October Job Creation Improves, But Inflation Pressures Remain

With more earnings ahead, the data doubles down our focus on operating margins.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Following our Axon (AXON) and Arista Networks (ANET) trades and analysis of SuRo Capital’s (SSSS) complete September-quarter results, we are turning to today’s economic data. The volume of data is far smaller because of the government shutdown, but we still need to understand the economic backdrop, especially when it comes to job creation and inflation. Plain and simple, the Fed is watching it, and therefore, we must be too.

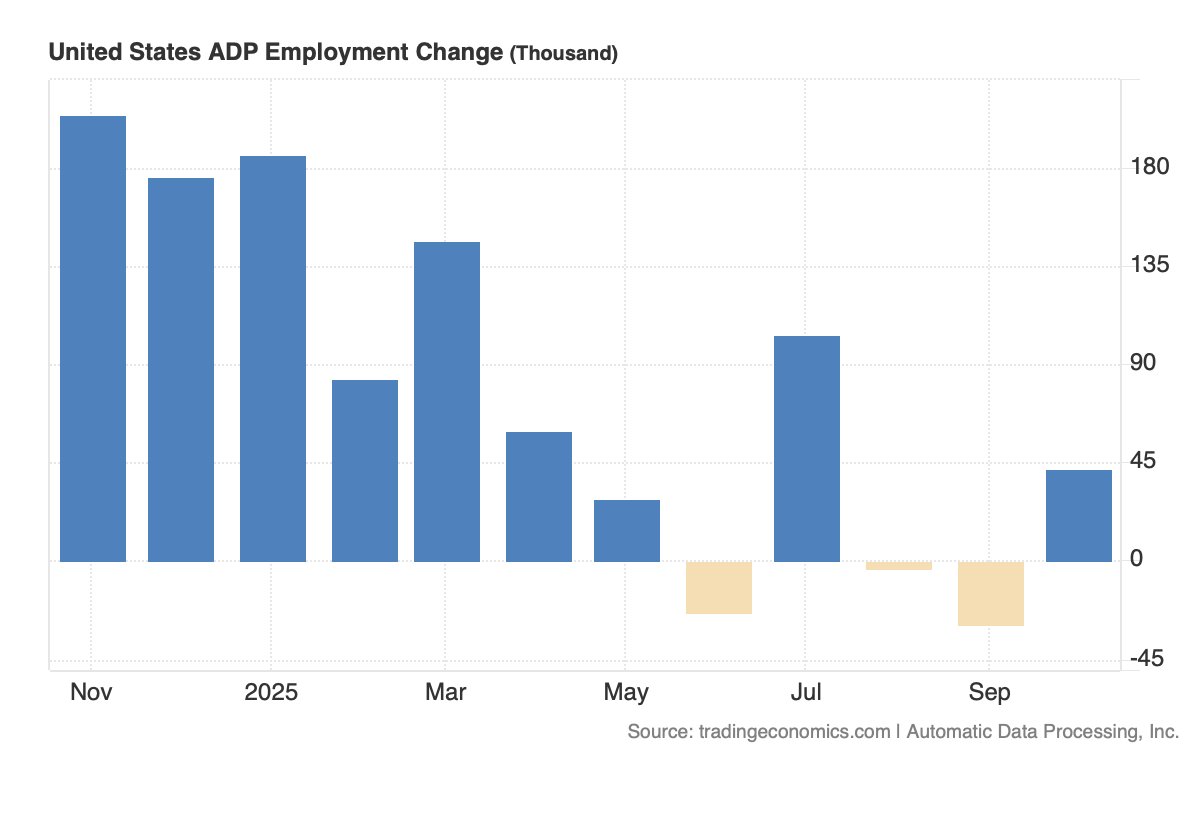

What can we surmise from today’s October Employment Report from ADP and ISM’s October Service PMI data? Job creation improved to its best level in the last three months, but it was still modest compared to earlier this year. Wage pressure didn’t accelerate, per ADP’s findings, compared to September, but with year-over-year path growth for job stayers remaining at 4.5% in October and at 6.7% for job changers, employers are still paying up for the jobs they are filling.

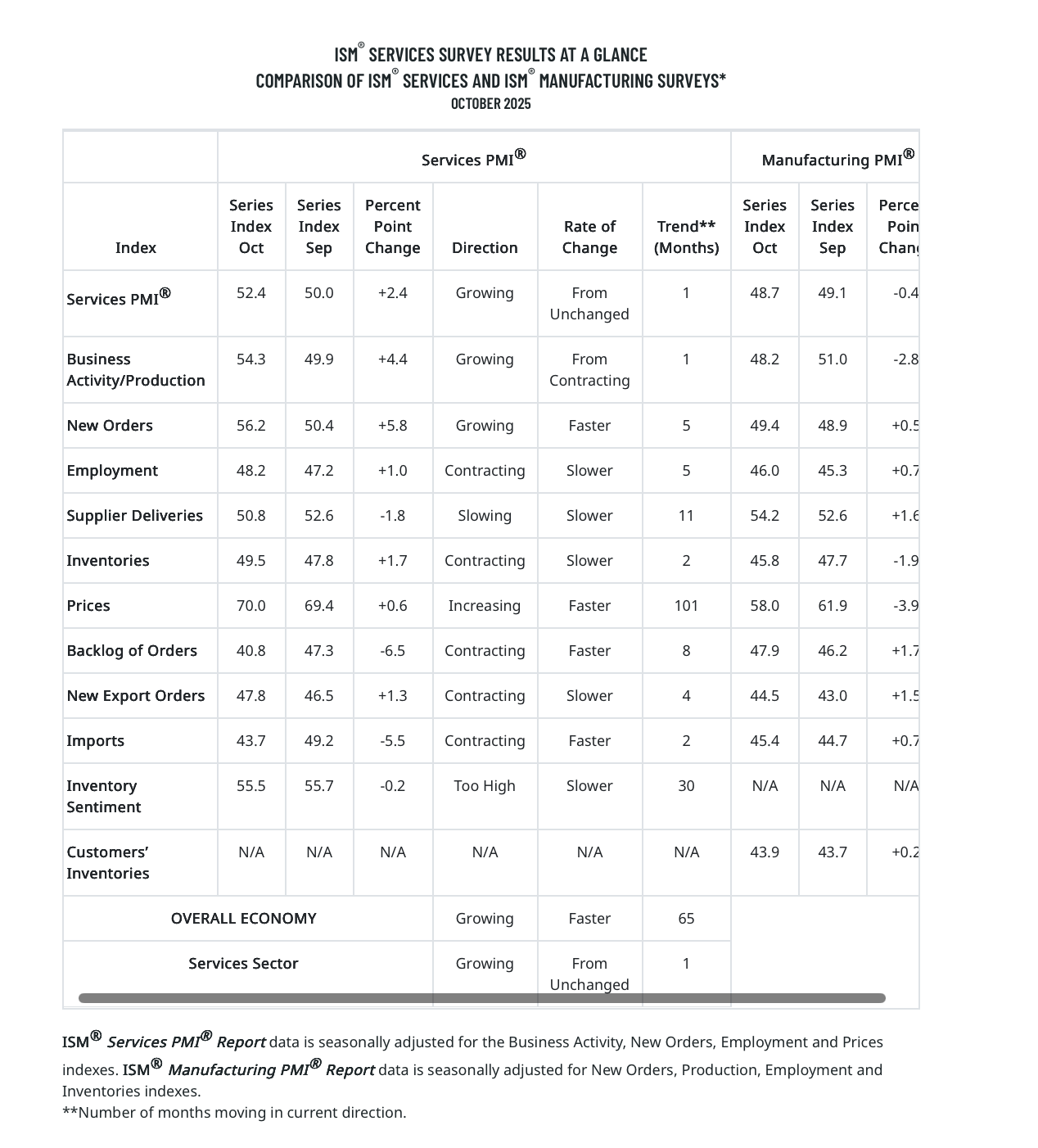

While ISM’s October Service data showed a nice pickup in production and new order activity, which tells us the current quarter started at a brisk pace, it also reveals inflation pressures ticked to the highest level in three years. Now that the increase reflects input costs, and while S&P Global’s Final Service PMI for October found that as well, S&P also found “that competitive pressures had limited the degree to which higher costs could be passed onto clients.” This doubles down our focus on operating margins as we move into the second half of the current earnings season.

When it comes to the Fed, the uptick in the uptick in Services sector activity and modest improvement in job creation are signals the economy isn’t in dire straits. Meanwhile, the uptick in inflation pressures is something that it will not miss.

Let’s keep in mind that we have more data to come this week, as well as November data to come before the Fed concludes its next policy meeting on December 10. When that picture is complete, we’ll have a much clearer picture as to whether the Fed will… or will not… deliver the rate cut the market expects.