May Services PMIs Confirm Inflation Is a Problem for the Fed

With indications pointing to slower May job gains, things could get tricky for the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

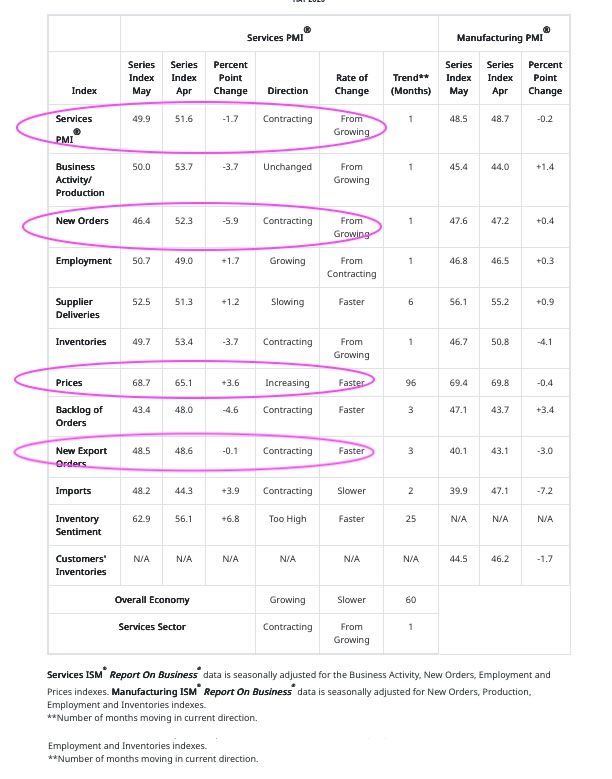

Let’s dig into the latest helping of May economic data: the disappointing ADP Employment Change Report and the twin Services PMI reports from S&P Global and the Institute for Supply Management (ISM). While the Services PMIs offer differing views on the part of the economy that drives 85%+ of overall GDP, because ISM’s data is an input to GDP, we’ll weigh that report and its findings over S&P’s.

What ISM’s May Services PMI report showed was a slowdown in that part of the economy and a sharp drop in new order activity, which signals a further slowing in June is highly probable. This is going to lead to downward revisions in rolling GDP forecasts, such as from the Atlanta Fed, which earlier this week showed the economy running at a 4.6% pace. You’ll recall we were surprised at that revision but there is little question about what should happen next with that GDPNow model.

ISM’s Services data also found, to no real surprise, that Prices chugged higher compared to May. Paired with its May Manufacturing PMI Prices figure that remained at elevated levels and ADP’s May Pay Insights report, it’s quite clear that we should expect upward movement in next week’s May CPI and PPI reports. ADP found median annual pay rose 4.5% year over year for Job-Stayers and 7.0% for Job Changers – unchanged compared to April.

In discussing May inflation pressures, S&P’s U.S. Services PMI report noted the following:

… tariffs and suppliers generally raising their prices meant input cost inflation accelerated steeply in May to its highest since June 2023. Wages were also reported to be a factor pushing up overall operating expenses.

Service sector companies responded by passing on their increased input costs to customers wherever possible. Output charge inflation subsequently jumped noticeably in May, hitting its highest level since August 2022.

Those figures will be a focal point for the Fed, and we would not be surprised to see this week's remaining central bank speakers become more hesitant on the topic of 2025 rate cuts. Atlanta Fed President Raphael Bostic has already commented that he sees just one rate on the table for this year. The inflation data above is likely to move at least a few more members of the FOMC into that camp regardless of what President Trump has to say about rate cuts.

Turning to the Fed’s other mandate, maximum employment, S&P’s findings showed an upturn in hiring in the Services sector while ISM’s pointed to a rebound in hiring in that part of the economy as well. Granted at 50.7, the ISM Employment figure for May does not scream robust hiring but it’s likely to support a figure better than the disappointing 37,000 found in ADP’s May Employment Change Report.

Triangulating those figures, it’s hard to see how Friday’s Employment Report doesn’t deliver a May jobs figure below the 130,000 market consensus, which was already down from April’s 177,000 figure.

This is where things could get tricky for the market. So long as job creation figures remain positive, and even if they dip into modest job losses, we’re likely to see the Fed remain focused on returning inflation back to its 2% target. Remember, several quarters ago, Fed Chair Powell signaled there could be some pain to get inflation down to that target. While that didn’t materialize in 2024, tariffs and the lack of trade deals so far means we are on a different footing this year.

Should Friday’s May Employment Report disappoint, we could see the market move higher as the herd contemplates the Fed doing more. However, should next week’s CPI and PPI data confirm what we’re seeing in the ISM’s May PMI Price figures and those from S&P, we could see the market gyrate as it re-thinks the number of expected Fed rate cuts.

This means we’ll continue to pick our spots, and if need be, move to lock in some gains where it makes sense.