Our Updated Game Plan With the August CPI Report in Hand

The uptrend in CPI data increases the potential for a 'buy-the-rumor, sell-the-news' Fed meeting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you were to look at the social media platform X, you are likely to see a wave of folks saying a 50-basis-point rate cut by the Fed is a sure thing following Thursday morning’s August CPI report and the latest jobless claims figures. However, while the expectation that the Fed will deliver a rate cut next week is high, and ticking even higher Thursday morning, I’m not so certain about a 50-basis-point rate cut next week. I also have questions about the market’s expectation for four consecutive 25-basis point cuts at its next four meetings (September, October, December, and January).

My skepticism about the number of steps the Fed could take in the coming months stems from the trailing three-month data contained in the August CPI print. Before we get to that analysis, first we have to acknowledge that headline CPI for August rose to 2.9% year over year and as expected compared to 2.7% in July. Core CPI also matched the market expectation of 3.1% on that basis, unchanged from July but up from 2.8%-2.9% in May and June. Examining the data on a sequential basis, while the core inflation rate held steady at 0.3%, headline inflation was warmer than expected, coming in at 0.4% up from 0.2% in July and ahead of the market’s 0.3% forecast.

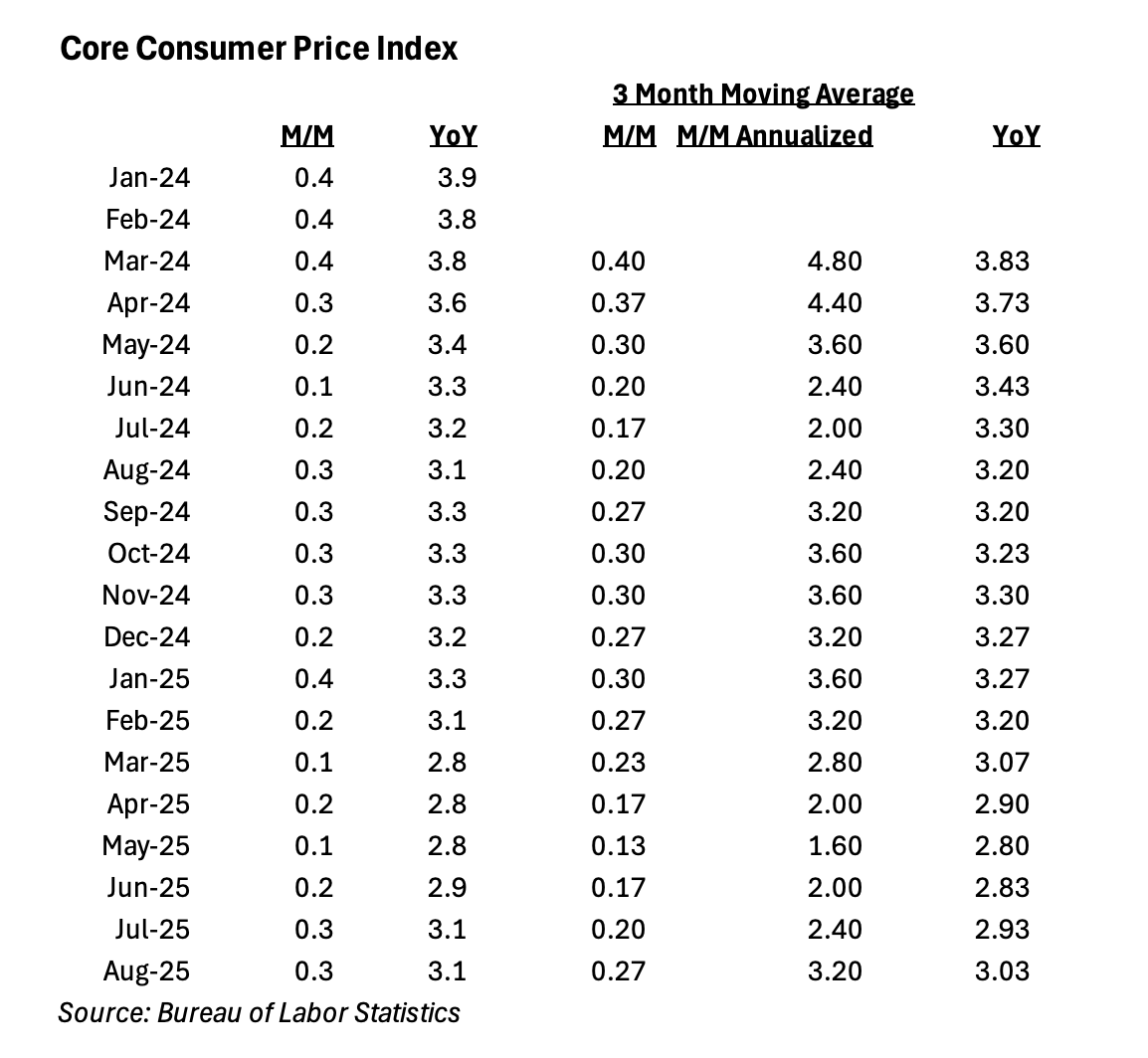

While those are the reported figures, as we’ve discussed many times, the Fed examines the figures on a trailing three-month basis as that tends to smooth out month-to-month volatility. When we look at that for core CPI, this is what we see:

Looking at the three columns to the right that present the monthly data a few different ways through a three-month moving average lens, it’s hard to ignore the uptrend that began in June for all three. The Fed isn’t likely to miss that.

Now let’s remember those retailer comments about pending price increases as they re-stock inventories and contend with tariffs.

But the employment market has softened, right?

No question that’s the case as evidenced by the August Employment Report and the revisions it contained for June and July, and the revised jobs data for the 12 months ended March 2025.

That gives the Fed room to deliver a 25-basis-point rate cut next week, but when it comes to the drop seen in the August PPI data, when has the Fed acted on a single data point? Powell is likely to acknowledge the drop and say that while favorable, the data can be volatile month to month, and therefore the Fed will want to see more “good data” to determine its next steps.

The softening in the labor market will also give the Fed cover fire to maintain the two 25-basis point rate cuts seen in its June 2025 set of economic projections. What we’ll be looking to see in those updated figures is how many rate cuts the Fed is penciling in for 2026.

Back in June, it was looking for just one 25-basis point rate cut. There is reason to think the Fed could lift that figure by a cut, maybe even two, but per the CME FedWatch Tool, the market sees the Fed funds rate between 2.75%-3.00% exiting 2026. That’s a total of six 25-basis point rate cuts, and that's a tall order the Fed isn’t likely to get behind based on the totality of the data we’ve seen so far.

Make no mistake, would we welcome cuts closer to that than not? As investors, sure we would. Let’s remember, however, the Fed doesn’t take its cues from the stock market or what investors want. At least not as long as it remains independent.

But as we discussed during this week’s podcast, next week’s Fed meeting very well could be a “buy the rumor, sell the news” event for the market.

Planning It Out

Contemplating the above and recognizing the market has been grinding to new highs the last few sessions, the odds of the Fed delivering a message the market may not like are rising. While the market isn’t overbought based on the RSI levels for the S&P 500 or the Nasdaq Composite, it’s a 2.5%-3.3% fall to their respective 50-day moving averages. Not enough to warrant taking out a short-term rental in an inverse ETF position like the ProShares Short S&P 500 SH, especially with the Fear & Greed Index only at “Neutral.”

Should we see the RSI levels for the S&P 500 move above 70 (overbought) and the Fear & Greed Index surge to “Extreme Greed” ahead of the Fed’s policy meeting next week, we may reconsider that thought.

We may also consider taking a few more chips of stocks that have had considerable runs lately and are deep into overbought territory, especially if the market grinds higher in the coming days. One such candidate for that consideration is Alphabet GOOGL, with a more than 84 RSI reading. To be clear, any such action, should it come to fruition, would be taking some, not all, chips off the table, especially with regards to Google.

At the same time, if the market does pull back following the Fed’s policy meeting, we’d be interested in picking up more shares of some of our holdings, subject to where they wind up.

TJX Companies TJX is one name we would be ripe for, but closer to $130.

Waste Management WM is one we’ve said we’re watching very closely, and that remains the case. We like what we are seeing in the stock’s MACD indicator.

With the east-to-west expansion story still intact, Dutch Bros BROS shares are flirting with support at the 50-day and 200-day moving average. Let’s see if that holds — if not, should the shares fill the gap in the chart near $57.50, that would be a compelling pick-up point.

Having recently visited the homebuilding group, we’re toiling away on something new-ish for the Pro Portfolio, while also keeping an eye on what we’ve got as investor conference season continues. As you saw Thursday morning, we’ll continue to connect the dots from those presentations and other signals.

At the time of publication, TheStreet Pro Portfolio was long GOOGL, TJX, WM and BROS.