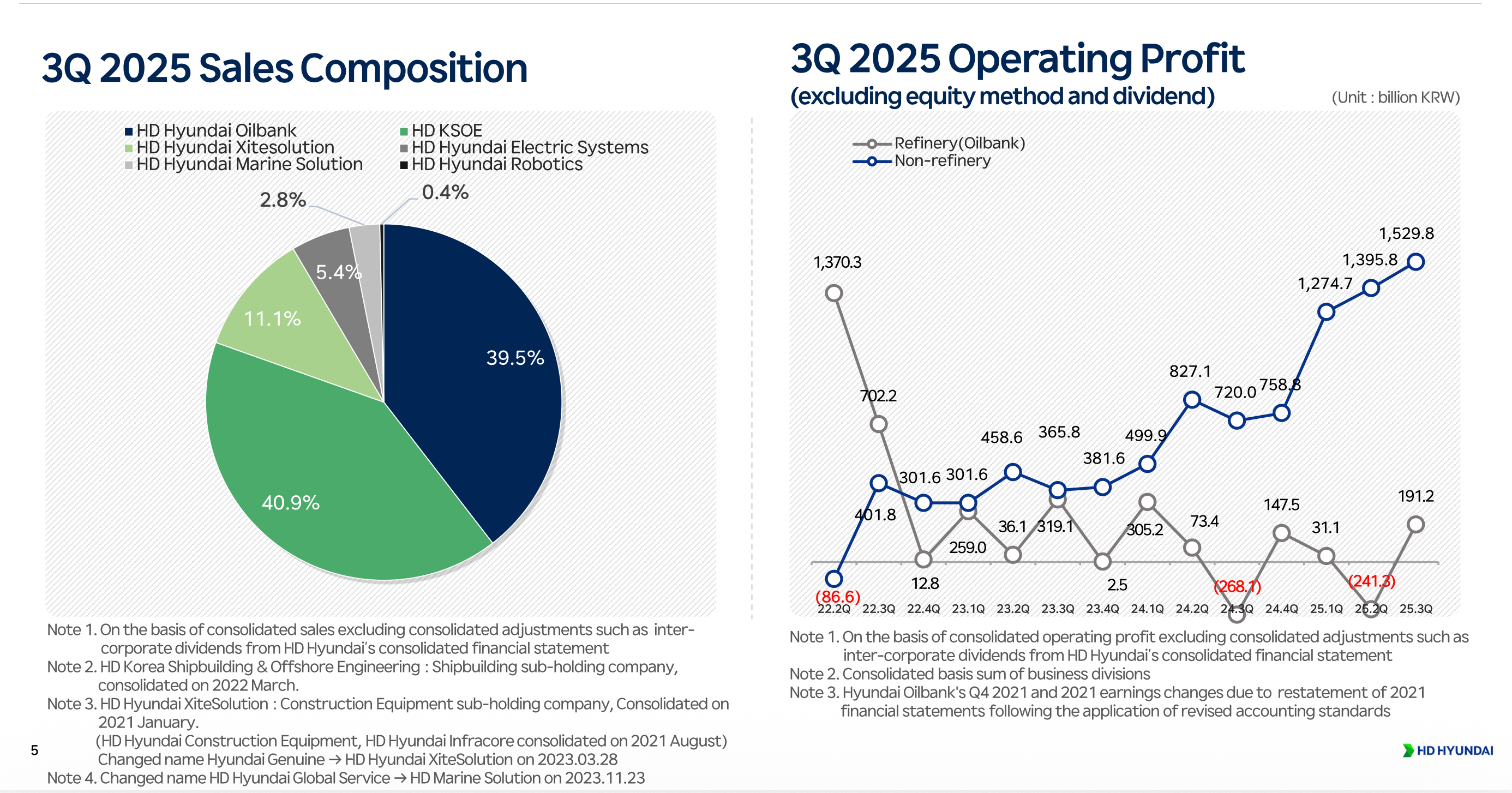

We’re talking about the expanded one between Palantir (PLTR) and HD Hyundai that moves beyond HD’s refinery operations as well as shipbuilding and construction equipment subsidiaries to “the full spectrum of HD Hyundai’s business, including electric systems, robotics, and marine aftermarket service, bringing the advanced AI tech and capabilities to the entire HD Hyundai ecosystem.”

While details were slim, Reuters made the following comment on Tuesday:

"The agreement is worth hundreds of millions of dollars to Palantir over several years, a person familiar with the matter told Reuters on Tuesday."

The other comment that stood out to us from HD Hyundai was that it is "now manufacturing ships around 30% faster using Palantir software to speed up operations…"

Let’s get some context on this expanded relationship.

In 2021, Palantir signed a deal for $20 million over five years with HD Hyundai, and that one was built on the $25 million one with HD’s refinery affiliate, Hyundai Oilbank, and construction machinery maker Hyundai Doosan Infracore.

Knowing the figures associated with those past announcements and that they accounted for up to 53.4% of HD’s revenue stream suggests there is significant incremental revenue for Palantir under this expanded relationship. What we don’t know is the duration of this expanded relationship, whether it includes the extension of the past ones, and if the “hundreds of millions of dollars” was in U.S. currency or not. If the answers are “multiple years" and “yes” to those first two items, respectively, then the agreement may be worth hundreds of millions of dollars.

If the answer to the third is “U.S. dollars,” then that is a meaningful win for Palantir on a few fronts, and it would mean we will likely need to address our current $220 target.

It expands its business not only outside of the U.S., but it also does the same for its commercial exposure. In Q3 2025, Palantir’s U.S. revenue accounted for 75% of its total revenue, while commercial revenue represented 46% of total revenue. If Palantir does not offer more details on this expanded HD relationship when it reports its quarterly results on February 2, something we see as rather unlikely, we may be able to guesstimate its size by comparing remaining performance obligation (RPO) figures. Exiting September, Palantir’s total RPO stood at $2.6 billion, of which $1.14 billion was classified as short-term RPO and the remaining $1.46 billion as long-term RPO.

We continue to see Palantir benefitting from expanding AI adoption and usage, which is behind the company’s expected EPS growing to $1.38 in 2027 from $0.72 in 2025. And yes, the win discussed above suggests there could be more upside for what’s expected this year and next.

Following the recent pullback in PLTR shares from around $195 in mid-December to Tuesday night’s close at $168.53, we reiterate our One rating. Should we see the shares retreat further, subject to market conditions, and land near the 200-day moving average, that would be a compelling place for us to add to what is already a sizable position size in the Portfolio.

More Pro Portfolio

- We're Moving Off the Sidelines and Buying More of This Holding

- Robo (Translation) Cops; Rich Pay Later, Too; More Investing News

- Weekly Roundup: Markets Take a Breath Ahead of Earnings Bump and Trump at Davos

At the time of publication, TheStreet Pro Portfolio was long NOW and PLTR.