New Microsoft Price Target After Surge in Cloud Revenue

We are fans of the mix shift to higher margin cloud businesses, and aim to remain owners.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Alright, folks, this is what you’ve been waiting for, or at least some of you have.

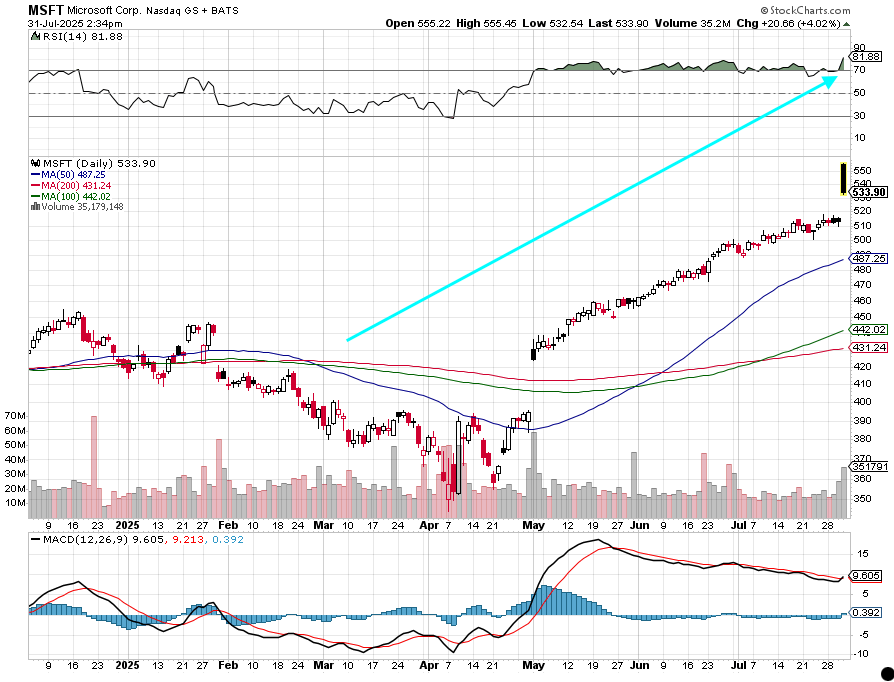

Coming off Wednesday night’s beat-and-raise quarter from Microsoft MSFT, we are raising our MSFT price target to $600 from $515. We’re on record saying that, as Microsoft monetizes the cloud capacity it was adding, we would revisit our MSFT price target, and that is what we are doing today following its impressive June quarter results and guidance.

And while it may not be a popular decision, we are sticking with our Two rating on the shares, given their relative strength index is now north of 80. We recognize this may frustrate some folks, but we simply must stick to our discipline, and that means keeping our Two rating intact, especially on the heels of Thursday's post-earnings pop.

Remember, a Two rating isn't a "sell" rating, but one that indicates we would be buyers on a pullback in the shares. We’ll continue to evaluate entry and pickup levels for folks who are underweight the Portfolio’s MSFT position size, sharing them with you along the way. As we review that, we will lift our MSFT panic point to $450 from $410

Microsoft's Quarter

As we alluded to earlier on Thursday and you’ve likely heard by now, Microsoft not only delivered a beat-and-raise June quarter, but it contained the re-acceleration in cloud that many, including us, had been waiting for. We’ve said that as Microsoft monetizes the cloud capacity it was adding, we would revisit our MSFT price target, and last night’s results show that is happening. Azure and other cloud revenue growth reaccelerated to 39% year over year, nicely ahead of management’s 34% to 35% guidance and the 22% posted in the March quarter.

Fueling that growth, for the first time, commercial bookings were over $100 billion in the quarter, up 37% year over year despite tough comparisons. Management commented that the number of $10 million-plus and $100 million-plus contracts was a big part of that increase and contributed to the company’s commercial remaining performance obligation (RPO) ballooning 35% to $368 billion. Quite impressive, but it was the comment made during the earnings call that roughly 35% of that RPO figure will be recognized as revenue in the next 12 months that really caught our attention. That on its own implies cloud-related revenue near $129 billion over the next year will be higher than simply annualizing the June quarter Intelligent Cloud revenue figure of $29.9 billion. That’s a strong base as we begin the new fiscal year.

Capital spending in the quarter was $24.2 billion and is forecasted to be around $30 billion for the current quarter. Reading between the lines of management comments on the earnings call, capital spending levels are likely to remain near that level in the December quarter, but we could see that rate of capex spending growth be dialed back some as we enter calendar 2026. That would suggest prospects for some additional margin improvement.

The near-term increase is to support the expected ramp in cloud revenue. Building on the RPO comment above, Microsoft management shared it forecasts another year of double-digit revenue ahead with further gains in operating income. Beyond that thumbnail sketch for the current fiscal year and assembling the pieces of its guidance, Microsoft sees total revenue for the current quarter between $74.70 billion to $75.80 billion, up about 15% year over year at the midpoint, and nicely ahead of the $74.15 billion expected by the market. Intelligent cloud is expected to lead the way with Azure revenue growth targeted at 37% while continued Microsoft 365 commercial and consumer cloud growth drives low double-digit growth at the Productivity and Business Processes segment.

Several quarters ago, we commented that when we strip away the jargon and zero in on its revenue stream, Microsoft is really a cloud and service company and increasingly less of a hardware one. Over three-quarters of its revenue stream in the June quarter was tied to Services and related revenue, and we only see that continuing. As the lower-margin More Personal Computing segment becomes a smaller part of the revenue mix, the influence of the higher margin Productivity and Business Processes and Intelligent Cloud should take hold. Much like the mix shift unfolding at Axon AXON, this is one we intend to stick around for.

Implications and Ramifications

During the earnings call, Microsoft shared that its More Personal Computing segment is “well positioned” as it approaches Windows 10 end of support in October, thanks to Windows 11 and Copilot+ PCs. We see that helping accelerate the PC industry mix shift toward AI PCs, which supports Qualcomm’s QCOM comment that it should have more than 100 AI PC designs being commercialized over the next 18 months.

More Pro Portfolio

- We're Adding to 3 Holdings After Recent Weakness

- Weekly Roundup: Trading Opportunistically as S&P Continues Hitting Record Levels

- Going Gray Online in China, AI on the Menu, KitKat Costs and More News for Investing

At the time of publication, TheStreet Pro Portfolio was long MSFT, AXON and QCOM.