Our Take as Services Sector Inflation Pressures Jump Big in March

Let's break down the implications of the March Services PMI report for economy, the Fed, the market and the Portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Inflation

Inflation

This morning we received the March Services PMI report from ISM, and if there were any lingering questions about the potential for renewed inflation pressures, ISM’s data cleared that up in a big way.

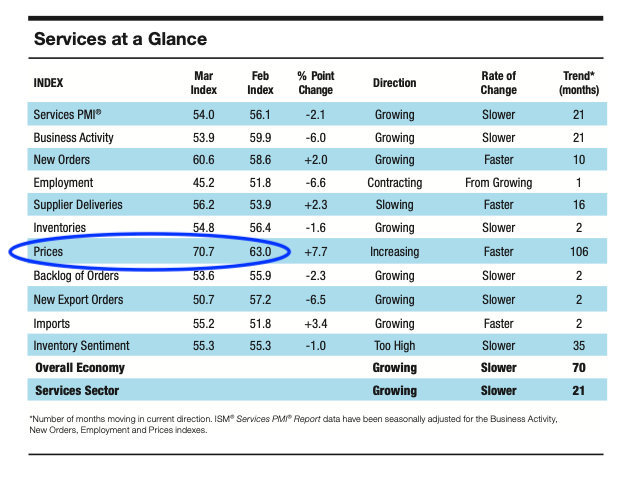

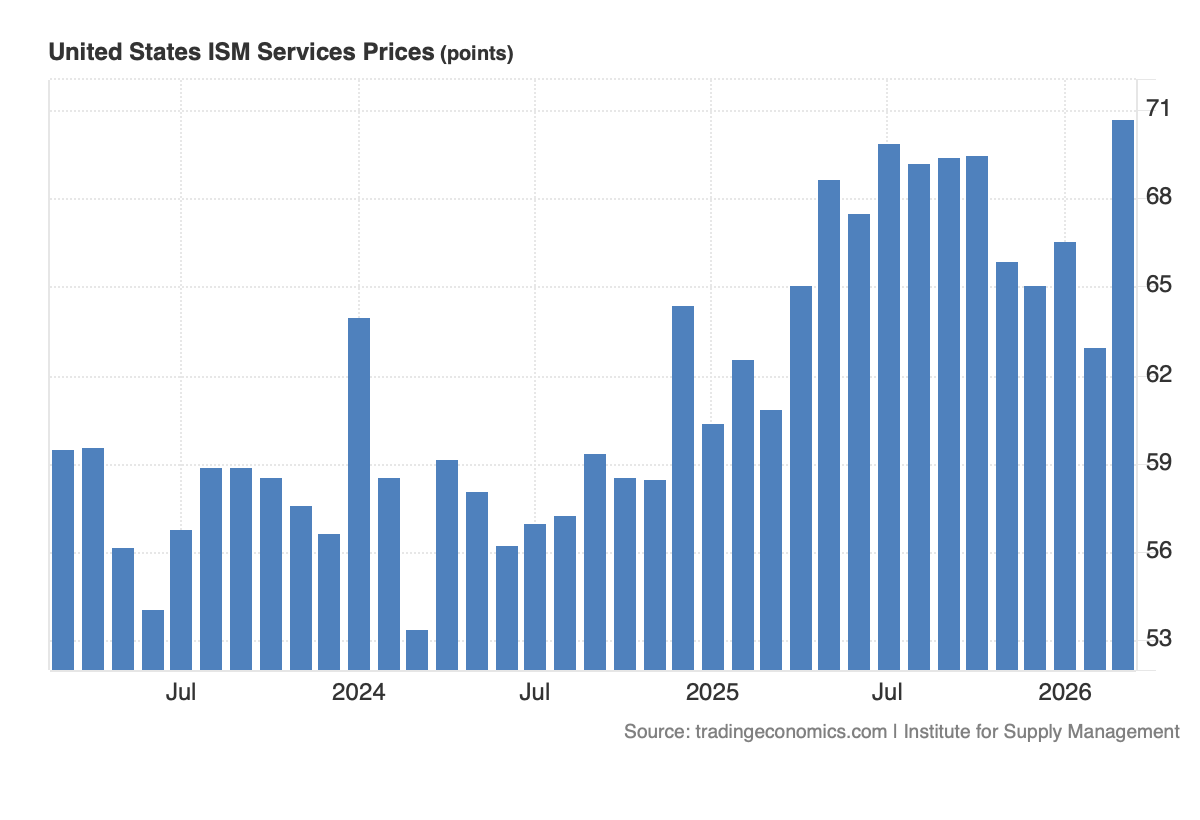

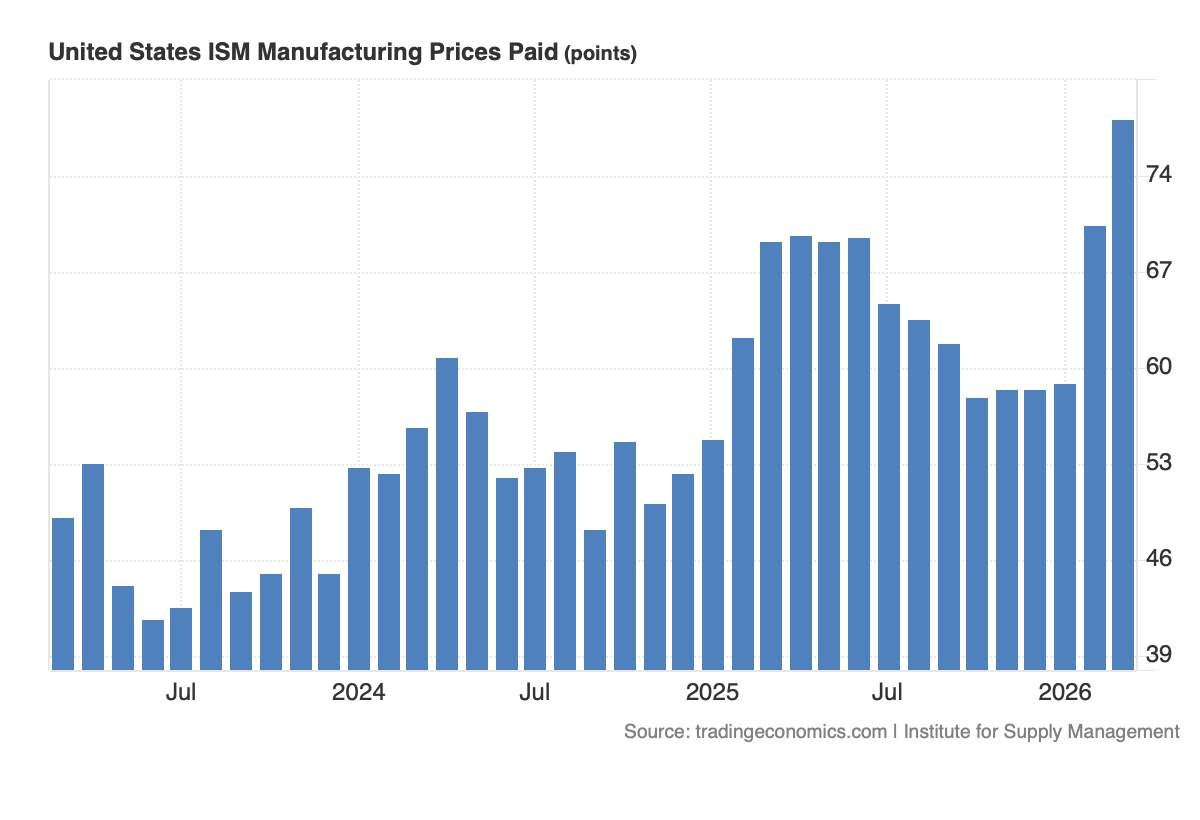

As we can see in the table below, the Prices sub-index hit 70.7 in March, the highest reading since October 2022. Let’s also remember the Pricing sub-index for ISM’s March Manufacturing PMI also came in super-hot at 78.3, the highest since June 2022.

These data points, along with the better-than-expected March Employment Report, are going to keep the Fed on the sidelines for some time, especially as questions about the duration of the U.S.-Iran conflict and its lingering follow-through effects remain. The pieces of pricing data also set the table for the upcoming March CPI and PPI reports, which would be shocking if they don’t show a sequential step up. Between now and Friday’s March CPI report, we’ll revisit the Cleveland Fed’s Inflation Nowcasting model as it updates its expectations to account for today’s March Services PMI data.

Looking past ISM’s Prices line item, the Services sector headline figure slowed in March but was still growing overall. New Order activity picked up, but similar to the question we raised about Hon Hai’s strong March revenue, there is the potential for some demand being pulled forward as the war escalated in March.

There was also a sharp drop in the Employment sub-index to 45.2, and while that figure can bounce around month to month, it was the lowest we’ve seen since late 2023. In the March quarter, we learned of corporate headcount reductions, and that could be the culprit behind the sharp drop we see in the March figure. It also raises questions about the number of jobs that were created per the March Employment Report. We know revisions to those numbers are commonplace, but this has us wondering about the size of the March revision in the April Employment Report.

Putting it all together, the March pricing data from ISM will have us listening even more intently in the coming weeks for company comments about input prices, surcharges, and fresh price increases. Those same March price figures also add to our thinking that margin pressures could have the market overly optimistic about second-half 2026 EPS expectations for the S&P 500. We’ll keep our market-hedging positions in place for now, while also reiterating our bullish stance on shares of Costco (COST) , TJX (TJX) and Amazon (AMZN) .

We’ll also be looking to see if Citigroup (C) makes another revision to its Fed rate cut call for this year. Today’s data is hard to ignore.

Related: This Optics Stock Is a Play on Both Military and Space Applications

More Pro Portfolio:

- Making 3 New Buys and Trimming 2 Holdings as We Layer in Protection

- We're Tracking 21 Portfolio Signals Across 9 of Our Investing Themes

- March Monthly Roundup: Portfolio Makes Up Lost Ground in Tough Month

At the time of publication, TheStreet Pro Portfolio was long COST, TJX and AMZN.