Our Game Plan for Today's Market Selloff

Here are our thoughts on the market's reaction to three 'surprising' developments — and how we plan to deal with it all.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are seeing stocks sell off hard Friday morning in response to three arguably surprising developments. We’re talking about President Trump’s latest move on tariffs and the uncertainty they are rekindling, but also the weaker-than-expected July Employment Report and the sharp downward revisions seen to job creation figures in May and June. Those revisions point to just 33,000 jobs created during those two months, far less than the 272,000 previously cited.

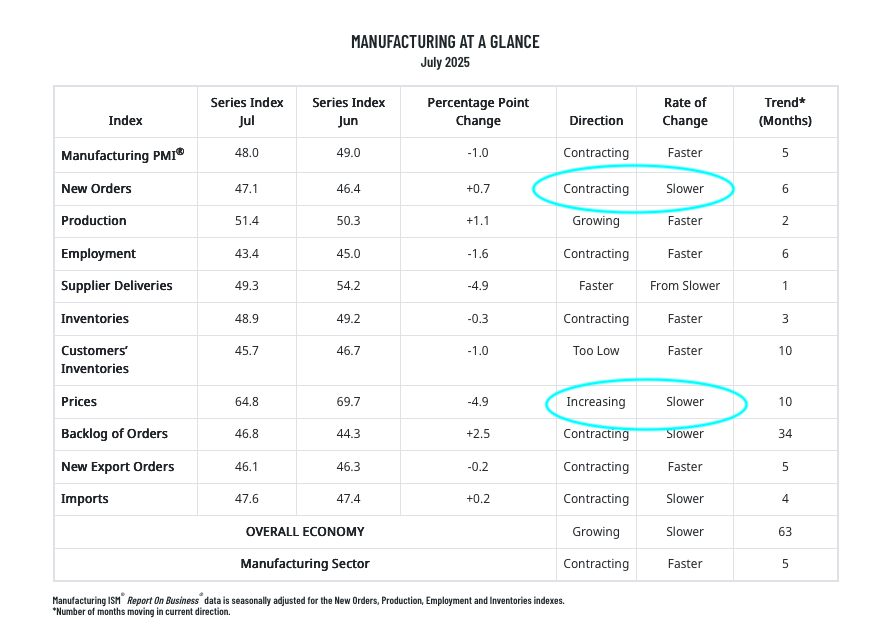

The third item is ISM’s July Manufacturing PMI report, which came in weaker-than-expected with a headline reading of 48.0, down from 49.0 in June and below the market forecast for an improvement to 49.5. The innards of that report showed modest progress in new order activity and the inflation front.

That trifecta of developments has triggered a shoot first, ask questions environment. When we encounter times like these, we are going to take a deep breath or several, and follow the data so as not to be swayed by emotions and make mistakes we may later regret. For example, we are seeing chip stocks sell off despite the findings of last week and this week about higher AI and data center capital spending levels. Data center construction activity is poised to continue, cyberattacks will still happen, and AI adoption is accelerating. Over time, we expect calmer heads will prevail, and we aim to be in that camp.

At the same time, this morning’s data is fostering yet another rethink on when the Fed may deliver its next rate cut. Following Fed Chair Powell’s sobering comments on Wednesday afternoon, the market’s expectation for a September rate cut tumbled, but following today’s data, the market now sees an 83% chance for such an event.

Next week brings another look at the Services economy, which, as we know, accounts for a far larger percentage of the overall domestic economy and GDP. If we see that the July PMI report from ISM falls short of expectations, it may fall into the camp of bad news for the economy is good news for rate cuts.

As we get that clarity, we have our pickup points for the pro Portfolio, and we’ll be opportunistic where it makes sense based on the data, our position sizes, and respective RSI levels.